4.1 What Is A Primary Market & Functions Of Primary Market

So by now you must have an idea about Market Intermediaries, the types of Market Intermediaries, their roles and who regulates Market Intermediaries.

As Vedant had promised Nirav to discuss the Primary Market they meet again and the learning continues.

Nirav: Vedant, whatever you explained till now was really helpful. You explained things in a clear way. I really appreciate you taking the time to explain these topics in detail Primary Market topics.

Vedant: I am glad to hear that Nirav. I am really happy that the explanation helped you understand Primary Market. The securities market can seem complicated at first. Once you break it down it starts making sense. So today as promised lets discuss the Primary Market.

What Is A Primary Market & Functions Of Primary Market

Vedant: Have you heard about the term “Go Public” related to Primary Market?

Nirav: No. Does it mean a company is open for debate about Primary Market?

Vedant: No, no. It means securities are created and sold for the time in the Primary Market.

Nirav: Oh sounds interesting. Please explain the Primary Market.

Vedant: Securities are. First time in the Primary Market.

So Primary Market is a segment of capital market where corporations, governments or institutions raise capital by issuing new securities directly to investors in Primary Market. In terms the Primary Market is where new securities are issued for the very first time. It’s the starting point in the life cycle of an asset. Whether it’s a stock, bond or other instrument related to Primary Market.

What are the functions of the Primary Market?

Formation of Capital: It provides companies/government/organizations access to finance for growth, operations, and infrastructural development.

Direct Deals: The investors are able to deal in securities without going through intermediaries in the Primary Market.

Price Discovery: Price discovery is another benefit where a fair value for securities can be determined based on various parameters.

Government Regulations: Primary Markets come under the regulation of government authorities such as Securities Exchange Board of India in the case of India, which compels organizations to make certain disclosures in the process.

Diversified Investment Opportunity for the Investors: Primary Market provides investors with diversified investment options, especially in emerging sectors. This could include technology, renewable sector, or healthcare firms.

Nirav: What exactly happens in the Primary Market? How are funds raised in the Primary Market?

Vedant: Okay lets understand methods of raising capital with examples for clearing your doubts, about the Primary Market.

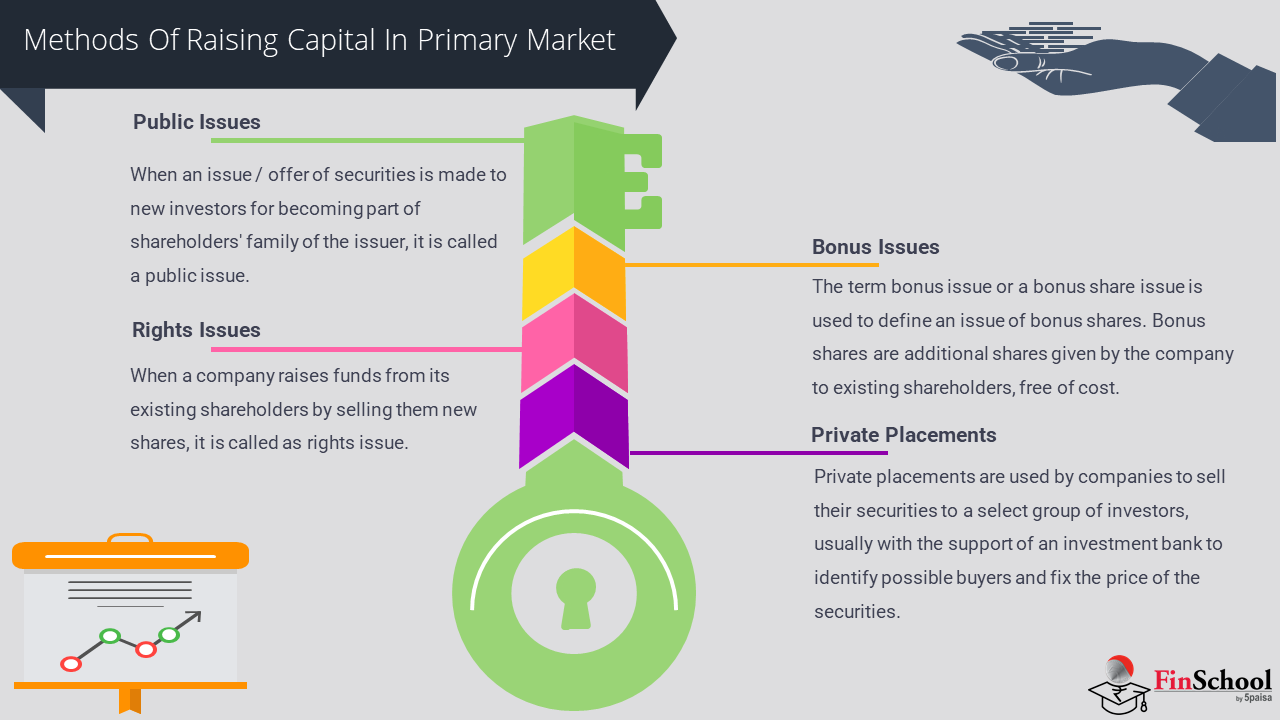

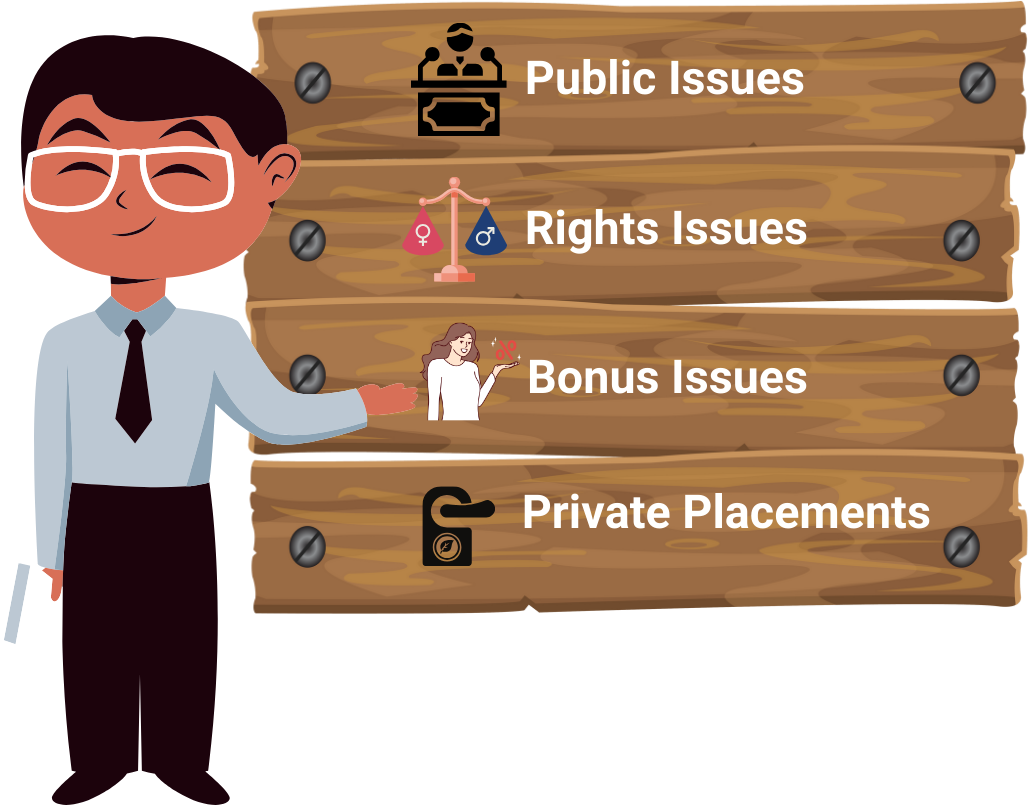

4.2 Different Methods Of Raising Capital In Primary Market

In the primary market companies raise capital in several ways each with its own rules and regulations. Here is a detailed breakdown of the methods:

-

Initial Public Offer (IPO) :

When a company wants to raise money from the public for the time it uses an Initial Public Offering. This is when an unlisted company sells its shares to the public. The company makes a plan gets approval from regulators and decides on a price for the shares. This is a step for a company and it often uses the money to grow pay off debt or get more attention. Initial Public Offer is a way for companies to become publicly traded and raise a lot of money.

-

Follow-on-Public Offering (FPO) :

Follow-on Public Offering is used by companies which are already listed on a stock exchange. These companies sell shares to the public to raise more money. This method is used by companies when they need funds for a large project or for expansion of their business. Follow-on Public Offer can be either sale of shares or sale of existing shareholders’ already owned shares.

-

Rights Issue

A Rights Issue is when a company offers shares to its existing shareholders at a lower price. The company gives these shares to its existing shareholders based on how shares they already own. This way the company can raise money without losing control to investors. Rights Issue is often used when a company needs money quickly or when it is restructuring.

-

Bonus Issue

A Bonus Issue is when a company gives shares to its existing shareholders without charging them. The company uses its money to do this. Although it does not raise money it helps the shareholders and makes the stock more liquid. Bonus Issue is often used when a company has made a lot of money but wants to invest it of giving it to shareholders as dividends.

5. Private Placement

Private Placement is when a company sells its shares directly to a group of investors. This method is faster. Has fewer rules than selling shares to the public. Companies use Private Placement to raise money especially when the market is not stable.

6. Preferential Allotment

A Preferential Allotment is when a company sells its shares to investors at a set price. This method is often used to bring in investors or to raise money from people who already own shares in the company.

7. Qualified Institutional Placement

The Qualified Institutional Placement is a way for companies to raise money from big investors, like banks and insurance companies. This method is regulated to ensure that only big investors participate. Qualified Institutional Placement is a way for listed companies to raise money without having to follow many rules.

Nirav : Vedant can you please explain each type with examples. It becomes easy to understand

Vedant : Ok so let us understand each category in detail with examples.

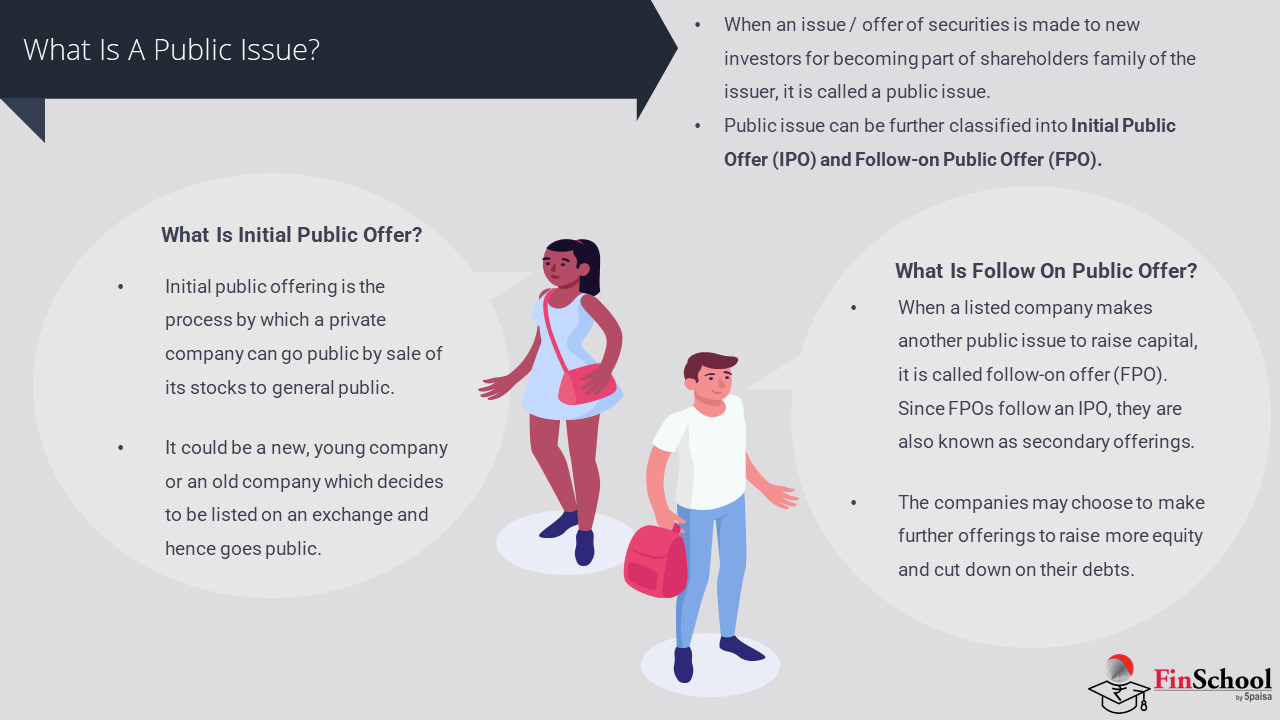

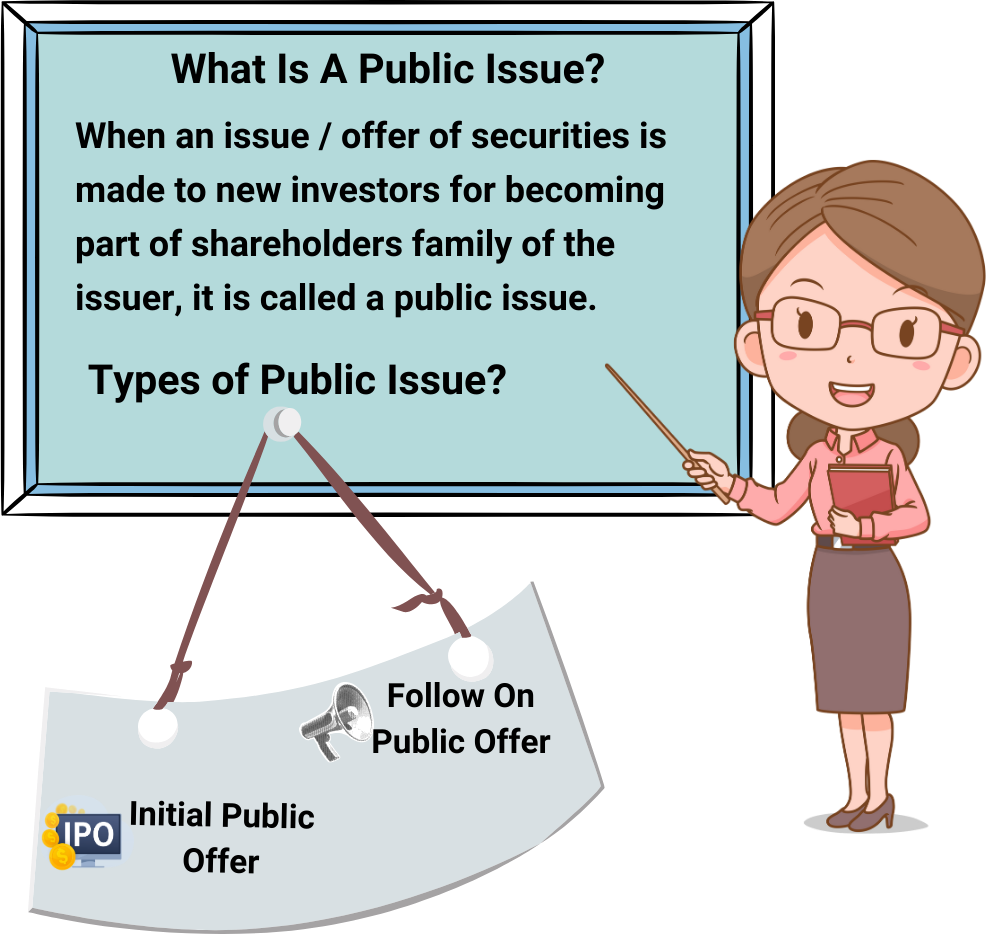

4.3 Public Issue

When a private company decides to sell its shares to the public for the time that is called an Initial Public Offering or IPO. This means the company is now a traded entity that people can buy and sell shares in. The company can now get money from investors. The people who invested in the company on can also sell their shares if they want to.

For example lets say there is a company called GreenGrid. It used to be like a club where only a few people could invest. Now they are opening it up to the public so anyone can buy shares. They are selling some of their shares to investors like you and me. So if you buy those shares you become a part-owner of GreenGrid. If you buy shares of GreenGrid you own a piece of the company. If GreenGrid grows and does well your shares could become more valuable. GreenGrid might also pay dividends to its shareholders in the future. Buying shares of GreenGrid is like getting in on the ground floor of something exciting. However there are risks involved so you need to read the prospectus and understand the business before investing in GreenGrid. The prospectus is a document that has detailed information about GreenGrids business, financial health, risks and plans for the money raised from the IPO.

Why does an Initial Public Offering like GreenGrid happen?

The company is looking to raise funds for expansion, debt repayment or investment in projects.Liquidity is provided by the fact that some of the shares of the founders and early investors of GreenGrid can be sold. GreenGrid being a company gives it more credibility and transparency, which is good for its brand and credibility. The IPO gives GreenGrid a market-driven valuation, which means its worth is determined by the market.

IPO Process Overview

- The company in this case GreenGrid appoints investment bankers, lawyers, auditors and registrars to help with the IPO process.

- They do their diligence and create a Draft Red Herring Prospectus or DRHP which is a document that has information about the IPO.

- GreenGrid promotes the IPO to investors , meaning they tell people about the opportunity to buy shares .

- Approves the offer , meaning they make sure everything is okay with the IPO . Investors bid in a range of prices. Price is determined by demand.

- The subscription period is generally 3-5 days during which investors can apply to buy shares through ASBA.

- Shares of GreenGrid are allotted based on demand and category and they are listed on the exchange.

Follow-on Public Offer (FPO)

You might be wondering, what if GreenGrid needs money after its IPO? That’s where a Follow-on Public Offer or FPO comes in. An FPO is like GreenGrid topping up its funds. They have already gone public. They need more capital to grow.

An FPO is an offering to raise capital. Its like an IPO but for companies that are already listed. If GreenGrid issues shares it might affect the price or ownership of the company.

Types of FPOs:

- Dilutive FPOs means a company, say GreenGrid, issues shares. This increases the shares outstanding. It can dilute the ownership of existing shareholders. Earnings per share can also fall. This they do to fund growth, to repay debt or to strengthen their balance sheet. An example is GreenGrid which might issue shares to raise capital for a new project.

- Non-Dilutive Shares are when existing shareholders of GreenGrid sell their holdings to the public. No new shares are created,. The number of shares remains the same. This strategy doesn’t create capital for GreenGrid. It might help the company meet regulatory standards or improve stock liquidity.

Uses of an FPO

The main uses of an FPO are:

- Expansion projects

- Debt reduction

- Better working capital

- Meeting requirements

Some key features of an FPO are:

- It requires a prospectus like an IPO and approval from SEBI.

- Shares are usually priced below market to attract investors.

- It may impact the share price of GreenGrid due, to dilution.

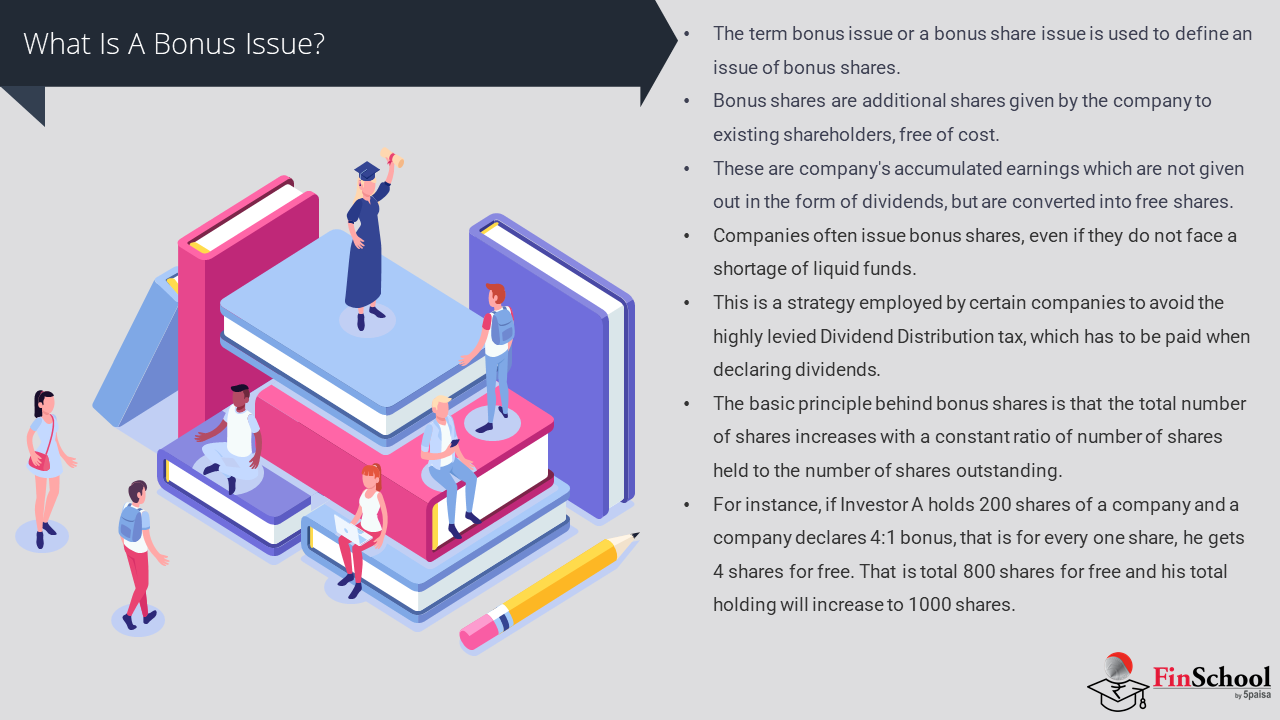

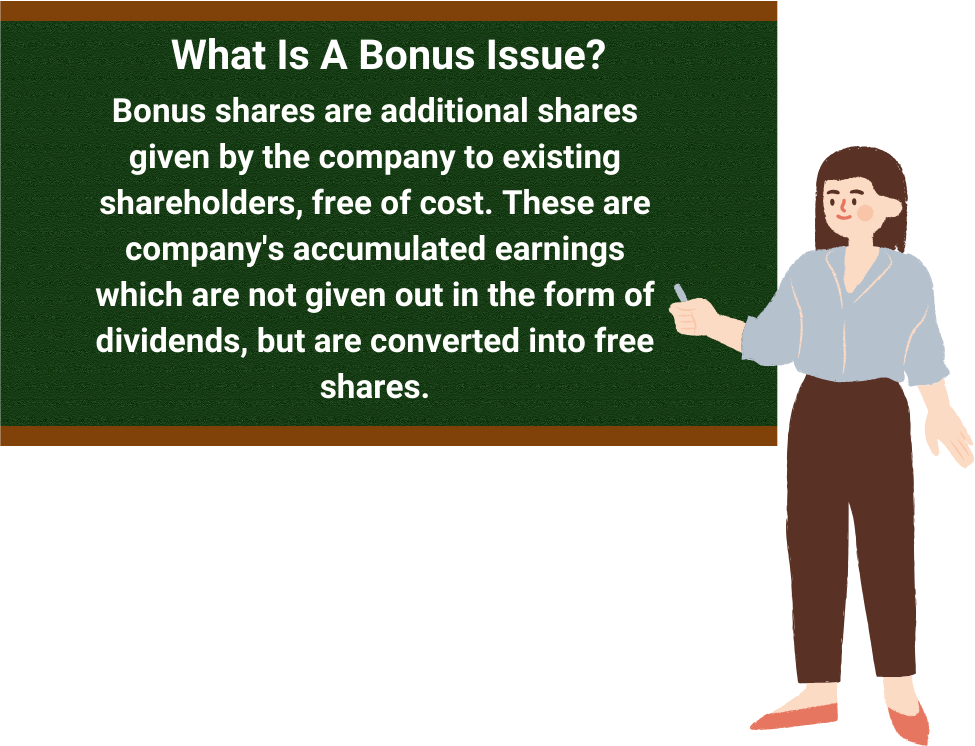

4.4 Bonus Issue

Vedant: “Nirav I just got some shares from a company and I did not have to pay for them.That is a bonus issue. The company is saying thank you for keeping your money invested with them. They are giving you shares instead of giving you cash.”

Nirav: “So you got shares for free and now you have shares?”

Vedant: “That is right. It helps people buy and sell shares easily and it means the company thinks it will make more money in the future.”

So

A Bonus Issue is when a company gives its shareholders shares without taking any money from them. They do this based on how shares the shareholders already have.

Mechanism:

When a company gives bonus shares it uses the money it made in the past that it did not give to shareholders as cash. This money is like a savings account for the company. The company decides to put this money into shares of giving it to shareholders as cash. The company gives these shares to its shareholders based on a plan. For example if the plan is one extra share for every share you already have that is what you get. If the plan is two shares, for every share you have then you get that. This does not change how cash the company has but it does change how many shares are out there which can make it easier for people to buy and sell shares. It also shows that the people running the company think it will do well in the run.

Purpose:

- The company wants to show that it has a lot of money

- The company wants to make it easier for people to buy and sell shares by lowering the price of each share

- The company wants to say thank you to the people who have been invested for a time

Impact:

- The total value of the company does not change

- The price of each share and the amount of money each share earns goes down after the bonus issue

- Each shareholder still owns the percentage of the company, which is bonus issue. The bonus issue does not change this.

4.5 Rights Offering

Nirav: “I was talking to a friend who buys shares. He told me his company is selling him new shares for a lower price. What is happening?”

Vedant: “This is called a rights issue. Since you already own shares in the company they are giving you a chance to buy shares usually for a cheaper price before they sell them to other people.”

Nirav: “Why do companies do this?”

Vedant: “It helps them get money while making sure the people who already own shares in the company have a chance to buy more. You can buy shares if you want to but you do not have to.”

So

a rights issue is when a company lets people who already own shares buy shares for a lower price, based on how many shares they already own.

The main reason, for a rights issue is to

- Get money without letting outsiders control the company

- Pay for things the company wants to buy pay off debts or help the company grow

Some important things to think about when it comes to a rights issue are

- The company needs to get permission from the board of directors and the shareholders

- The company has to follow the rules made by the Securities and Exchange Board of India

- The company has to decide how many new shares to sell to each shareholder and how much to charge for them because this will affect how investors react to the rights issue and whether or not they want to buy shares in the company.

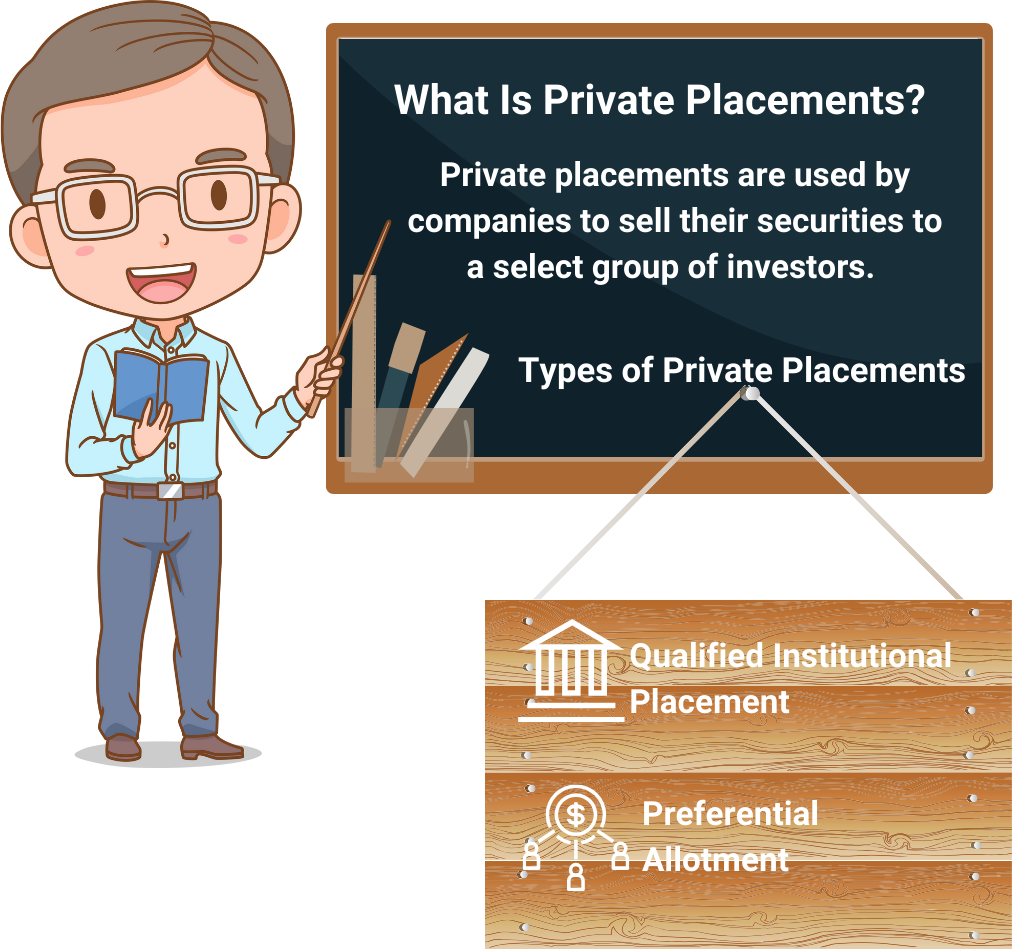

4.6 Private Placement

A private placement refers to the issuance of a company’s securities to very few investors and is not open to the general public. Nirav: I heard startup got money but did not go public. How is that possible?

Vedant: “That’s placement. Instead of public issue they went directly to some investors like banks or rich people.

Nirav : ” So it is faster and has rules ?

Vedant: “Yeah. It is good when companies want to keep things secret or need money quickly without all the trouble of an issue.”

The company can sell kinds of securities like equity shares, preference shares and debentures to these select investors. This helps the company get the money it needs in the way that’s best for them and the investors. The process begins when the company issues a Private Placement Offer Letter to the selected investors. The letter is intended to inform the investors of the offer. The company cannot make this offer to the public. The company needs to get some papers approved by its board and shareholders before it can send the letter. The investors must pay the money from their bank account so everything is clear and easy to see. Private Placement has some things about it. It is faster. Has fewer rules than a public issue. The company can also make the offer in a way that’s just right for the investors it wants. Private Placement also has some limits. The company cannot tell everyone about the offer. Ask people to join. The company has to keep a list of all the investors it has offered the securities to.

What are PAS-4 and PAS-5?

PAS-4 and PAS-5 are forms that companies, in India have to use when they do a placement. These forms are part of the Companies Act and the Companies rules. They help make sure that private placements are done correctly.

4.7 Qualified Institutional Placement

Qualified Institutional Buyers include:

- Mutual funds

- Insurance companies

- Pension funds

- Banks

Nirav said: “I saw a company raise money from big institutions no public offer. What is that?”

Vedant said: “That is a Qualified Institutional Placement. It is a route for listed companies to raise capital from institutional players like mutual funds or insurance companies.”

Nirav said: “Why not include investors in a Qualified Institutional Placement?”

Vedant said: “Because Qualified Institutional Placements involve financially savvy buyers and do not require lengthy disclosures. It is efficient. Often helps stabilize Qualified Institutional Buyers confidence.”

So

A Qualified Institutional Placement is a capital raising tool for listed companies to issue securities to Qualified Institutional Buyers without undergoing regulatory procedures.

Features of a Qualified Institutional Placement are:

- Faster than a Follow On Public Offer or a Rights Issue

- No need for Securities and Exchange Board of India approval to compliance with Issues of Capital and Disclosure Requirements regulations

- Pricing based on market price over preceding weeks

Benefits of a Qualified Institutional Placement are:

- Efficient access to institutional capital for listed companies

- Minimal dilution due to targeted issuance to Qualified Institutional Buyers

- Enhances credibility and visibility among Qualified Institutional Buyers

Nirav said: “So who are the participants of the Primary Market?”

Vedant said: “There are participants to the Primary Market. Let us understand each of the participants, in detail.”

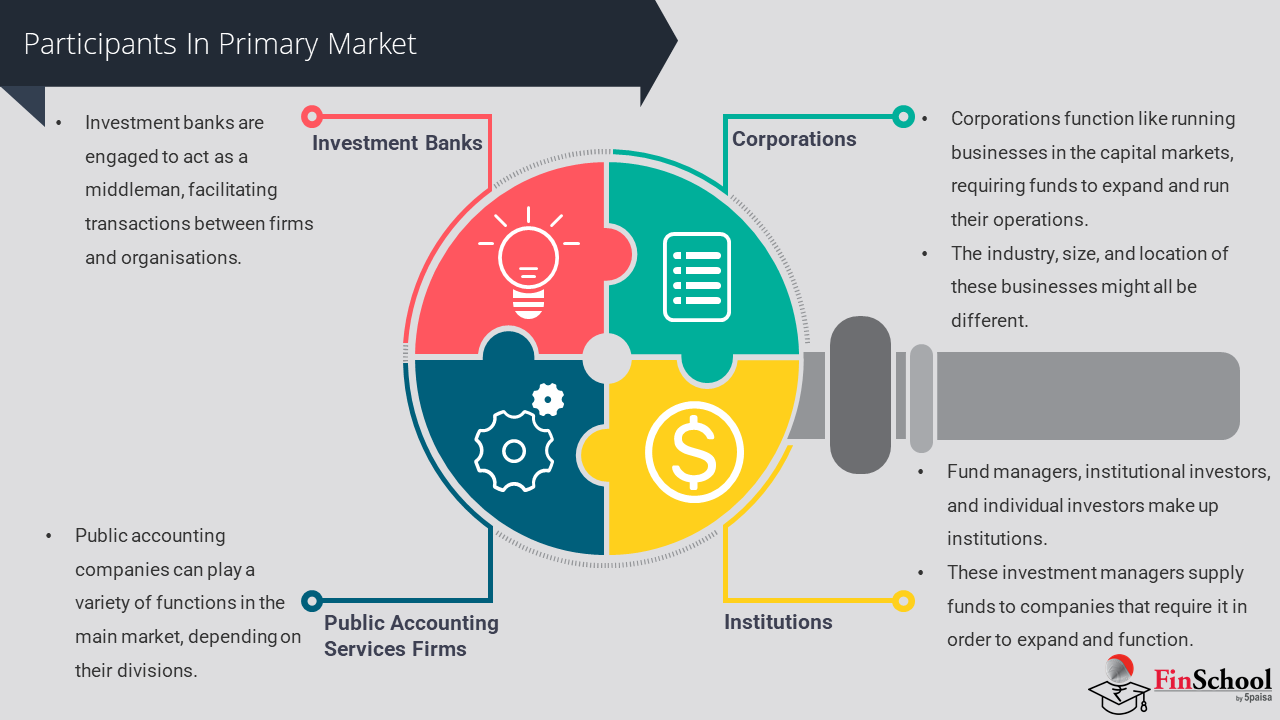

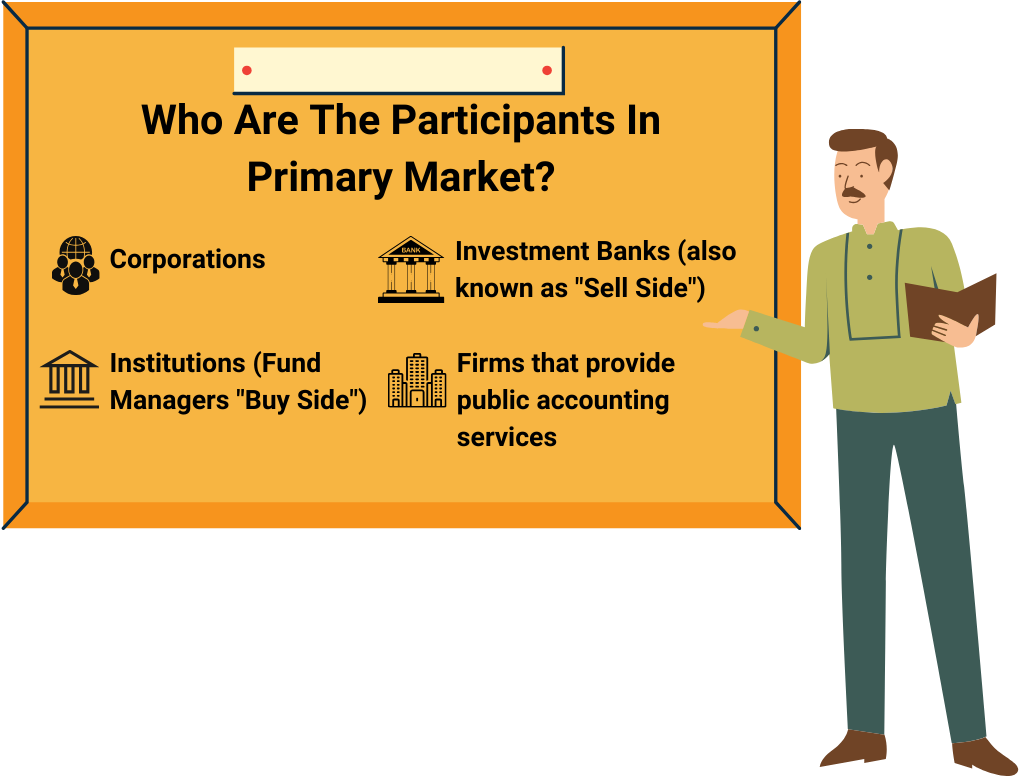

4.8 Participants In Primary Market

Think of the primary market like organizing a big wedding. You have the couple i.e. the company ready to begin a new financial journey, and they need support to bring their big plans to life. The event planner creates and puts in place an ideal party environment; investors bring their gifts ,and the venue provides for properly regulated and lawfully executed events. In a wedding, all participants contribute to the success of the event.In the primary market, a diverse range of participants, including but not limited to issuers, underwriters, and regulators, cooperate to provide an efficient mechanism for issuing new securities and investing back into them.

The primary market has various players who work together to facilitate the issuance and subscription of new securities. Each player has a specific role to play to ensure that the capital formation takes place in an efficient, transparent and regulated manner. Here’s a detailed breakdown: Issuers Suppose you want to start a new restaurant and need some money. You prepare a business plan, decide whether to take a loan or sell a stake of your ownership and invite people to invest. You are the issuer – seeking capital to expand or stabilize your operations.

Issuers

The issuers are the bodies, generally the companies, governments or public sector undertakings, who wish to raise capital and issue securities such as shares, debentures or bonds. They initiate the process by preparing the offer documents, deciding the type of instrument to be issued and the terms of the offer. Their objective may be funding expansion, repaying debt or meeting regulatory requirements, etc.

Merchant Bankers (Lead Managers)

Consider them as your consultant when you start that restaurant. They help you decide how much funding you need, draft legal paperwork, talk to government agencies for permits, and even figure out when to launch for maximum attention. They manage everything behind the scenes.Merchant bankers are financial institutions registered with SEBI to manage the issue . They conduct due diligence , prepare the prospectus , liaise with regulators and supervise the entire issuance process . They also advise on pricing , timing and targeting of investors .In many cases, they act as underwriters, committing to subscribe to unsold portions of the issue.

Underwriters

Suppose you’re selling 100 pre-order vouchers for your restaurant. A friend promises to buy any leftover vouchers if others don’t, just because your opening day doesn’t flop. That friend is the underwriter, ensuring you get the cash regardless of demand.The underwriters bear the risk of the offering by guaranteeing that a certain fraction will be subscribed. If the public does not subscribe fully, the underwriters buy the remaining shares, so that the issuer gets the desired capital.Underwriting may be done by banks, financial institutions, or merchant bankers.

Registrars and Transfer Agents (RTAs)

Think of them like the organizers handling RSVP forms (These forms help organizers know who’s coming, how many guests they’re bringing, and any special needs they might have—like dietary restrictions or accessibility requirements.) and meal preferences at your wedding.They collect guest details, check everything is correct and deliver the right meals. For securities they manage who applied, who got allotment and update records. RTAs manage the logistics of the issue, which includes collecting applications, verifying investor details, and overseeing allotment and refunds. They trade and own securities after they have been issued. Their work is critical for accuracy and transparency in investor servicing.

Bankers to the Issue

These are the cash counters at your event or donation desk. People walk in to pay or register and these guys manage the money—making sure it goes to the right account, handling refunds, and keeping transaction clarity. The set of designated banks to collect the application money from the investors during the subscription period. They manage the escrow accounts, process the refunds and ensure the funds are transferred securely to the issuer. Their infrastructure supports online and offline transactions.

Depositories (NSDL and CDSL)

These are like digital lockers where you keep family jewellery – safe, secure and transferable easily. These institutions hold your investment electronically, ensuring that you don’t lose physical papers and can access your securities whenever needed. Depositories hold securities in electronic form and facilitate dematerialization.They provide safe custody and seamless transfer of ownership. For receiving securities issued in the primary market, investors are required to open a demat account with a depository participant.

Stock Exchanges

These are like the online marketplaces like Amazon or Flipkart, where you list your restaurant’s gift vouchers once they are launched. People can buy and sell them thereafter. The exchanges ensure rules are followed and buyers trust the platform.The securities are listed on exchanges such as NSE and BSE after they are issued. They scrutinize listing applications, require adherence to disclosure norms and facilitate trading in the secondary market. Their role starts from the IPO route and continues during the life of the security.

Regulatory Authorities (SEBI)

Think of the food safety inspector who visits your restaurant before the grand opening.They ensure you follow hygiene and safety norms. SEBI ensures all participants in the financial setup behave fairly and transparently. The primary market in India is regulated by SEBI which reviews offer documents, enforces disclosure standards and monitors compliance to protect interests of investors. SEBI’s role ensures that issuers and intermediaries operate within a transparent and fair framework. Investors These are the people who book tables at your new restaurant or buy your pre-order vouchers. Some are your close friends (retail investors), some are big restaurant chains scouting for opportunities (QIBs), each with their own expectation and impact on your success.They subscribe to the securities and supply the capital. They are divided by category, with each category having specific allotment quotas and bidding norms.

Credit Rating Agencies

Think of a food critic reviewing your restaurant before you open. They sample your dishes and assign ratings. Consumers use those reviews to decide if it’s worth eating there. Similarly, investors use ratings to evaluate the risk of your bonds or debentures . Credit ratings agencies evaluate the financial position of the issuer of debt instruments and assign ratings that reflect the risk. These ratings affect investor decisions and the pricing of the securities. Legal Advisors and Auditors Like your lawyer reviewing the lease and your accountant confirming the costs before opening day. They ensure everything is legitimate and your documentation isn’t hiding any unpleasant surprises.Their stamp builds trust with investors.

Legal advisors ensure that the offer meets the requirements of the law . Auditors verify the validity of financials presented . Their due diligence gives investors the confidence to trust the offer and regulators to approve it .

Nirav: I read about the issue value at which the securities are issued. How is that value determined?

Vedant: Sure. The primary market is when the companies issue securities to the investor directly to raise the capital. The value or issue price is usually determined by face value, premium or by book-building. That decision is driven by factors including the company’s valuation, demand from investors and the market’s state.

Nirav: So if a company issues shares at ₹100 and the face value is ₹10, does that mean ₹90 is premium?

Vedant: That’s right. That Rs 90 goes into the securities premium reserve on the company’s balance sheet. It indicates how investors perceive the company’s growth prospects.

Nirav: What’s this book-building method you mentioned?

Vedant: Book-building is a price discovery mechanism, which is mostly used for IPOs. The company does not fix a price, but a price band, say between ₹95 and ₹105 and investors bid within this price band. The final issue price is then decided based on highest concentration of demand.

Nirav: Interesting.

Vedant: Yes. Does SEBI have any regulation on how these prices are fixed? SEBI wants full disclosure in offer document for transparency. The methods of pricing have to be clearly laid out to protect the investors and the integrity of markets.

Nirav: Good point. So either fixed pricing or book-building, the basic idea is to match the investor interests with the company valuation.

Vedant: Exactly. For traders or analysts, it can be helpful to know these pricing strategies to identify IPO candidates or trying to figure out the market’s reaction to a new offering.

4.9 Value At Which Securities Are Issued In Primary Market

A. Types of Issue Pricing Mechanism

- Fixed Price Method (i.e. For Movie Tickets at a Theatre)

The price is fixed and disclosed before you decide to buy eg. You pay ₹250 for a ticket, whether the hall is full or almost empty. The price is fixed and disclosed before you decide to buy

- The issuer fixes a pre-determined price for the securities.

- The price will be disclosed in the offer document before the opening of the issue.

- Investors know the exact price they will pay while applying.

- Common in smaller or less complex offerings.

2. Book Building Method

For example A flight from Mumbai to Delhi may have a price band of ₹3,000–₹6,000. Early buyers or buyers at off-peak times get lower prices, while peak time buyers pay higher. Set by investor bids and demand.

Price band – Investors bid the amount they want to buy and the price they are willing to pay within this band. Commonly used while pricing IPOs

B. Factors affecting issue price

Think of it as the sale of home-made Diwali sweets in your locality. If your sweets are always tasty and well received, it indicates you have good fundamentals – confidence in your quality, and a good track record of results. Your neighbours compare your prices with other sellers of similar items to help set your price, similar to valuation methods such as P/E or P/B ratios in finance. Now if it is festival time and all want to buy, the mood is good and demand increases. This is like a bullish market trend where premium pricing is possible.

On the other hand, if it is an off-season or there is sudden inflation in ingredient costs, the demand may fall or your costs may increase – like bearish conditions in the stock market. In such situations you may have to reduce your price or even postpone selling. Finally, if your housing society has such rules that pricing and ingredient have to be displayed clearly, that is like SEBI’s regulatory oversight, which ensures transparency and protects the interests of buyers.

Company Fundamentals

- Financial performance, growth prospects, asset base and profitability.

- Strong fundamentals often warrant a higher issue price.

Valuation Methods

- Price-to-Earnings Ratio (P/E Ratio)

- Price-to-Book Value Ratio (P/B Ratio)

- Discounted Cash Flows Method

- Valuation tool for peer group and industry comparisons

Market Conditions

- Current mood of investors

- Interest rates

- Economic indicators

- Bull market condition, warrants should be priced higher

- Bear market conditions, warrants should be priced lower

Demand-Supply Factors

- While valuing using the book building method, the demand-supply factor could make the price fall near the upper limit.

- Demand is low, and therefore the product may have been priced at the lower limit.

Regulatory Oversight

- Full disclosure of pricing rationale in the offer document is mandated by SEBI.

- is transparent and protects the interests of investors.

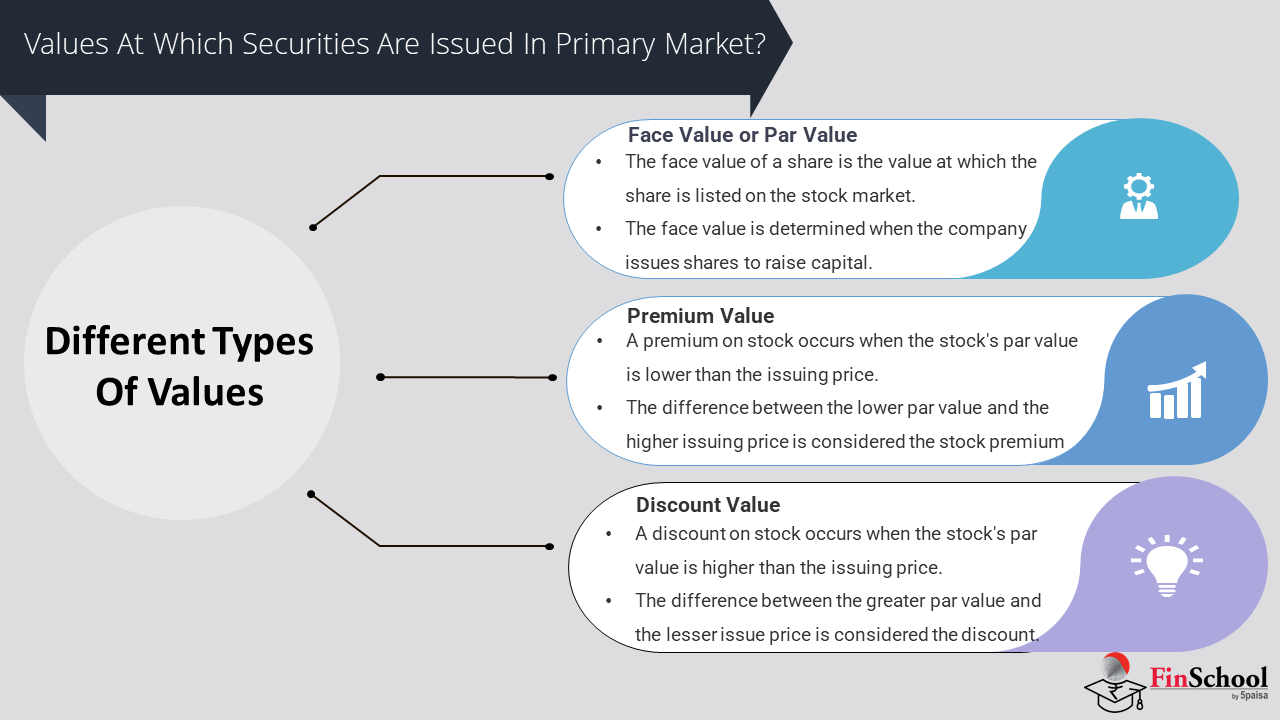

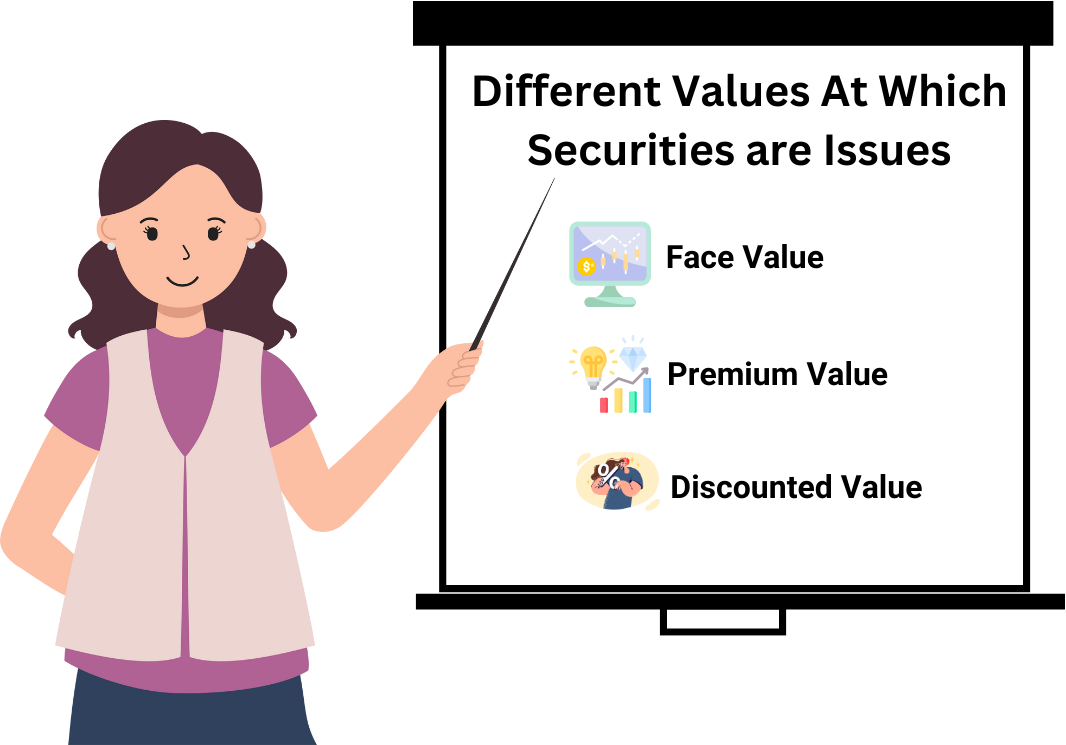

Premium, Discount and Face Value

Imagine that you are selling notebooks made by you in a local fair. You think that the basic price of a notebook will be ₹100, which is its face value. Now, lIf your notebooks are beautifully made and are in high demand, you can sell them for ₹150. That excess ₹50 is a premium, for how much people value your product. lIf you’re trying to clear stock or get early buyers, you can sell them for ₹80. That’s a discount, used strategically to increase interest.

And if you sell them exactly at ₹100, that’s at par no premium or discount, just the nominal value.

So,

Face Value: Nominal value of the security (e.g., ₹10 per share).

Issue Price: Can be at par (equal to face value), at a premium (above face value), or at a discount (below face value, though rare and regulated).

- The premium is a measure of investor confidence and a measure of the valuation of the company

- A discount may be available in rights issues or to strategic investors under certain conditions

- Role of Intermediaries

Imagine that you are organizing a big wedding and you are the host but you need someone to help you sort out the details: The wedding planner is the merchant banker. He advises you on budget, choice of venue and how to allocate resources, just like merchant bankers advise companies on pricing and valuation. An underwriter is like a caterer who promises to feed 500 guests even if only 300 actually turn up. They take the risk and promise the service will be rendered irrespective of the number of people who turn up. A food critic who looks at the past performances of the caterer and gives a rating is like a credit rating agency. Their evaluation decides whether the guests will feel that the food will be good or not, just as the ratings affect the confidence of the investors in the debt instruments.

So,

- Merchant Bankers: Advise on pricing strategy and do the valuation.

- Underwriters: Can affect pricing based on their risk appetite and ability to reach the market.

- Credit Rating Agencies : Ratings affect coupon rates and investor perception of the debt instrument

Nirav : Vedant , Now I Just need to Understand what are Risks and Challenges involved in Primary Market?

Vedant : Sure! You definitely need to know What are the Risks involved in Primary Market

4.10 Risks and Challenges in Primary Market

Imagine a business owner who wants to start a new food delivery app in your city. She thinks her app is worth a lot of money so she charges a high subscription fee.. When people start using the app they find out it does not work very well and they uninstall it. This is like when a new company goes public and its stock price goes down because it is not as good as people thought. The business owner is new so people do not know if she is trustworthy and her advertising does not give all the details, like which areas she delivers to and how to get a refund.

Some people sign up for the app because they hear it is good. Then they feel cheated when they find out it is not. Others do not want to sign up because they do not have information.. People who are good with technology and do their research know more about the app and can make a better decision. If the business owner starts her app during the monsoon season when people do not want to order food that is a time to start.. If her app crashes when a lot of people are trying to use it that is a problem with how it is run.

Like when a company goes public the success of the app depends on many things like when it starts, how honest the business owner is and if people trust her.

- Problems with the company

- The company might be worth less than people think or the price might be too high which can make investors lose confidence.

- The company might not have a history. It is hard to know if it is a good investment.

- The company might not give all the information, which can mislead investors and get the company in trouble.

- Problems with investors

- Some investors might not have all the information they need to make a decision.

- Some investors might make decisions based on what others are doing rather than thinking for themselves which can make the price of the stock go up and down.

- Some investors might not get to buy much stock as they want which can make them not want to invest.

- Problems with the market

- The market might be unpredictable which can affect how investors feel about the company.

- The market might not be interested in the stock, which can make it hard to sell.

- The timing of when the company goes public might be bad which can make it hard to sell the stock.

- Problems with rules and regulations

- The process of going public can be complicated and expensive.

- The company might get in trouble if it does not tell the truth or leaves out information.

- The rules and regulations are always changing, which can make it hard for the company to keep up.

- Problems with operations and costs

- Going public can be expensive which can be a problem for companies.

- The people who help the company go public might not be able to sell all the stock, which can be a problem for them.

- The companys technology and infrastructure might not be good enough which can make it hard for investors to buy the stock.

Nirav: That was a lot to learn about the market like how prices are set and the risks involved.

Vedant: Yes it is a lot to take in.. It is all important when a company wants to raise money from the public.

Nirav: So just to summarize the primary market is where companies first sell their stock and the price is determined by how much people want to buy it and how much the company wants to sell it.

Vedant: That is right.. All this leads us to the next topic, which is IPOs.

Nirav: IPOs are when companies go public right?. Why do they do that?

Vedant: Companies go public to get a lot of money which they can use to grow their business pay off debt or innovate. It also helps build trust and gives the people who started the company a chance to make some money.

Nirav: So an IPO is like a bridge from being a company, to being a public company.

Vedant: That is a way to put it. Time we can talk more about what an IPO is and how it works.