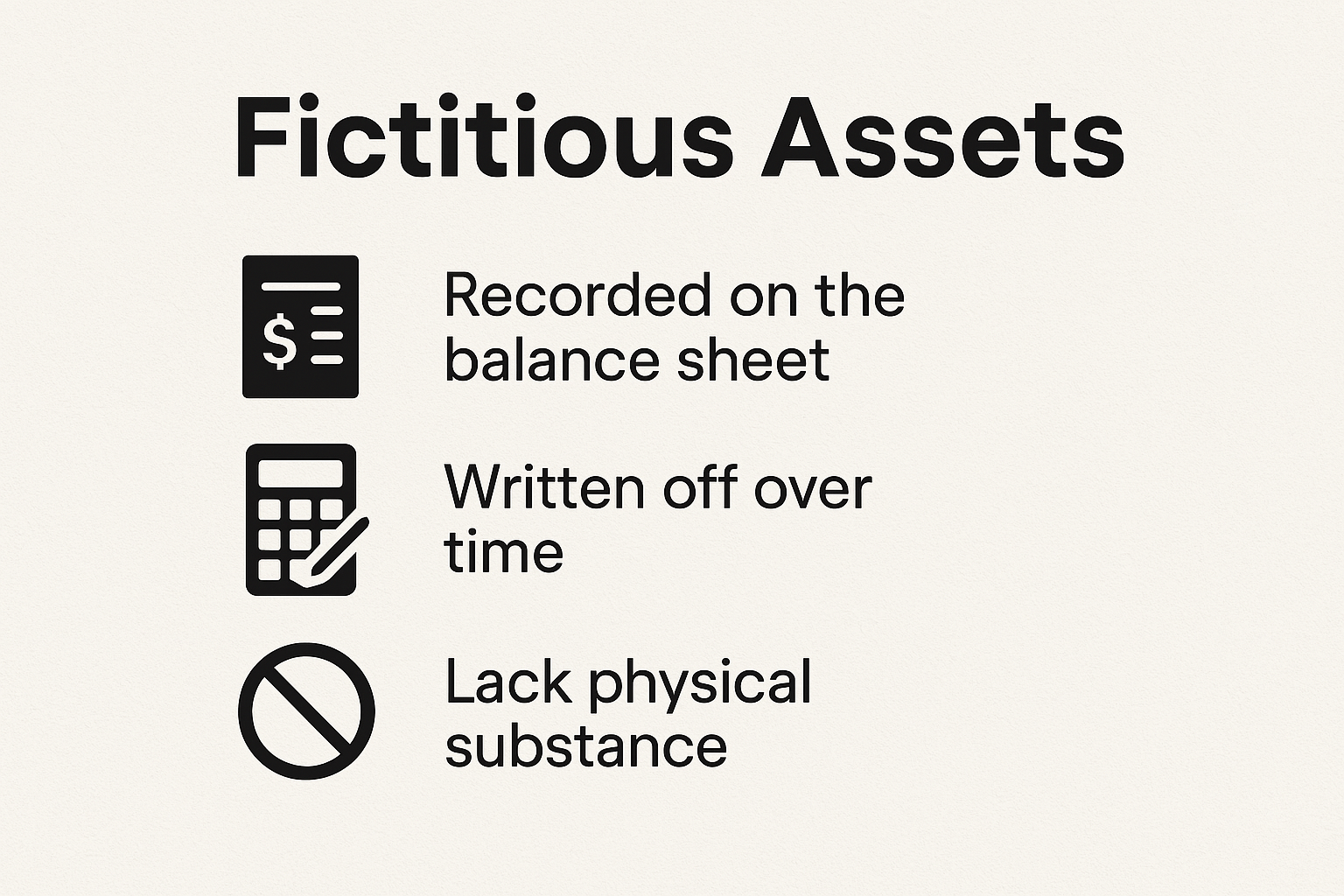

Fictitious assets aren’t real assets in the traditional sense; they don’t have physical substance or intrinsic value but are recorded on the balance sheet to represent expenses that can’t be immediately written off. These include preliminary expenses, promotional expenses, and accumulated losses.

Even though they’re called “assets,” they don’t generate revenue or hold tangible value like cash, inventory, or real estate. Instead, they are expenses or losses that companies carry over for accounting purposes. Businesses aim to gradually write them off against future profits.

Definition of Fictitious Assets

Fictitious assets are expenses or losses recorded on a company’s balance sheet that do not hold tangible value but are carried forward for accounting purposes. They are not actual assets like cash, inventory, or property, but instead represent expenditures that cannot be immediately written off. Examples include preliminary expenses, accumulated losses, and promotional costs. Businesses gradually write them off against future earnings until fully amortized.

Common Examples

- Promotional Expenses– Expenses related to advertising, marketing campaigns, and brand promotion that do not hold tangible value.

- Losses from Issue of Debentures– Discounts or expenses associated with raising funds through debentures that are amortized over time.

- Accumulated Losses– Past losses that are carried forward in financial statements instead of being written off immediately.

- Underwriting Commission –Fees paid to underwriters for helping a company issue shares or debentures.

Why Traders Should Care About Fictitious Assets

Traders should pay attention to fictitious assets because they can impact a company’s financial health and valuation. While these assets don’t have tangible value, they affect accounting decisions, profitability, and investment strategies. Here’s why they matter:

- Financial Transparency –Companies with significant fictitious assets may appear stronger than they actually are. Traders must assess how these expenses are being written off to understand the true financial position.

- Impact on Profits – Since fictitious assets are gradually amortized, they can reduce reported profits over time. This affects earnings reports, which traders closely monitor.

- Stock Valuation – A company carrying excessive fictitious assets may have inflated valuations. Traders should analyze whether the business is truly generating value or just managing losses.

- Liquidity Concerns –Fictitious assets don’t contribute to a company’s cash flow, which can be a red flag for traders seeking companies with strong financial fundamentals.

- Risk Assessment– If a company relies heavily on fictitious assets, it may indicate poor financial management or previous losses that haven’t been recovered, raising concerns for investors.

Impact on Financial Statement Analysis

- Balance Sheet Appearance –Fictitious assets inflate the asset side of the balance sheet even though they lack tangible value. This can misrepresent a company’s financial strength.

- Profitability Impact – Since these assets are gradually written off, they reduce reported profits over time, affecting earnings per share (EPS) and investor confidence.

- Liquidity Misrepresentation –Companies with large fictitious assets may seem well-capitalized, but since these assets don’t generate cash, they can mask liquidity issues.

- Debt-to-Asset Ratio Distortion –Businesses carrying significant fictitious assets may appear to have better debt-to-asset ratios than they actually do, potentially misleading creditors.

- Investment Decisions –Analysts and traders must carefully adjust financial ratios to exclude fictitious assets when evaluating a company’s actual financial condition.

Role in IPO and New Listings

Fictitious assets play a crucial role in IPOs (Initial Public Offerings) and new stock listings, as they can influence a company’s financial presentation before going public. Here’s how they impact the process:

- Enhancing Financial Statements– Companies often manage fictitious assets strategically to improve the appearance of their balance sheet before an IPO, making them seem financially stronger to investors.

- Investor Perception– Since IPO investors rely on financial disclosures, excessive fictitious assets can create an illusion of profitability, potentially leading to misinterpretations of a company’s actual financial health.

- Regulatory Scrutiny– Regulatory bodies examine fictitious assets closely during IPO filings to ensure transparency and proper accounting treatment, preventing companies from misleading investors.

- Amortization Planning– Firms plan how they will write off fictitious assets over future years, impacting post-IPO earnings reports and financial performance expectations.

- Valuation Adjustments– Investment banks and analysts adjust company valuations by factoring in fictitious assets, ensuring more realistic pricing for new shares.

Accounting Treatment of Fictitious Assets

The accounting treatment of fictitious assets ensures they are gradually written off over time instead of being treated as revenue-generating assets.

- Recording in the Balance Sheet– Fictitious assets appear under the asset side of the balance sheet, even though they don’t have intrinsic value. They are carried forward as deferred expenses.

- Amortization Over Time– These expenses are systematically amortized over several financial periods instead of being written off in a single year. The amortization method depends on company policy and accounting standards.

- Impact on Profit and Loss Account –As amortization occurs, a portion of these expenses is transferred to the Profit and Loss (P&L) account, reducing the net profit for that period.

- Tax Treatment Considerations– Certain fictitious assets, like preliminary expenses, may be eligible for tax deductions. Companies must follow tax regulations to claim deductions accordingly.

- Compliance with Accounting Standards– Businesses must adhere to accounting principles such as IFRS and GAAP to ensure accurate reporting and prevent financial misrepresentation.

- Gradual Write-Off Process– Over time, fictitious assets are completely eliminated from the books, reducing their impact on future financial statements.

How They Are Recorded

Fictitious assets are recorded in financial statements as deferred expenses rather than tangible assets. Here’s the step-by-step process for recording them:

- Initial Recognition –When a company incurs expenses that qualify as fictitious assets (such as preliminary expenses or losses on debenture issuance), they are recorded on the asset side of the balance sheet under a separate account.

- Classification as Deferred Expenses –These expenses are classified as deferred because they cannot be fully written off in the current accounting period and will be gradually amortized.

- Amortization Process– Each financial period, a portion of the fictitious asset is transferred from the balance sheet to the Profit & Loss (P&L) account. This reduces net profit for that year but helps spread the cost over multiple periods.

- Impact on Financial Ratios– Businesses adjust financial metrics such as net income and total assets to reflect the amortization of fictitious assets.

- Complete Write-Off –Once fully amortized, the fictitious asset disappears from the books, ensuring accurate financial representation.

Method of Write-off

The write-off method for fictitious assets involves gradually eliminating these expenses from the financial records over multiple accounting periods. Here’s how it works:

- Amortization Over Time – Fictitious assets are systematically written off in portions rather than all at once. The company decides on the number of years over which the expense will be amortized.

- Charge to Profit & Loss (P&L) Account – Each year, a portion of the fictitious asset is transferred from the balance sheet to the P&L account, reducing reported profits.

- Accounting Standards Compliance – The write-off must follow relevant accounting standards (such as IFRS or GAAP) to ensure financial transparency.

- Impact on Taxation – In some cases, expenses categorized as fictitious assets may qualify for tax deductions, benefiting the company financially.

- Final Write-Off – Once the full amount has been amortized, the fictitious asset is removed from the balance sheet, reflecting a more accurate financial position.

No Resale Value or Recovery

Fictitious assets have no resale value or recovery because they do not represent tangible or realizable assets like machinery, real estate, or inventory. Unlike physical assets that can be sold or liquidated, fictitious assets exist purely for accounting purposes and are gradually written off over time.

Here’s why they hold no resale value:

- Not Physical or Marketable – They are recorded expenses, such as preliminary costs or promotional expenses, which cannot be sold or exchanged.

- No Direct Financial Benefit – Unlike investments or inventory, fictitious assets do not generate revenue or provide economic benefits in future transactions.

- Gradual Write-Off – Companies systematically write them off over years to reduce their impact on profitability.

- Cannot Be Recovered – Once amortized, they disappear from the books, leaving no residual value.

Trader’s Checklist for Evaluating Fictitious Assets

Balance Sheet Review

Check if fictitious assets are reported under deferred expenses. Analyze the proportion of fictitious assets relative to total assets. Look for excessive preliminary expenses that could distort financial strength.

Profitability Impact

Assess how amortization affects net profits over multiple periods. Compare reported profits with actual cash flow to ensure realistic earnings. Look for signs of financial engineering used to manage fictitious asset write-offs.

Liquidity and Cash Flow

Ensure fictitious assets are not misleading liquidity ratios. Compare cash reserves with fictitious asset balances. Watch for signs of financial strain masked by large deferred expenses.

Debt and Leverage Considerations

Determine whether fictitious assets are inflating total asset value. Check debt-to-equity ratio adjustments that exclude fictitious assets. Assess if excessive fictitious assets suggest past financial distress.

Regulatory and Compliance Factors

Verify if fictitious assets are being reported per accounting standards (GAAP/IFRS). Check IPO filings for transparency in reporting fictitious assets. Investigate historical adjustments to fictitious assets in financial statements.

By following this checklist, traders can gain a clearer understanding of a company’s true financial standing. Would you like a case study or real-world example of how fictitious assets have influenced stock valuations?

Conclusion

Fictitious assets play a significant role in financial reporting, affecting balance sheets, profitability, and investment decisions. While they do not hold tangible value, companies use them strategically to manage expenses and present financial stability. Traders and investors must carefully evaluate fictitious assets to ensure a realistic assessment of a company’s financial health.

Understanding how these assets are recorded, written off, and influence trading strategies helps mitigate risks and make informed investment choices. By applying smart analysis techniques, traders can navigate potential financial misrepresentations and enhance their decision-making process.