The Z-Score, developed by Edward Altman in 1968, is a financial metric that helps assess the likelihood of a company experiencing bankruptcy within the next two years. This formula combines several financial ratios to provide a snapshot of a company’s financial stability. By measuring aspects such as liquidity, profitability, leverage, and efficiency, the Z-Score offers valuable insight into a company’s overall health. The score is primarily used by investors, creditors, and financial analysts to gauge the risk level associated with a company, helping them make more informed decisions regarding investments or credit extensions. A higher Z-Score indicates a lower risk of bankruptcy, while a lower score suggests higher financial distress, potentially signaling impending financial troubles. As a reliable tool for evaluating corporate distress, the Z-Score has become a critical instrument in the financial industry.

What is a Z-Score?

A Z-Score is a financial ratio used to predict the likelihood of a company’s bankruptcy by analyzing its financial health. Developed by Edward Altman in 1968, this score combines five key financial variables—working capital, retained earnings, earnings before interest and taxes (EBIT), market value of equity, and sales—into a single number. The Z-Score helps identify companies at risk of financial distress by evaluating their liquidity, profitability, leverage, and operational efficiency. A higher Z-Score indicates a lower risk of bankruptcy, while a lower Z-Score suggests a higher likelihood of financial trouble. This tool is widely used by investors, creditors, and analysts to assess the financial stability of a company and make informed decisions about investments, loans, or partnerships. The Z-Score has become a standard method for predicting corporate solvency and is particularly useful in evaluating the creditworthiness of firms.

How is the Z-Score Calculated?

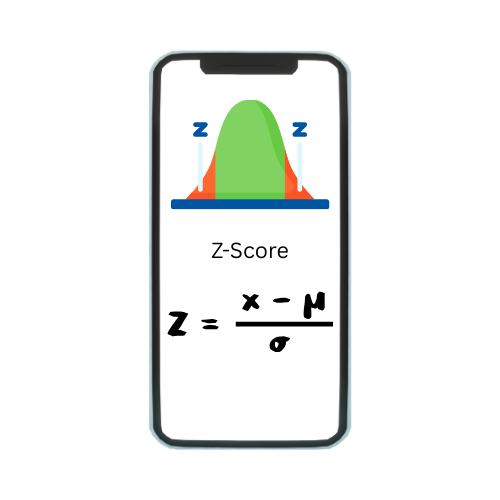

The Z-Score is calculated using a weighted formula that combines five distinct financial ratios, each representing a different aspect of a company’s financial health. The original Altman Z-Score formula is:

Z = 1.2 × (A) + 1.4 × (B) + 3.3 × (C) + 0.6 × (D) + 1.0 × (E)

Where:

- A= Working Capital / Total Assets (measures liquidity)

- B= Retained Earnings / Total Assets (indicates profitability and reinvested earnings)

- C= EBIT / Total Assets (shows operational efficiency)

- D= Market Value of Equity / Total Liabilities (reflects solvency and market confidence)

- E= Sales / Total Assets (assesses asset turnover and efficiency)

Each variable is given a specific weight to reflect its importance in predicting the probability of bankruptcy. The resulting Z-Score is a single number that summarizes a company’s financial condition. A higher Z-Score suggests financial strength, while a lower score indicates potential distress. This method is particularly effective for manufacturing and publicly listed companies and serves as a practical tool for financial risk assessment.

Interpreting the Z-Score

The Z-Score offers valuable insights into a company’s financial risk. The general thresholds for the Z-Score are as follows:

- Z-Score Above 2.99: The company is considered financially healthy, with a low risk of bankruptcy.

- Z-Score Between 1.8 and 2.99: The company is in the “grey” zone, where there is some risk of financial trouble, but it is not an immediate concern.

- Z-Score Below 1.8: The company is at high risk of bankruptcy, and financial distress is likely.

Why is the Z-Score Important?

- Predicts Financial Distress:The Z-Score serves as an early warning system by identifying companies at risk of bankruptcy, allowing stakeholders to take preventive actions.

- Supports Investment Decisions:Investors rely on the Z-Score to evaluate a company’s financial stability before allocating capital, helping them avoid high-risk investments.

- Assists Credit Evaluation:Lenders and creditors use the Z-Score to determine the creditworthiness of a company, which influences loan approvals and interest rates.

- Aids in Corporate Monitoring:Internal management can use the Z-Score to monitor the company’s financial health over time and implement corrective strategies if needed.

- Facilitates Mergers and Acquisitions:In M&A transactions, the Z-Score helps assess the financial viability of target companies, reducing the risk of acquiring distressed assets.

- Provides a Standardized Metric:It offers a consistent and quantitative measure of financial risk across companies, making it easier to compare firms within the same industry.

Applications of the Z-Score

- Bankruptcy Prediction:The Z-Score is widely used to forecast the likelihood of a company entering bankruptcy within a specified time frame, typically two years. It helps stakeholders identify financially unstable firms early.

- Investment Risk Assessment:Investors use the Z-Score to assess the financial soundness of companies they are considering investing in. A low score may indicate high risk and discourage investment.

- Credit Risk Analysis:Banks and financial institutions rely on the Z-Score to evaluate the repayment ability of borrowers, especially in corporate lending. A strong score can lead to better credit terms.

- Corporate Financial Health Monitoring:Companies themselves use the Z-Score as an internal tool to monitor financial performance and detect early signs of distress, enabling timely corrective actions.

- Due Diligence in M&A:During mergers and acquisitions, acquirers use the Z-Score to analyze the target company’s financial condition and avoid taking over liabilities associated with distressed businesses.

Advantages of Using the Z-Score

- Early Warning System:The Z-Score provides an early indication of financial distress, allowing companies, investors, and creditors to take preventive or corrective measures before a crisis occurs.

- Comprehensive Risk Assessment:By combining multiple financial ratios into a single score, it offers a holistic view of a company’s financial health, covering liquidity, profitability, leverage, and efficiency.

- Simple and Quantifiable:The Z-Score is easy to compute and interpret, providing a clear numerical value that can be used to compare companies or track performance over time.

- Widely Accepted Tool:It is a well-established and trusted method in the finance industry, commonly used by analysts, lenders, auditors, and regulatory agencies for risk evaluation.

- Objective and Data-Driven:Since it relies on audited financial statements, the Z-Score is grounded in factual data, minimizing subjective judgment in financial analysis.

- Helps Avoid Costly Mistakes:Investors and creditors can use the Z-Score to steer clear of financially unstable companies, potentially saving money and reducing exposure to default risk.

Limitations of the Z-Score

- Industry Specificity:The original Z-Score model was designed primarily for publicly traded manufacturing firms, making it less reliable for service-based, financial, or startup companies with different financial structures.

- Outdated Weightings:The formula uses fixed weightings based on historical data from the 1960s, which may not fully reflect today’s dynamic business environments or sector-specific nuances.

- Market Value Dependency:The model includes the market value of equity, which can fluctuate significantly due to external market conditions, potentially skewing the score without reflecting real financial distress.

- Ignores Qualitative Factors:The Z-Score only considers quantitative financial data and overlooks qualitative aspects such as management quality, brand strength, market competition, or regulatory risks.

- Limited for Private Companies:Traditional Z-Score models require market value inputs, which are not available for private companies, making the original model less applicable without adjustments.

The Evolution of the Z-Score Model

Since the creation of the original Z-Score, it has undergone modifications to improve its accuracy and relevance. The most notable updates include:

- Z-Score for Private Companies: A variation of the Z-Score has been developed for privately held companies, which do not have a market value of equity (as required by the original formula).

- Z’-Score: This version is designed for private companies and uses slightly different variables, such as Total Assets instead of Market Value of Equity.

- Z’’-Score: A newer version of the Z-Score that focuses on emerging market companies, incorporating regional financial conditions into the formula.

Z-Score and Market Volatility

The Z-Score plays a significant role during periods of market volatility, as it helps assess a company’s resilience amid economic uncertainty. In turbulent market conditions—such as during recessions, geopolitical tensions, or financial crises—companies with weak financial fundamentals are more likely to experience distress or insolvency. The Z-Score becomes particularly valuable in such scenarios by highlighting firms that may not withstand sharp declines in revenue, rising debt costs, or liquidity crunches. Since it evaluates factors like profitability, leverage, and liquidity, the Z-Score enables investors and creditors to distinguish between financially stable companies and those vulnerable to market shocks. However, it’s important to note that sudden market fluctuations can also impact components of the Z-Score, such as market capitalization, potentially leading to short-term distortions. Despite this, the Z-Score remains a useful tool for identifying companies that are fundamentally at higher risk during periods of economic stress.

Z-Score and Its Impact on Credit Ratings

The Z-Score has a direct influence on a company’s creditworthiness and, consequently, its credit rating. Credit rating agencies often consider financial health indicators like the Z-Score when assessing a company’s ability to meet its debt obligations. A high Z-Score reflects strong financial stability, signaling to credit analysts that the company is less likely to default, which can lead to a favorable credit rating. Conversely, a low Z-Score suggests higher bankruptcy risk, increasing the likelihood of a downgrade in the company’s credit rating. Such downgrades can raise borrowing costs, reduce investor confidence, and limit access to financing. Since credit ratings affect everything from bond yields to investor perceptions, maintaining a healthy Z-Score can be essential for a company seeking to preserve financial flexibility. While not the sole factor, the Z-Score serves as a critical quantitative input that supports credit risk evaluation and lending decisions.

Conclusion

The Z-Score stands as a powerful and practical tool in the realm of financial analysis, offering a concise yet comprehensive measure of a company’s financial health and bankruptcy risk. By integrating key financial ratios—covering liquidity, profitability, leverage, and efficiency—it provides valuable insights that aid investors, creditors, and corporate managers in making informed decisions. Whether used to assess investment opportunities, evaluate credit risk, or monitor internal financial performance, the Z-Score delivers objective and data-driven guidance. However, like any analytical model, it is not without limitations. It must be applied with an understanding of industry context, company-specific nuances, and market dynamics. When used alongside other qualitative and quantitative assessments, the Z-Score can significantly enhance the accuracy of financial evaluations and strategic planning. As market conditions continue to evolve, the relevance of the Z-Score remains intact, especially as a preventive indicator of financial distress in an increasingly uncertain economic environment.