11.1 What is the clearing and settlement process

Nirav: Vedant, I clicked “Buy” on a stock yesterday and saw it in my portfolio today. It felt instant—how does that work so fast?

Vedant: It feels What is the clearing and settlement process in the share market?instant, but there’s a whole system running quietly behind the scenes. The trade has to be cleared and settled properly.

Nirav: You mean like paperwork?

Vedant: Not anymore! Today, it’s digital and follows something called a T+1 cycle—your trade gets settled the very next working day. Behind that smooth process are clearing corporations and depositories making sure money and shares move safely. Nirav: So even though it looks quick on my app, there’s a well-managed process ensuring I get my shares and the seller gets their money?

Vedant: Exactly. Think of it like a backstage crew making sure your trading show runs smoothly—even if you don’t see them, they’re essential.

So,

The clearing and settlement process is like what happens when you buy groceries online. You click the buy button. It feels like the groceries are going to be at your door right away.. There is a lot going on behind the scenes. The store checks if they have the groceries you want they pack them up. Then the delivery person picks them up. The day the groceries are at your door. This all happens because each person does their job and does it well.

The clearing and settlement process in the share market is similar. When you buy shares it looks like it happens away.. The clearing houses and brokers and other people are working together to make sure the shares and money are transferred correctly. This all happens by the day, which is called T+1. It is like how your groceries get to your door after everyone does their part.

The clearing and settlement process is what makes it possible for you to buy and sell shares on your computer or phone. When you click the buy or sell button it feels like it happens instantly.. There is a lot going on behind the scenes to make sure everything works correctly. The clearing and settlement process makes sure that money and shares are transferred without any mistakes or cheating. This is what allows millions of people to buy and sell shares every day without worrying.

The Indian share market uses a system called T+1 settlement. This means that when you buy or sell shares the transaction is completed one working day later. This makes everything work efficiently and gives people quicker access to their shares and money. There are companies like NSCCL and ICCL that help make this process work. They make sure that both the buyer and seller do what they are supposed to do.

The process starts when you buy or sell shares. The information about the trade is sent to the clearing corporation, which figures out what each person owes. The clearing corporation also makes sure that people do not take much risk and that everything works smoothly. All of this happens automatically. Is watched closely by regulators.

The settlement is when the shares are actually transferred from the seller to the buyer and the money is transferred from the buyer to the seller. This is done by companies like NSDL and CDSL which keep track of who owns which shares. On the day of settlement the shares and money are transferred electronically. What makes the Indian system work well is that it only settles the amount that people owe each other. This reduces the number of transactions. Makes everything more efficient.

The clearing and settlement system is like the people who work behind the scenes at a theater. While you are watching the show they are making sure everything works smoothly. If they did not do their job the show would not be good. People would not want to come back. It is the same with the share market. If the clearing and settlement process did not work well people would not trust the market. Would not want to buy and sell shares.

Nirav: I have heard people say that the market is structured. What does that mean? Is it people buying and selling shares?

Vedant: No it is more, than that. The market has parts that work together to make sure everything works smoothly and is safe. These parts include the exchanges, brokers, clearing houses and depositories. All of these parts working together are what make up the market structure. The market structure is what makes it possible for people to buy and sell shares with confidence. The clearing and settlement process is a part of the market structure. It is what makes sure that shares and money are transferred correctly and that everything works smoothly.

11.2 What is Market Structure?

The stock market works like a team effort to make buying and selling smooth and safe. At the center are stock exchanges like NSE and BSE, where people place and match orders electronically. When a trade happens a clearing corporation like NSCCL makes sure both the buyer and seller do what they agreed to do. This corporation acts as a middleman to both sides ensuring the deal goes through even if one side changes their mind. Depositories like NSDL and CDSL hold the shares in a digital form and keep track of who owns what. Each part works together to make sure trading is trustworthy, clear and efficient.

Rohan wants to buy Infosys shares. He places an order through 5paisa his broker, which sends the order to NSE. The exchange finds a matching sell order. Makes the trade happen. NSCCL steps in to ensure the deal goes through even if one party does not follow through. CDSL holds the shares. Updates Rohans account to show he now owns them. Each step from broker to exchange to clearing to depository helps make the trade happen.

Nirav: Hey Vedant, when I tap “Buy” on my app what really happens?

Vedant: It starts a series of steps. Your broker sends the order to the exchange, where it matches with a sell order and behind the scenes the money and shares get ready to be swapped the day.

11.3 What Happens When You Buy a Stock?

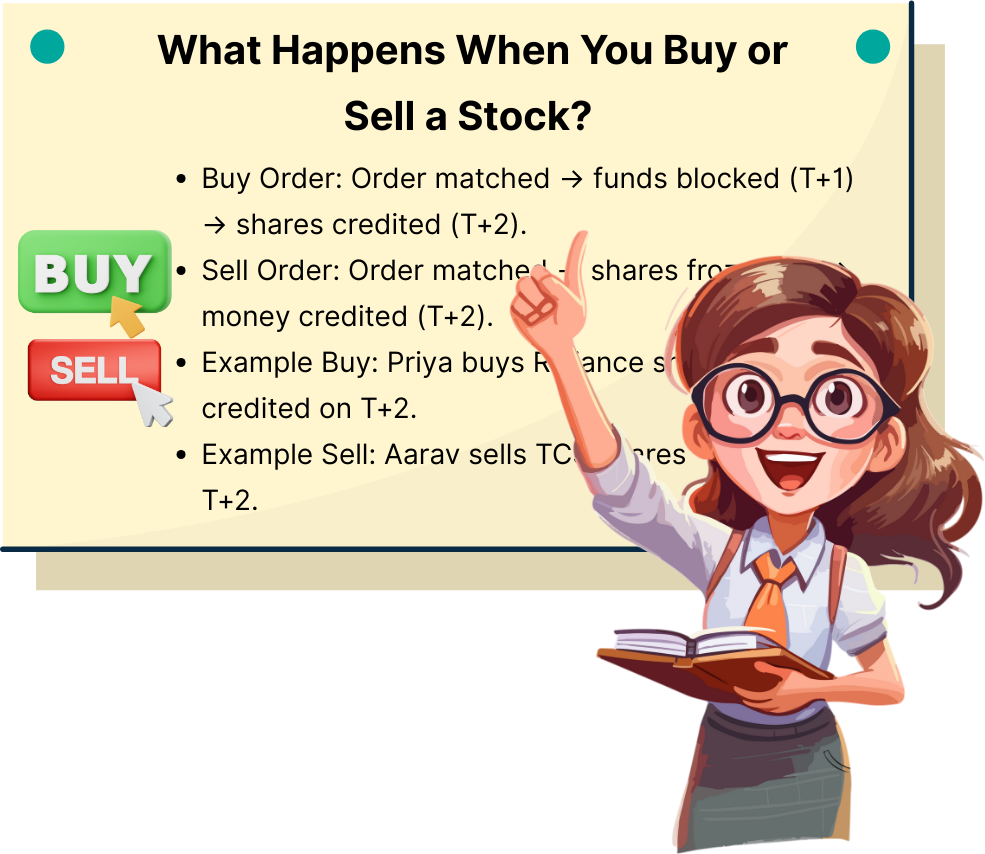

When you place a buy order through your broker or trading app it goes to the stock exchange. Once it matches with a sellers price a trade is made.. That’s just the start. On the business day (T+1) your money is set aside for that trade. The clearing corporation makes sure everyone does their part. By T+2 the depository, either NSDL or CDSL adds the shares to your account. So even though it seems instant all the work happens over two days.

Lets say Priya buys 100 Reliance shares at ₹2,800 each. On the trade day (T) the exchange matches her order. On T+1 ₹2,80,000 is set aside in her bank account. By T+2 NSDL adds those 100 shares to her account. Priya now officially owns the shares. It took two days and many, behind-the-scenes helpers to make it happen.

Say Priya buys 100 shares of Reliance at ₹2,800 each. On trade day (T), the exchange matches her order. On T+1, ₹2,80,000 is earmarked (blocked) in her bank account. By T+2, NSDL credits those 100 shares into her demat account. Priya now officially owns the shares, but the actual transfer took two days and multiple entities working behind the scenes to complete.

Nirav: Selling feels just as easy. I tap “Sell” and the amount shows up soon. What’s going on in the backend?

Vedant: When you sell, your shares get locked, the exchange finds a buyer, and once matched, the clearing process kicks in. Your shares go out and money comes in—all tightly tracked.

11.4 What Happens When You Sell a Stock?

Selling reverses the buying steps. Once your sell order is matched on the exchange, your demat account is earmarked for the quantity of shares sold. These shares are frozen—reserved for transfer. On T+1, the clearing corporation ensures the buyer has the funds and you have the shares. On T+2, your shares are debited from your account, and your bank account is credited with the proceeds. It’s a trust-driven relay where each entity passes the baton seamlessly.

Suppose Aarav decides to sell 50 shares of TCS. He places the order on a Monday. Once matched, those 50 shares are earmarked in his demat account—frozen for delivery. By Wednesday (T+2), NSCCL ensures the buyer has paid, and the shares are debited from Aarav’s account. That evening, his bank account receives the money, say ₹1,75,000. To him, it’s a quick trade—but the machinery that made it happen ran a tight, regulated schedule.

Nirav: Vedant, my app said “Shares earmarked for selling.” What does that even mean?

Vedant: That means your shares are temporarily marked or reserved for that trade. It stops you from selling them again while the settlement is being completed.

11.5 What is Earmarking?

Earmarking is the process of reserving resources—either funds or shares—specifically for a trade that’s already been executed but not yet settled. For a buyer, earmarking blocks the exact amount needed in your bank account so the money can be transferred on T+2. For a seller, it freezes the relevant shares in your demat account so they can’t be sold again or transferred elsewhere. It’s like placing a tag on items in a store marked “SOLD”—you still possess them, but they’re off-limits until the buyer picks them up.

Let’s say Simran wants to sell her 25 shares of HDFC Bank. When she places the sell order, these 25 shares are earmarked by CDSL. Even though the shares remain in her demat account, she can’t transfer or sell them elsewhere—they’ve been tagged for this specific settlement. It ensures that when the buyer comes calling on T+2, those shares are ready to go—no surprises, no delays.

Nirav: Vedant I must say. I find it really interesting to know how trades are settled and how the system keeps everything balanced. It’s like there is a safety net that works behind every trade. I mean think about it every trade that happens it all gets settled properly. The system makes sure that everything is, in order.

Vedant: Exactly. Most traders don’t realize the effort that goes into making a simple “buy” or “sell” look effortless. Clearing, settlement, and market structure are the silent engines of trust.

Nirav: So now that the trade is done and settled, what’s next for a stockholder? Vedant: This is where corporate actions come in—dividends, bonus shares, splits, mergers. All these decisions made by companies directly affect stock prices and investor value.

Nirav: I’ve seen news flashes like “XYZ announces 1:2 bonus issue.” Does that mean I get extra shares?

Vedant: That’s right. These actions change the number of shares you hold or the value per share—but your overall investment stays balanced.

11.1 What is the clearing and settlement process

Nirav: Vedant, I clicked “Buy” on a stock yesterday and saw it in my portfolio today. It felt instant—how does that work so fast?

Vedant: It feels What is the clearing and settlement process in the share market?instant, but there’s a whole system running quietly behind the scenes. The trade has to be cleared and settled properly.

Nirav: You mean like paperwork?

Vedant: Not anymore! Today, it’s digital and follows something called a T+1 cycle—your trade gets settled the very next working day. Behind that smooth process are clearing corporations and depositories making sure money and shares move safely. Nirav: So even though it looks quick on my app, there’s a well-managed process ensuring I get my shares and the seller gets their money?

Vedant: Exactly. Think of it like a backstage crew making sure your trading show runs smoothly—even if you don’t see them, they’re essential.

So,

The clearing and settlement process is like what happens when you buy groceries online. You click the buy button. It feels like the groceries are going to be at your door right away.. There is a lot going on behind the scenes. The store checks if they have the groceries you want they pack them up. Then the delivery person picks them up. The day the groceries are at your door. This all happens because each person does their job and does it well.

The clearing and settlement process in the share market is similar. When you buy shares it looks like it happens away.. The clearing houses and brokers and other people are working together to make sure the shares and money are transferred correctly. This all happens by the day, which is called T+1. It is like how your groceries get to your door after everyone does their part.

The clearing and settlement process is what makes it possible for you to buy and sell shares on your computer or phone. When you click the buy or sell button it feels like it happens instantly.. There is a lot going on behind the scenes to make sure everything works correctly. The clearing and settlement process makes sure that money and shares are transferred without any mistakes or cheating. This is what allows millions of people to buy and sell shares every day without worrying.

The Indian share market uses a system called T+1 settlement. This means that when you buy or sell shares the transaction is completed one working day later. This makes everything work efficiently and gives people quicker access to their shares and money. There are companies like NSCCL and ICCL that help make this process work. They make sure that both the buyer and seller do what they are supposed to do.

The process starts when you buy or sell shares. The information about the trade is sent to the clearing corporation, which figures out what each person owes. The clearing corporation also makes sure that people do not take much risk and that everything works smoothly. All of this happens automatically. Is watched closely by regulators.

The settlement is when the shares are actually transferred from the seller to the buyer and the money is transferred from the buyer to the seller. This is done by companies like NSDL and CDSL which keep track of who owns which shares. On the day of settlement the shares and money are transferred electronically. What makes the Indian system work well is that it only settles the amount that people owe each other. This reduces the number of transactions. Makes everything more efficient.

The clearing and settlement system is like the people who work behind the scenes at a theater. While you are watching the show they are making sure everything works smoothly. If they did not do their job the show would not be good. People would not want to come back. It is the same with the share market. If the clearing and settlement process did not work well people would not trust the market. Would not want to buy and sell shares.

Nirav: I have heard people say that the market is structured. What does that mean? Is it people buying and selling shares?

Vedant: No it is more, than that. The market has parts that work together to make sure everything works smoothly and is safe. These parts include the exchanges, brokers, clearing houses and depositories. All of these parts working together are what make up the market structure. The market structure is what makes it possible for people to buy and sell shares with confidence. The clearing and settlement process is a part of the market structure. It is what makes sure that shares and money are transferred correctly and that everything works smoothly.

11.2 What is Market Structure?

The stock market works like a team effort to make buying and selling smooth and safe. At the center are stock exchanges like NSE and BSE, where people place and match orders electronically. When a trade happens a clearing corporation like NSCCL makes sure both the buyer and seller do what they agreed to do. This corporation acts as a middleman to both sides ensuring the deal goes through even if one side changes their mind. Depositories like NSDL and CDSL hold the shares in a digital form and keep track of who owns what. Each part works together to make sure trading is trustworthy, clear and efficient.

Rohan wants to buy Infosys shares. He places an order through 5paisa his broker, which sends the order to NSE. The exchange finds a matching sell order. Makes the trade happen. NSCCL steps in to ensure the deal goes through even if one party does not follow through. CDSL holds the shares. Updates Rohans account to show he now owns them. Each step from broker to exchange to clearing to depository helps make the trade happen.

Nirav: Hey Vedant, when I tap “Buy” on my app what really happens?

Vedant: It starts a series of steps. Your broker sends the order to the exchange, where it matches with a sell order and behind the scenes the money and shares get ready to be swapped the day.

11.3 What Happens When You Buy a Stock?

When you place a buy order through your broker or trading app it goes to the stock exchange. Once it matches with a sellers price a trade is made.. That’s just the start. On the business day (T+1) your money is set aside for that trade. The clearing corporation makes sure everyone does their part. By T+2 the depository, either NSDL or CDSL adds the shares to your account. So even though it seems instant all the work happens over two days.

Lets say Priya buys 100 Reliance shares at ₹2,800 each. On the trade day (T) the exchange matches her order. On T+1 ₹2,80,000 is set aside in her bank account. By T+2 NSDL adds those 100 shares to her account. Priya now officially owns the shares. It took two days and many, behind-the-scenes helpers to make it happen.

Say Priya buys 100 shares of Reliance at ₹2,800 each. On trade day (T), the exchange matches her order. On T+1, ₹2,80,000 is earmarked (blocked) in her bank account. By T+2, NSDL credits those 100 shares into her demat account. Priya now officially owns the shares, but the actual transfer took two days and multiple entities working behind the scenes to complete.

Nirav: Selling feels just as easy. I tap “Sell” and the amount shows up soon. What’s going on in the backend?

Vedant: When you sell, your shares get locked, the exchange finds a buyer, and once matched, the clearing process kicks in. Your shares go out and money comes in—all tightly tracked.

11.4 What Happens When You Sell a Stock?

Selling reverses the buying steps. Once your sell order is matched on the exchange, your demat account is earmarked for the quantity of shares sold. These shares are frozen—reserved for transfer. On T+1, the clearing corporation ensures the buyer has the funds and you have the shares. On T+2, your shares are debited from your account, and your bank account is credited with the proceeds. It’s a trust-driven relay where each entity passes the baton seamlessly.

Suppose Aarav decides to sell 50 shares of TCS. He places the order on a Monday. Once matched, those 50 shares are earmarked in his demat account—frozen for delivery. By Wednesday (T+2), NSCCL ensures the buyer has paid, and the shares are debited from Aarav’s account. That evening, his bank account receives the money, say ₹1,75,000. To him, it’s a quick trade—but the machinery that made it happen ran a tight, regulated schedule.

Nirav: Vedant, my app said “Shares earmarked for selling.” What does that even mean?

Vedant: That means your shares are temporarily marked or reserved for that trade. It stops you from selling them again while the settlement is being completed.

11.5 What is Earmarking?

Earmarking is the process of reserving resources—either funds or shares—specifically for a trade that’s already been executed but not yet settled. For a buyer, earmarking blocks the exact amount needed in your bank account so the money can be transferred on T+2. For a seller, it freezes the relevant shares in your demat account so they can’t be sold again or transferred elsewhere. It’s like placing a tag on items in a store marked “SOLD”—you still possess them, but they’re off-limits until the buyer picks them up.

Let’s say Simran wants to sell her 25 shares of HDFC Bank. When she places the sell order, these 25 shares are earmarked by CDSL. Even though the shares remain in her demat account, she can’t transfer or sell them elsewhere—they’ve been tagged for this specific settlement. It ensures that when the buyer comes calling on T+2, those shares are ready to go—no surprises, no delays.

Nirav: Vedant I must say. I find it really interesting to know how trades are settled and how the system keeps everything balanced. It’s like there is a safety net that works behind every trade. I mean think about it every trade that happens it all gets settled properly. The system makes sure that everything is, in order.

Vedant: Exactly. Most traders don’t realize the effort that goes into making a simple “buy” or “sell” look effortless. Clearing, settlement, and market structure are the silent engines of trust.

Nirav: So now that the trade is done and settled, what’s next for a stockholder? Vedant: This is where corporate actions come in—dividends, bonus shares, splits, mergers. All these decisions made by companies directly affect stock prices and investor value.

Nirav: I’ve seen news flashes like “XYZ announces 1:2 bonus issue.” Does that mean I get extra shares?

Vedant: That’s right. These actions change the number of shares you hold or the value per share—but your overall investment stays balanced.