LIC: Performance beyond IPO!

The LIC IPO made a lot of noise, even in the most uncertain market conditions, it managed to catch the eyeballs of a lot of investors. In this blog, we won’t really talk about its IPO and usual stuff, rather we will dig into its business and see if it has got itself covered.

Before digging into LIC, let's learn a bit about the insurance business, because an insurance business operates in a significantly different manner than any other business.

So, most businesses make money by selling goods and services, now deduct the expenses they have incurred for things like cost of goods etc and there you have the net profit. Easy Peasy, right? Well, Insurance business is not that simple, in the insurance business you pay a regular or one time premium to the insurance company in exchange of a promise that in case of a pre specified event, the company will pay you money, apart from it there are other policies as well, under which you get money as well returns, quite similar to mutual funds.

So, the revenue is mainly the premiums that are collected from the policy holders, plus insurance companies invest their premiums, so that they get returns through which they can provide claims, as well as make profits.

So, what are the ways through which we can analyze LIC,

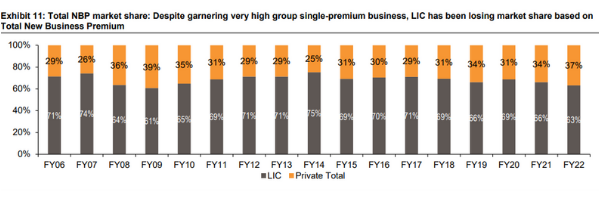

1. Growth in premiums: LIC’s market share based on Total Premium (new and renewal) and Total New Business Premium (regular new premium + single premium) is 62% and 63%, respectively, in FY22.

In the last ten years, its share has fallen from 71% to 63%, while the NBP for the sector has grown at a CAGR of 13%, LIC share has been on a decline.

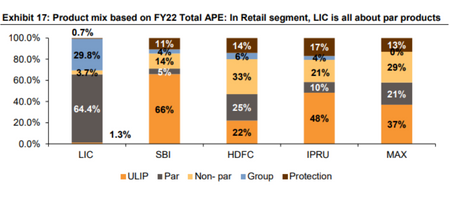

2. Product Mix: Another important factor to analyse an insurance company is to look at its product mix, that is the kind of policies that the company sells.

Why does product mix matter?

Does Tata make the same profit by selling a Jaguar and Nexon? No, right?

Insurance companies have some policies under which they share a part of their profits with the policyholders and these policies constitute 64.4% of LICs portfolio. LIC distributes 95% of its profits to the policyholders and rest to its shareholders. The insurance giant has changed this ratio to 90:10, but still since the share of participating policies is more in its product mix, most of the profits of the company would flow into it.

Now, here the bigger problem is that even if the company wants to increase the share of non participating policies in its mix it would be quite difficult for it to do so because of its distribution mix.

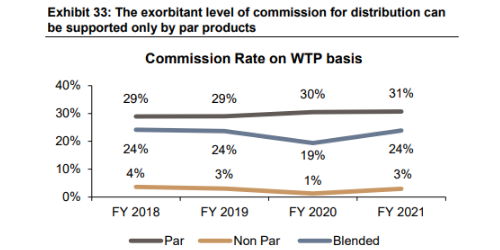

Well, it is no news that LIC has a massive network of agents, I bet you must have a chacha, bhaiya, or padosi who is an LIC agent.

To change the product mix, these agents would have to push the non-participating policies among their customers, however it is difficult because the non-par policies are low margins and commissions are generally higher in the participating policies.

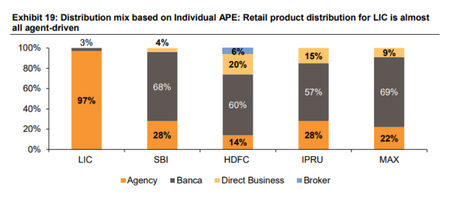

LIC’s distribution mix is definitely something the company needs to work on, with 97% of its individual policies sold through agents, its business is dependent a lot on them, also having an army of agents increase the commission expenses of the company drastically, also, with more internet penetration people are preferring to buy insurance through digital channels and therefore the company should try increasing its sales through banks or digital channels.

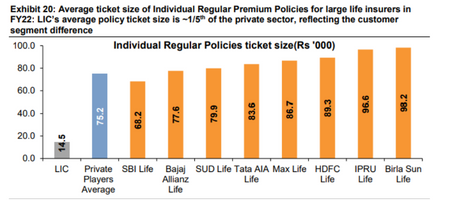

3. Ticket Size of Premiums: If we look at the average ticket size of regular individual insurance policies, the ticket size of LIC is ⅕ that of the private players, considering its high operational costs the company needs to work on increasing the ticket size as well.

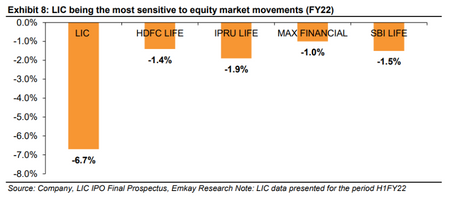

High exposure to equity investments: As we discussed before, Insurance companies' major income comes from their investments in different instruments, and LIC, total investment or Assets under management is more than the entire mutual fund industry.

Sounds like something LIC should be proud of but here’s the catch my friend, LIC high AUM is something that it boasts about, but when you delve deeper you see that 25% of its holdings are invested into equity markets, which is quite high when compared with its peers.

Since equity markets are quite volatile, and LIC has a lot of exposure to them, any volatility in the markets can impact the financials of LIC.

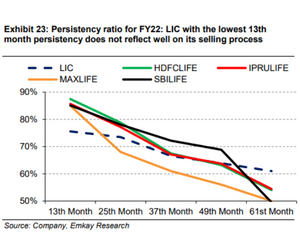

4. Persistency ratio: Another important metric for an Insurance business is the persistency ratio.

The Persistence ratio basically tells you how many people are paying their renewal premiums.

The persistency ratio is less when compared with its peers in 13th month duration, but over the years persistency ratio for LIC has more or less been the same, which is a positive.

5. Valuation

LICs current market cap is 5.3 trillion, while its embedded value is around Rs. 5.4 trillion, LIC Market cap/EV is around 1-1.05, while if we talk about the private players their valuation is 2x-4x of their EV, but you see while valuing a company we look at the future growth prospects of the companies, now in case of insurance, either the growth in the business could be due to increase in sales or VNB margins. Private players command very high VNB margins when compared to LIC, primarily because of the cost heavy structure of its business. Therefore, its valuation should not be compared with them. Also, the increase in its EV is due to change in its funds bifurcations, and most of the money of that change is in equity investments that are prone to volatility in the markets.

Some downside risks of its business are investment-variance due to equity market fluctuations and the lack of interest-rate hedging on the guaranteed book and lower-than-expected VNB margin expansion because of the company’s sticky cost structure.

LIC is a mammoth, its gigantic size is something that sets it apart. But its gigantic size is in a way stopping it from being agile, and adopting the change. So, is its size a two edged sword?

Start Investing in 5 mins*

Rs. 20 Flat Per Order | 0% Brokerage