મ્યુચ્યુઅલ ફંડ લાંબા સમયથી સ્ટૉક માર્કેટની જટિલતાઓ વિશે સીધા જાણ કર્યા વિના ડાઇવર્સિફિકેશન અને પ્રોફેશનલ મેનેજમેન્ટ મેળવવા માંગતા વ્યક્તિઓ માટે સૌથી લોકપ્રિય ઇન્વેસ્ટમેન્ટ વિકલ્પોમાંથી એક છે. તેઓ ઘણીવાર રોકાણકારો માટે તેમના નાણાંકીય લક્ષ્યોને પ્રાપ્ત કરવા માટે સુવિધાજનક, ઓછા ખર્ચની રીત તરીકે માર્કેટ કરવામાં આવે છે. જો કે, તેમની સ્પષ્ટ સરળતાની સપાટીની નીચે છુપાયેલા ખર્ચની શ્રેણી છે જે તમારી સંપૂર્ણ જાગૃતિ વિના તમારા રિટર્નને બગાડી શકે છે. આ ખર્ચ, જે ઘણીવાર ફંડના માળખા અને કામગીરીમાં શામેલ હોય છે, તે સમય જતાં તમારી સંપત્તિને નોંધપાત્ર રીતે અસર કરી શકે છે. શું તમે તમારા મ્યુચ્યુઅલ ફંડના રોકાણ માટે વિચારી રહ્યા છો તેના કરતાં વધુ ચૂકવણી કરી રહ્યા છો? ચાલો છુપાયેલા ખર્ચ અને તેમની અસરોને શોધવા માટે મ્યુચ્યુઅલ ફંડની દુનિયામાં ઊંડાણપૂર્વક વિચાર કરીએ.

ખર્ચના રેશિયો: તમારા રિટર્ન પર ચાલુ ડ્રેન

મ્યુચ્યુઅલ ફંડ સાથે સંકળાયેલા સૌથી જાણીતા ખર્ચ ખર્ચનો રેશિયો છે. આ મેનેજમેન્ટ ફી, વહીવટી ખર્ચ અને માર્કેટિંગ ખર્ચ જેવા સંચાલન ખર્ચને કવર કરવા માટે ફંડ દ્વારા વસૂલવામાં આવતી વાર્ષિક ફીનું પ્રતિનિધિત્વ કરે છે. જ્યારે ખર્ચના રેશિયોને અગાઉથી જાહેર કરવામાં આવે છે, ત્યારે ઘણા રોકાણકારો તેમની લાંબા ગાળાની અસરને ધ્યાનમાં લેવામાં નિષ્ફળ થાય છે. 1% ના નાના ખર્ચના રેશિયો સાથેનો ફંડ દાયકાઓથી નોંધપાત્ર ખર્ચમાં કમ્પાઉન્ડ કરી શકે છે, જે તમારા એકંદર રિટર્નને નોંધપાત્ર રીતે ઘટાડી શકે છે.

ઉદાહરણ તરીકે, જો તમે 1% એક્સપેન્સ રેશિયો સાથે મ્યુચ્યુઅલ ફંડમાં ₹10,00,000 ઇન્વેસ્ટ કરો છો અને 8% નું સરેરાશ વાર્ષિક રિટર્ન કમાઓ છો, તો 20 વર્ષથી વધુના એક્સપેન્સ રેશિયોનો કમ્પાઉન્ડ ખર્ચ ઘણા લાખ જેટલો હોઈ શકે છે. પેસિવ ઇન્ડેક્સ ફંડ્સ જેવા ઓછા ખર્ચ રેશિયો ફંડ્સ, સક્રિય રીતે સંચાલિત ફંડ્સ માટે ખર્ચ-કાર્યક્ષમ વિકલ્પ પ્રદાન કરે છે, જ્યાં ઉચ્ચ ફી ઘણીવાર સામાન્ય રીતે વધુ સારી પરફોર્મન્સને યોગ્ય ઠેરવવામાં નિષ્ફળ થાય છે.

એક્ઝિટ લોડ: વહેલા ઉપાડનો ખર્ચ

રોકાણકારો ઘણીવાર એક્ઝિટ લોડને અવગણતા હોય છે, જે જ્યારે તમે ચોક્કસ સમયસીમા પહેલાં તમારા એકમોને રિડીમ કરો છો ત્યારે મ્યુચ્યુઅલ ફંડ દ્વારા વસૂલવામાં આવતા શુલ્ક છે. સામાન્ય રીતે 0.5% થી 1% સુધી, એક્ઝિટ લોડનો હેતુ ટૂંકા ગાળાના ટ્રેડિંગને નિરુત્સાહિત કરવાનો છે અને સુનિશ્ચિત કરવાનો છે કે રોકાણકારો લાંબા ગાળા માટે પ્રતિબદ્ધ રહે. જો કે, જો તમારે અણધાર્યા સંજોગોમાં તમારા ઇન્વેસ્ટમેન્ટને ઉપાડવાની જરૂર હોય, તો આ શુલ્ક તમારા રિટર્નને ઘટાડી શકે છે.

બૅકગ્રાઉન્ડમાં છુપાયેલ ખર્ચ

મ્યુચ્યુઅલ ફંડ સાથે સંકળાયેલ અન્ય અદૃશ્ય ખર્ચ ટ્રાન્ઝૅક્શન ખર્ચ છે. આમાં તેના પોર્ટફોલિયોમાં સિક્યોરિટીઝ ખરીદતી વખતે અથવા વેચતી વખતે ફંડ દ્વારા કરવામાં આવતી બ્રોકરેજ ફી, સ્ટેમ્પ ડ્યુટી અને સિક્યોરિટીઝ ટ્રાન્ઝૅક્શન ટૅક્સ (STT) શામેલ છે. જોકે આ ખર્ચ સીધા રોકાણકારો પાસેથી વસૂલવામાં આવતા નથી, પરંતુ તેઓ ફંડના નેટ એસેટ વેલ્યૂ (એનએવી) માં એમ્બેડ કરવામાં આવે છે, પરોક્ષ રીતે તમારા રિટર્નને ઘટાડે છે.

ઉચ્ચ પોર્ટફોલિયો ટર્નઓવરવાળા ફંડ-સિક્યોરિટીઝની વારંવાર ખરીદી અને વેચાણ-વધુ ટ્રાન્ઝૅક્શન ખર્ચ ધરાવે છે. સક્રિય રીતે સંચાલિત ફંડ, ખાસ કરીને, ઘણીવાર નોંધપાત્ર ટ્રાન્ઝૅક્શન ખર્ચ થાય છે, જે ઓછા-ટર્નઓવર ઇન્ડેક્સ ફંડના સંબંધમાં તેમના પરફોર્મન્સને ઘટાડી શકે છે.

ટૅક્સ: અનિવાર્ય ખર્ચ

ટૅક્સ મ્યુચ્યુઅલ ફંડની અન્ય છુપાયેલ કિંમતનું પ્રતિનિધિત્વ કરે છે. જ્યારે ટૅક્સ એક જરૂરી જવાબદારી છે, ત્યારે જો અસરકારક રીતે મેનેજ ન કરવામાં આવે તો મ્યુચ્યુઅલ ફંડ રિટર્ન પર તેમની અસર નોંધપાત્ર હોઈ શકે છે. મ્યુચ્યુઅલ ફંડ પર ટૅક્સ કેવી રીતે લાગુ પડે છે તે અહીં આપેલ છે:

- ઇક્વિટી મ્યુચ્યુઅલ ફંડ: 12 મહિનાથી ઓછા સમય માટે રાખેલ ઇક્વિટી ફંડમાંથી મળતા લાભોને શોર્ટ ટર્મ કેપિટલ ગેઇન (એસટીસીજી) તરીકે વર્ગીકૃત કરવામાં આવે છે અને 15% પર કર લાદવામાં આવે છે. 12 મહિનાથી વધુ સમય માટે રાખવામાં આવેલા એકમોમાંથી મળેલા લાભોને લાંબા ગાળાના મૂડી લાભ (એલટીસીજી) તરીકે વર્ગીકૃત કરવામાં આવે છે, જેમાં ઇન્ડેક્સેશન વગર ₹1 લાખથી વધુના લાભ પર 10% પર કર લાદવામાં આવે છે.

- ડેબ્ટ મ્યુચ્યુઅલ ફંડ: ત્રણ વર્ષથી ઓછા સમય માટે હોલ્ડ કરેલ ડેબ્ટ ફંડમાંથી મળતા લાભોને એસટીસીજી તરીકે ગણવામાં આવે છે અને તમારા લાગુ ઇન્કમ ટૅક્સ સ્લેબ રેટ પર ટૅક્સ લગાવવામાં આવે છે. ત્રણ વર્ષથી વધુ સમય માટે રાખવામાં આવેલા એકમોમાંથી મળતા લાભો એલટીસીજી તરીકે પાત્ર છે, જે ઇન્ડેક્સેશન લાભો સાથે 20% પર કર લાદવામાં આવે છે.

ટૅક્સેશન તમારા મ્યુચ્યુઅલ ફંડ રિટર્નને નોંધપાત્ર રીતે અસર કરી શકે છે, ખાસ કરીને જો તમે વારંવાર યુનિટ રિડીમ કરો છો અથવા ટૅક્સ કાર્યક્ષમતાને ધ્યાનમાં રાખીને તમારા ઇન્વેસ્ટમેન્ટને પ્લાન કરવામાં નિષ્ફળ થાઓ છો.

પરફોર્મન્સ-આધારિત ફી: ખર્ચનું અતિરિક્ત સ્તર

કેટલાક મ્યુચ્યુઅલ ફંડ, ખાસ કરીને હેજ ફંડ જેવા માળખાઓ અથવા વિશિષ્ટ ઇન્વેસ્ટમેન્ટ ટીમો દ્વારા સંચાલિત, સ્ટાન્ડર્ડ એક્સપેન્સ રેશિયો ઉપરાંત પરફોર્મન્સ-આધારિત ફી લાગુ કરે છે. આ ફી સામાન્ય રીતે ચોક્કસ બેંચમાર્ક અથવા "અવરોધ દર" ઉપર પેદા થતા વળતરની ટકાવારી છે

પરફોર્મન્સ માટે ચુકવણી કરવાનો વિચાર યોગ્ય લાગી શકે છે, ત્યારે ડિલિવર કરેલા રિટર્ન દ્વારા વધારાનો ખર્ચ યોગ્ય છે કે નહીં તેનું મૂલ્યાંકન કરવું જરૂરી છે. મોટાભાગના રોકાણકારો માટે, સરળ ફી સ્ટ્રક્ચર સાથે ઓછા ખર્ચે ફંડ વધુ અંદાજિત અને ખર્ચ-અસરકારક વિકલ્પ પ્રદાન કરે છે.

છુપાયેલ વિતરણ ખર્ચ: ફંડ વેચાણ માટે ચુકવણી

ઘણા રોકાણકારો એમ્બેડેડ ડિસ્ટ્રિબ્યુશન ખર્ચ વિશે અજાણ છે જે મ્યુચ્યુઅલ ફંડ તેમના એકમોને માર્કેટિંગ અને વેચવા માટે થાય છે. આ ખર્ચને ઘણીવાર વિતરકો અથવા સલાહકારોને ચૂકવવામાં આવતા "કમિશન" તરીકે લેબલ કરવામાં આવે છે જે રોકાણકારોને ભંડોળની ભલામણ કરે છે. જ્યારે કમિશન પોતાને સીધા તમને ચાર્જ કરવામાં આવતું નથી, ત્યારે તે ખર્ચ રેશિયોનો ભાગ બનાવે છે, પરોક્ષ રીતે તમારા રિટર્નને ઘટાડે છે.

ડાયરેક્ટ પ્લાન, જે મધ્યસ્થી કમિશનને દૂર કરે છે, નિયમિત પ્લાન માટે ખર્ચ-અસરકારક વિકલ્પ પ્રદાન કરે છે. ડાયરેક્ટ પ્લાનમાં ઇન્વેસ્ટ કરીને, તમે વિતરણ ખર્ચ પર બચત કરી શકો છો અને લાંબા ગાળે ઉચ્ચ રિટર્નનો આનંદ માણી શકો છો.

ગેરમાર્ગે દોરનારા પ્રોત્સાહનો: અન્ડરપરફોર્મન્સ માટે ચુકવણી

મ્યુચ્યુઅલ ફંડના સૌથી નિરાશાજનક છુપાયેલા ખર્ચમાંથી એક ગેરમાર્ગે દોરવામાં આવેલા પ્રોત્સાહનો માટે સંભવિત છે. સક્રિય રીતે સંચાલિત ફંડ ઘણીવાર તેમની પરફોર્મન્સને ધ્યાનમાં લીધા વિના ઉચ્ચ ફી વસૂલ કરે છે, જે રોકાણકારોને સબપાર પરિણામો માટે ચુકવણી કરવાની ફરજ પાડે છે. સમય જતાં, આ નોંધપાત્ર સંપત્તિમાં ઘટાડો કરી શકે છે, ખાસ કરીને જો તમે સતત અન્ડરપરફોર્મિંગ ફંડમાં રોકાણ કરો છો.

તમારા મ્યુચ્યુઅલ ફંડના પરફોર્મન્સની સમયાંતરે સમીક્ષા કરવી અને જરૂર પડે ત્યારે વધુ સારા પરફોર્મિંગ, ઓછા ખર્ચના વિકલ્પો પર સ્વિચ કરવું મહત્વપૂર્ણ છે. ઇન્ટરશિયાને તમને ફંડમાં લૉક કરવા દેશો નહીં જે પૈસા માટે મૂલ્ય ડિલિવર કરવામાં નિષ્ફળ થાય છે.

તકનો ખર્ચ: કમ્પાઉન્ડિંગ પર ઉચ્ચ ખર્ચની અસર

છેવટે, ઉચ્ચ મ્યુચ્યુઅલ ફંડ ખર્ચ અગાઉથી કમ્પાઉન્ડિંગની દ્રષ્ટિએ તકની કિંમતનું પ્રતિનિધિત્વ કરે છે. ફી, ટૅક્સ અથવા ટ્રાન્ઝૅક્શન ખર્ચ પર ખર્ચ કરેલ દરેક રૂપિયા રિઇન્વેસ્ટમેન્ટ માટે ઓછું ઉપલબ્ધ છે. દાયકાઓથી, આ છુપાયેલા ખર્ચ નોંધપાત્ર રકમમાં વધારો કરી શકે છે, જે તમને તમારા ઇન્વેસ્ટમેન્ટની સંપૂર્ણ ક્ષમતાથી વંચિત કરી શકે છે.

ઉદાહરણ

સ્નેહાની મ્યુચ્યુઅલ ફંડની યાત્રાની વાર્તા

મુંબઈના યુવા માર્કેટિંગ પ્રોફેશનલ સ્નેહાએ તાજેતરમાં જ તેના ફાઇનાન્શિયલ ભવિષ્યને સુરક્ષિત કરવા માટે ઇન્વેસ્ટ કરવાનું શરૂ કર્યું હતું. ઘણા પ્રથમ વખતના રોકાણકારોની જેમ, તેઓ સરળતા અને વ્યાવસાયિક મેનેજમેન્ટના તેમના વચન દ્વારા આકર્ષિત મ્યુચ્યુઅલ ફંડમાં વળ્યા. After researching online and consulting her bank’s advisor, she decided to invest ₹5,00,000 in a popular equity mutual fund. The returns looked promising, and the advisor assured her it was a “safe” choice. Sneha was thrilled to finally take charge of her financial journey, but little did she know, a series of hidden costs were silently eroding her wealth.

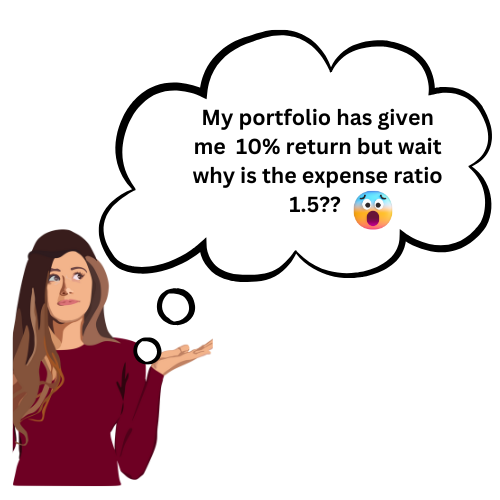

The Expense Ratio Revelation

A year later, Sneha decided to review her investment performance. She noticed that her fund had delivered a decent return of 10%. But when she checked the fine print, she discovered the expense ratio of the fund was 1.5% annually. Initially, Sneha dismissed it as a minor fee, but out of curiosity, she did the math.

Her ₹5,00,000 investment had grown to ₹5,50,000 before expenses. However, 1.5% of the total amount—₹8,250—was deducted as the expense ratio. Over the course of 20 years, Sneha realized, this seemingly small percentage could compound into a significant amount, eating into her returns. She started exploring funds with lower expense ratios, such as index funds, and regretted not paying attention to this detail earlier.

The Exit Load Surprise

Life threw Sneha a curveball when she needed to withdraw a portion of her investment to cover unexpected medical expenses. She redeemed ₹1,00,000 from her mutual fund, only to discover that an exit load of 1% was deducted since she had withdrawn within the first year. This meant she received ₹99,000 instead of the full amount.

Sneha couldn’t help but feel frustrated. She had invested her hard-earned money, only to face a penalty for accessing it when she needed it most. Moving forward, she made a note to consider funds with lower or no exit loads and to understand the lock-in periods before investing.

The Hidden Transaction Costs

Over time, Sneha noticed that her fund’s Net Asset Value (NAV) didn’t always align with her expectations. Despite market growth, her returns seemed slightly lower than anticipated. Upon digging deeper, she learned about the transaction costs incurred by mutual funds.

Her fund had a high portfolio turnover, meaning the fund manager frequently bought and sold stocks to adjust the portfolio. Each transaction incurred brokerage fees and taxes, which were deducted from the fund’s overall returns. These costs weren’t directly visible to Sneha but were quietly embedded in the NAV. She realized that funds with a lower turnover rate might be a better fit for her investment strategy.

Taxes: The Unavoidable Bite

After three years, Sneha sold another portion of her mutual fund investment to fund her sister’s wedding. She was delighted to see substantial long-term gains but soon learned that a portion of these gains would be subject to taxation. The long-term capital gains (LTCG) tax on equity mutual funds—10% on gains above ₹1,00,000—meant she had to part with ₹3,000 in taxes.

Though taxes are inevitable, Sneha understood the importance of factoring them into her investment calculations. She started planning her withdrawals more strategically, aiming to minimize tax liabilities while maximizing her returns.

The Performance Fee Dilemma

Encouraged by her friends, Sneha also explored a niche mutual fund that promised exceptional returns. This fund had a performance-based fee structure, charging an additional fee if returns exceeded 12% annually. While the fund performed well initially, it struggled to sustain its momentum in subsequent years. Yet, the high fees continued to eat into her profits.

Sneha learned an important lesson: higher costs don’t always translate into higher returns. She decided to stick with low-cost funds where the fee structures were simpler and more predictable.

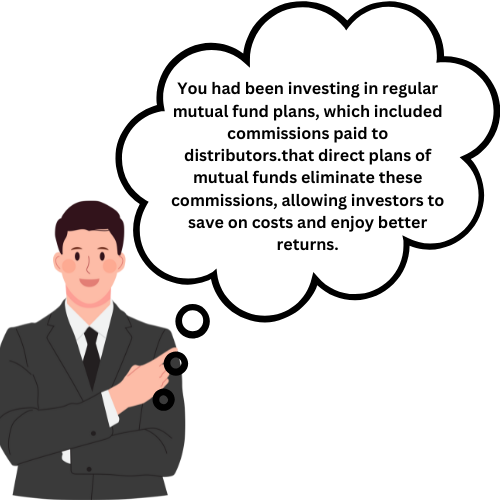

Direct Plans vs Regular Plans

During a casual chat with her colleague Ramesh, Sneha discovered she had been investing in regular mutual fund plans, which included commissions paid to distributors. Ramesh explained that direct plans of mutual funds eliminate these commissions, allowing investors to save on costs and enjoy better returns.

Sneha promptly switched her investments to direct plans. Over the next few years, she saw a noticeable improvement in her returns, simply by avoiding the unnecessary distribution costs embedded in regular plans.

Opportunity Costs of High Fees

Finally, Sneha realized the true opportunity cost of hidden fees. Had she opted for low-cost index funds from the beginning, she could have reinvested the savings from lower fees into additional investments. Over decades, this reinvestment could have compounded into a significant amount.

For instance, by saving ₹5,000 annually on fees and reinvesting it at an 8% annual return, Sneha could have accumulated nearly ₹10,00,000 over 30 years. This realization motivated her to optimize her portfolio and take a more cost-conscious approach to investing.

ટેકઅવે

Sneha’s journey with mutual funds was a mix of ups and downs, filled with valuable lessons about the hidden costs of investing. From expense ratios to taxes and performance fees, each layer of costs taught her the importance of due diligence and informed decision-making.

Today, Sneha is a more confident and savvy investor. She carefully evaluates fund costs, opts for direct plans, and prioritizes low-cost, high-value investments. Her story serves as a reminder to all investors: don’t let hidden costs erode your wealth. Take the time to understand where your money is going, and make every rupee count.

નિષ્કર્ષ

જ્યારે મ્યુચ્યુઅલ ફંડ ઘણા લોકો માટે એક શ્રેષ્ઠ ઇન્વેસ્ટમેન્ટ વાહન રહે છે, ત્યારે તમારા રિટર્નને નષ્ટ કરી શકે તેવા છુપાયેલા ખર્ચ વિશે જાગૃત રહેવું જરૂરી છે. એક્સપેન્સ રેશિયો, એક્ઝિટ લોડ, ટ્રાન્ઝૅક્શન ખર્ચ, ટૅક્સ અને અન્ય ફીને સમજીને, તમે માહિતગાર નિર્ણયો લઈ શકો છો અને તમારા ઇન્વેસ્ટમેન્ટ પોર્ટફોલિયોને ઑપ્ટિમાઇઝ કરી શકો છો. Opt for low-cost funds, invest in direct plans, and periodically review your fund performance to ensure that you’re not paying more than you think.