A Long Iron Butterfly is implemented when an investor is expecting volatility in the underlying assets. This strategy is initiated to capture the movement outside the wings of options at expiration. It is a limited risk and a limited reward strategy. A Long Iron Butterfly could also be considered as a combination of bull call spread and bear put spread.

When to initiate a Long Iron Butterfly

A Long Iron Butterfly spread is best to use when you expect the underlying assets to move sharply higher or lower but you are uncertain about direction. Also, when the implied volatility of the underlying assets falls unexpectedly and you expect volatility to shoot up, then you can apply Long Iron Butterfly strategy.

How to construct a Long Iron Butterfly?

A Long Iron Butterfly can be created by buying 1 ATM call, Selling 1 OTM call, buying 1 ATM put and selling 1 OTM put of the same underlying security with the same expiry. Strike price can be customized as per the convenience of the trader; however, the upper and lower strike must be equidistant from the middle strike.

Let’s try to understand with an example:

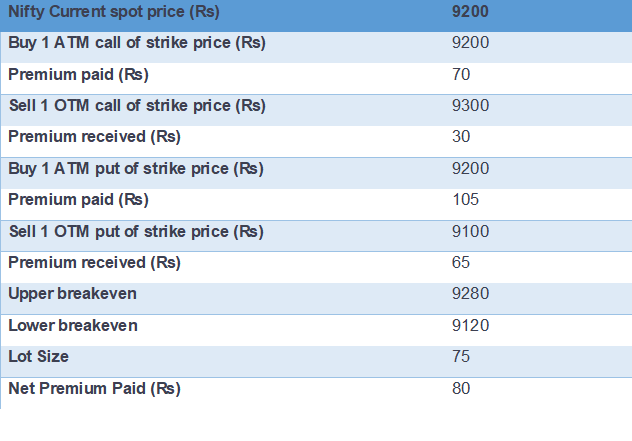

Suppose Nifty is trading at 9200. An investor Mr A thinks that Nifty will move drastically in either direction, below lower strike or above higher strike by expiration. So he enters a Long Iron Butterfly by buying a 9200 call strike price at Rs 70, selling 9300 call for Rs 30 and simultaneously buying 9200 put for Rs 105, selling 9100 put for Rs 65. The net premium paid to initiate this trade is Rs 80, which is also the maximum possible loss.

This strategy is initiated with a view of movement in the underlying security outside the wings of higher and lower strike price in Nifty. Maximum profit from the above example would be Rs 1500 (20*75). Maximum loss will also be limited up to Rs 6000 (80*75).

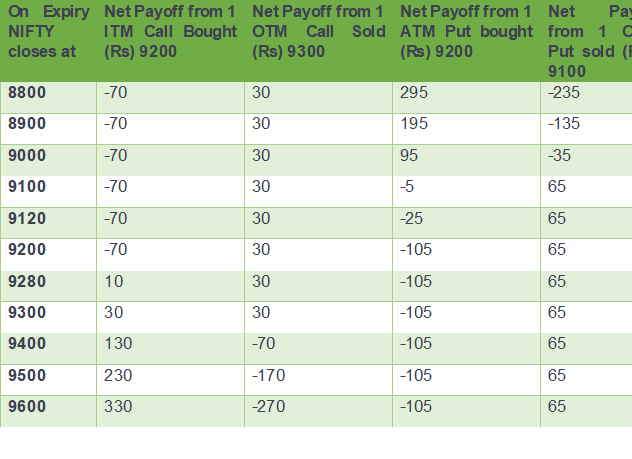

For the ease of understanding of the payoff, we did not take in to account commission charges. Following is the payoff chart and payoff schedule assuming different scenarios of expiry.

The Payoff chart:

The Payoff Schedule:

Impact of Options Greeks before expiry:

Delta: The net Delta of a Long Iron Butterfly spread remains close to zero if underlying assets remain at middle strike. Delta will move towards 1 if underlying expires above higher strike price and Delta will move towards -1 if underlying expires below the lower strike price.

Vega: Long Iron Butterfly has a positive Vega. Therefore, one should buy Long Iron Butterfly spread when the volatility is low and expect to rise.

Theta: With the passage of time, if other factors remain same, Theta will have a negative impact on the strategy.

Gamma: This strategy will have a long Gamma position, so the change in underline assets will have a positive impact on the strategy.

How to manage Risk?

A Long Iron Butterfly is exposed to limited risk but risk involved is higher than the net reward from the strategy, one can keep stop loss to further limit the losses.

Analysis of Long Iron Butterfly strategy:

A Long Iron Butterfly spread is best to use when you are confident that an underlying security will move significantly. Another way by which this strategy can give profit is when there is an increase in implied volatility. However, this strategy should be used by advanced traders as the risk to reward ratio is high.