5paisa Capital Ltd.

5paisa Capital Ltd.

5paisa Capital Ltd

5paisa Capital Ltd

Women-Led Companies: High-Growth Companies With Female Leadership

by

5paisa Capital Ltd

27th Nov 2025

Last Updated: 26th November 2025 - 12:25 pm

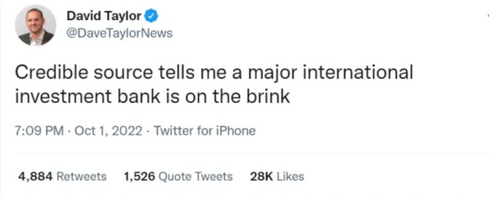

Last weekend was quite eventful for Credit Suisse.

A tweet from renowned business journalist David Taylor whipped up a storm on social media. With his tweet, he hinted at the bankruptcy of Credit Suisse.

The tweet spread like a wildfire on social media platforms. Even though he deleted it later on Monday, the damage was already done. Netizens started comparing its possible fall to 2008, the Lehman Brothers crisis.

The storm on social media platforms spread to the markets as well! Its shares fell around 10% on Monday and reached their all-time low of $3.70.

If you have been missing out on all the drama, here is a quick recap of what happened to Credit Suisse.

Credit Suisse founded in 1856, is one of the largest banks in the world. The Switzerland-headquartered bank is so huge, that it is a global systematically important i.e, its collapse can have a huge impact on the global economy!

Investors and Financial analysts globally have raised concerns about its financial strength. So, is there any substance in this news or are these just rumors? And if it is true, how the hell, did one of the largest banks in the world reach the brink of bankruptcy?

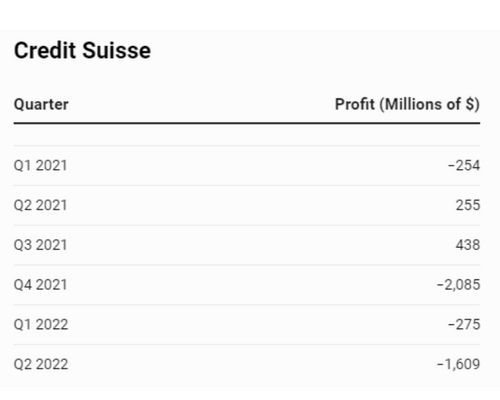

Well, investors aren't just making a fuss about nothing. The Swiss Bank has posted record losses in recent quarters and these losses are mainly due to its reckless decisions and involvement in multiple scandals.

For instance, In March 2021, it lost around $5.5 billion, when a US family-owned hedge fund, Archegos Capital defaulted on its loan. The hedge fund took highly leveraged bets and eventually lost the money. These trades were financed by Credit Suisse and therefore it lost billions when the company defaulted.

As per an independent report, the losses were a result of the failure of its investment banking and prime brokerage division. The bank was greedy and focused on maximizing short-term profits and failed to assess the long-term risks.

An investment bank's primary task is to deploy capital in such a way that returns are higher while risks are low. If it cannot do so, then its employees' competence must be questioned!

Then there was Greensill fiasco. Greensill, a UK-based financial services company mainly offered supply chain loans to its customers. It involves a middleman paying a supplier immediately at a discount, and then collecting the full amount from the buyer a few months later.

Now, to offer these supply chain loans, it borrowed the money from Credit Suisse, who in turn convinced its clients to invest in it. They invested an eye-popping $10 billion in the company, and when Greensill went bust and declared bankruptcy, CS had to freeze the fund.

A lot of investors sued the bank over the Greensill funds. These two weren’t one-off incidences, the bank was involved in various scandals lately. For instance, Credit Suisse pleaded guilty to defrauding investors over an $850 million loan to Mozambique.

Then, a Bermuda court ruled in March that former Georgian Prime Minister Bidzina Ivanishvili and his family are due damages of more than half a billion dollars from Credit Suisse's local life insurance arm. The trial costed the bank $600 million dollars.

All of this has led to the bank losing billions of dollars and a lot of investor confidence. Now, as a listed investment bank you cannot afford to have a bad reputation!

Why, you ask?

Well,

You know the very nature of a bank’s business involves borrowing money. Now, what if the bank defaults or doesn’t pay in full? There is a huge credit risk for the lenders, right? So, to protect themselves against a default, lenders buy credit default swaps. What they do is buy credit default swaps. It is just like buying insurance, they buy these swaps so that in case of default, the buyer would cover these losses.

Increasing credit default swap values indicate that more investors are rushing to buy such swaps as insurance.

In simple terms, now the insurers are asking for more money to insure them against default by Credit Suisse because they believe there are higher chances of a default.

That is exactly what is happening. The CDS of the bank reached its record high on Monday. The last time it reached these levels was in 2008 when the worst financial crisis in the world happened.

How it impacts the bank?

The cost of capital would increase for the bank! High credit spreads would make it difficult for the bank to refinance its debt and would further worsen matters.

The bank quoted,

“A point of concern for many stakeholders, including speculation by the media, continues to be our capitalization and financial strength.

The bank’s top executives have been calling and reassuring its stakeholders about its financial health.

So, is it over for Credit Suisse?

Not yet, it is a systematically important bank. This means the government and other stakeholders would come together to save it if there is a crisis. Remember the Yes Bank debacle? But we hope it doesn’t come to that and things get better.

Business and Economy Related Articles

Women-Led Companies: High-Growth Companies With Female Leadership

Corporate Restructuring Winners: Stocks after Strategic Spinoffs & Mergers in Indian Listed

Family-Owned Turnarounds in Indian Listed Companies: Promoter-Led Companies Modernising Operations

Overview of Various Investment Avenues in India

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.