1.1 What Is Investing & Why to Invest?

“ Investing puts money to work. The only reason to save money is to invest it.”-Grant Cardone.

Grant Cardone a well-known entrepreneur, real estate investor, motivational speaker, and author wrote this quote which explains us how important investing is. Investing puts money to work. Absolutely True. Because in this era of rapid economic shifts , inflationary pressures, and evolving financial landscape investing is no longer optional. It has definitively become a necessity. Today Global economy demands a protective approach to wealth building and investing wisely is the only solution for long term success.

What is Investing & Why Should you Invest?

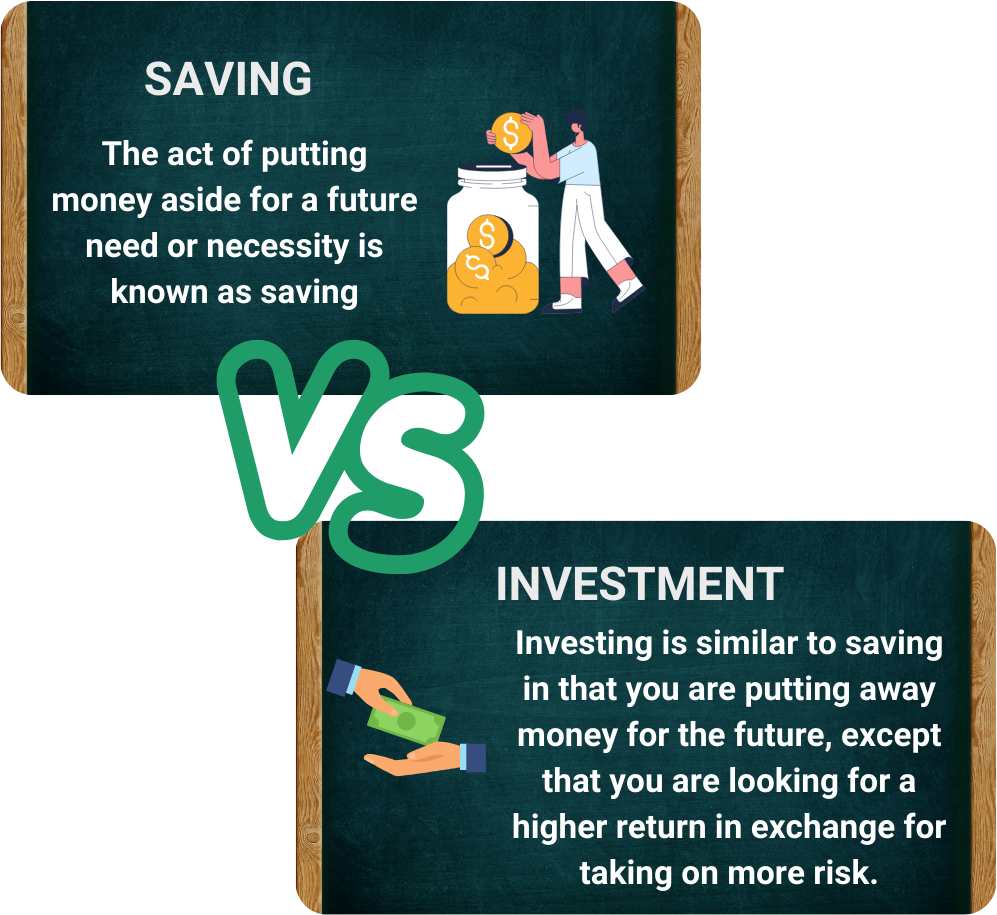

Investing is a process where money or resources are allocated to assets with the expectation of generating returns over time. Now What are these Assets? It includes stocks, bonds, real estate, mutual funds, commodities or even businesses. Savings involves keeping money in a safe place like a bank account but investing involves putting money to work that have the potential to grow in value.

Let us understand through a example. Nirav and Vedant are companions. Both are young and they worked hard, earned a decent income, but they had different approaches and mindset to managing their money.

Nirav – The Saver

Nirav was very cautious. Every month he used to carefully set aside a portion of his salary in his savings account. He felt secured as he knew he had money for emergencies. His account grew slowly, and he was happy with this fact.

Vedant – The Investor

Vedant, on the other hand, believed that money should grow. Although he had the habit of keeping some money in savings for emergencies, he ensured that he invested a portion of his money in stocks, mutual funds, and real estate.Vedant knew very well that investing came with risks, but he believed in the power of compounding and market growth.

Now Imagine the situation after 10 years

Nirav had built up a reasonable savings amount, but inflation had slowly eaten up his savings. The rising cost of living meant his money was not worth as much as it should be.

So What did you learn from this?

- Savings provide liquidity but that is not enough as it grows slowly

- Investments have risks but have the potential for higher returns and wealth

Then Why Should You Invest? Here are some points listed which could help you

- To Beat Inflation & Preserve your Wealth

- Take Advantage of Compounding

- Risk Management for Better Returns

Now that you have understood the concept investing and why it is so much important to invest in today’s world , our next step is to explore the risks that come along with it. Investing opens doors to long-term wealth creation and financial freedom but you should also understand it comes along with lot of challenges. Now let us understand the various risks investors face and how informed decisions can transform risk into opportunity.

1.2 Risks Associated With Investing

“ Risk comes from not knowing what you are doing.” – Warren Buffett

Warren Buffett stresses that the investing risk comes from lack of expertise, not knowing about market place volatility. Investors who act on emotion or follow traits with out understanding what they are investing in are basically not trading. Knowledgeable investors are those who studies employer fundamentals, grasp market cycles, and diversify wisely and they are ones who can better manage uncertainty and reduce losses. While making an investment offers strong ability for economic increase, it additionally contains inherent dangers and understanding those risks is fundamental to building clever techniques that protect our capital and increase our returns.

-

Market Risk

Market risk is the loss generated due to broad marketplace fluctuations because of factors like financial downturns, political instability, pandemics, or economic crises. A top instance is the 2008 Global Financial Crisis, while inventory markets worldwide plunged as predominant financial institutions collapsed and the housing bubble burst, impacting investments throughout stocks, bonds, and commodities, regardless of individual organization electricity. While marketplace danger affects the whole monetary system and can not be avoided completely it can be controlled through diversification.

-

Inflation Risk

Inflation Risk takes place when the value of money erodes over time, lowering the real returns on investments that don’t keep pace with growing expenses. For examples Income of 5% yearly on fixed deposits at the time when the inflation is running at 6%. An example from the history is the oil disaster, where hovering oil charges induced global inflation, diminishing the cost of fixed-income assets like bonds and savings. Investing in assets that often outpace inflation, such as stocks, real estate, or inflation-indexed bonds is considered essential for investors to preserve their wealth.

-

Liquidity Risk

Liquidity Risk Investors face liquidity risk when an asset cannot be sold without impacting its value. Stocks and mutual funds are simple to trade, however, assets like real estate, fine art, and private equities, are more difficult to convert in a timely manner. Yes Bank 2020 disaster is a good example. Financial instability made Yes Bank depositors panic and they could not retrieve their own deposits. Yes Bank exemplified the importance of Corporate Financial Analyis and having an optimal strategy of short and long term investments.

-

Interest Rate Risk

Interest rate risk applies to bonds and other fixed income securities. It is a concerning thought to watch one’s investment losing value. Because of a normal inverse relationship between interest rates and market value of bonds, the investments are losing value when interest rates are rising. Investors with fixed income securities watch the actions of the country’s central bank in this case the RBI, in order to predict interest rate changes. For example, the RBI hiked the rates in 2022 and the bonds prices plummeted. This is unfavorable for people with the bonds because the bonds are supposed to be a long term investment. Additionally, people with floating rate mortgages are exposed to this risk. When market interest rates rise, their interest payments increase, thus, they experience more financial stress.

-

Credit Risk

Credit risk is a type of risk where the borrower whether an organization or government, does not fulfill its financial commitments creating a risk for investors in bonds, loans, or other debt instruments. This can be avoided by selecting high-credit-rating securities and performing comprehensive financial analysis. Remember Kingfisher Airlines? The owner Vijay Mallya borrowed significantly however didn’t generate income, leading to loan defaults and ultimately the airline’s crumbled. Indian banks confronted important losses, highlighting the dangers of lending to companies with poor monetary basics.

-

Business & Industry Risk

Business threat refers to the challenges which occur due to business or industry poor management regulatory shifts, competition or technological disruption. A classic example here would be of Kodak . Our childhood photography giant Kodak’s decline was in 2000’s and as soon as the images massive failed to adapt digital revolution at the same time rivalry like Sony and Canon embraced innovation, leading to Kodak’s financial ruin in 2012. Similarly Jet Airways downfall in 2019 because of mismanagement and rising gas costs and fierce opposition from IndiGo brought about suspension in their operations and accordingly led to insolvency.These cases illustrate how even big corporations can falter if they don’t reply correctly to evolving marketplace dynamics. Diversifying facilitates mitigate such risks.

-

Exchange Rate Risk

Exchange rate risk impacts traders keeping overseas property, as currency fluctuations can have an impact on returns. When Rupee depreciates against US Dollars it actually hurts Indian investors holding US assets even more . During the COVID-19 pandemic, global uncertainty drove high currency volatility also importers were burdened due to currency fluctuations and Exporters got the benefit of INR depreciation. Thus understanding exchange rate risk is very important to manage volatility and protect our returns.

-

Emotional & Behavioral Risk

Investing isn’t just a numbers recreation, it is deeply influenced through psychology. Emotional selections pushed with the aid of fear, greed, or herd mentality frequently cause errors and panic in the course of downturns and this is just because you have not understood the basics. A good example is the cryptocurrency hype in India, where many traders sold Bitcoin at huge fees due to FOMO. While understanding risks helps keep away from pitfalls, timing is equally critical,starting early helps to gain income through compounding, and thus your cash multiplies over the years .

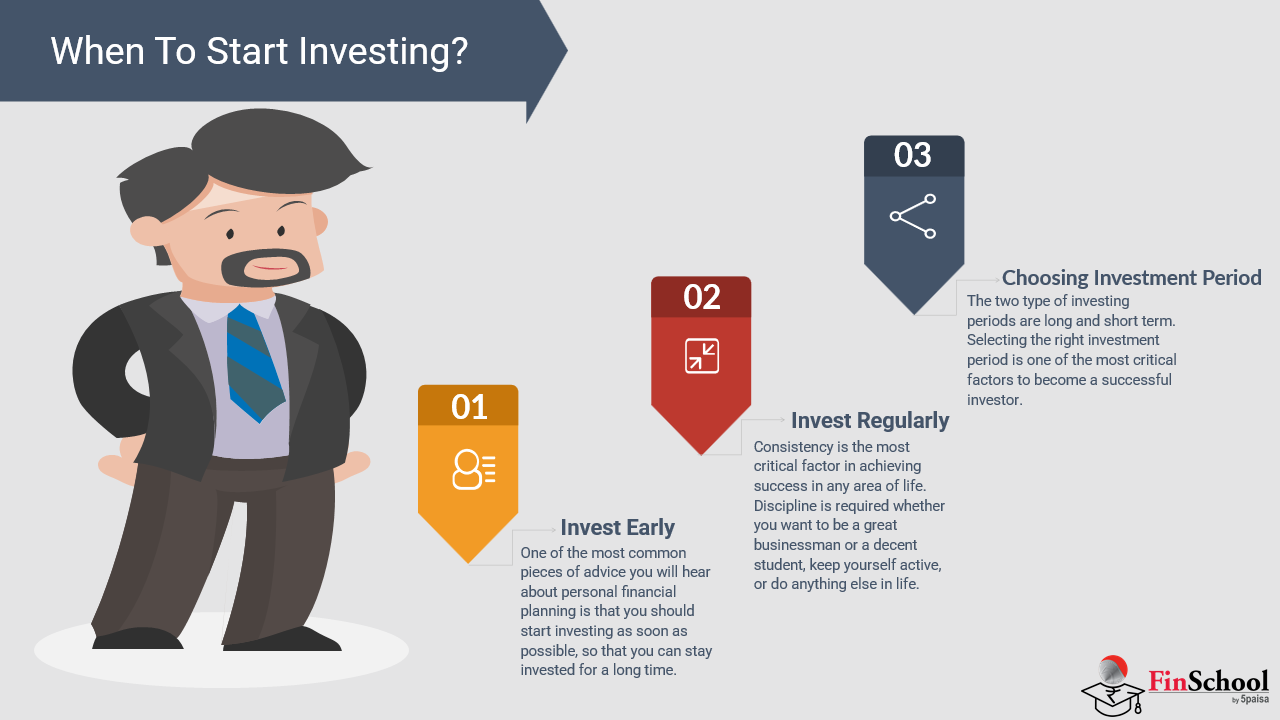

1.3 When To Start Investing?

Often even before investing the first question that comes to our mind is When to Start Investing? What is the Right time and age to start investing?

Well the answer is quite simple – As Early As Possible!

When you start investing early, you have enough time for your money to grow due to the power of compounding. This is the process where earnings generate more earnings over time. However the right time to start investing depends on factors like financial stability , your risk tolerance levels and investment goals.

Let us understand this with the help of an example

The Power of Early Investing

Now Nirav and Vedant example

Vedant suppose started to make investment of ₹4,000 per month at age 25. Nirav delayed his investing until the age of 35. Assuming a 10% annual return, below we have a table which shows how their investments grow by the age of 55:

|

Age Started |

Monthly Investment |

Total Invested |

Value at 55 (10% return) |

|

Vedant(25) |

₹4,000 |

₹14.40 lakhs |

₹91.57 |

|

Nirav (35) |

₹4,000 |

₹9.60 lakhs |

₹30.62 lakhs |

CASE 1

Compounding Calculation for Vedant

|

Sr No |

Amount |

Formula |

|

25 |

₹48,000 |

₹ 50,681.12 |

|

26 |

₹ 96,000 |

₹ 1,06,669.23 |

|

27 |

₹1,44,000 |

₹ 1,68,520.01 |

|

28 |

₹1,92,000 |

₹ 2,36,847.38 |

|

29 |

₹ 2,40,000 |

₹ 3,12,329.52 |

|

30 |

₹ 2,88,000 |

₹ 3,95,715.63 |

|

31 |

₹ 3,36,000 |

₹ 4,87,833.35 |

|

32 |

₹ 3,84,000 |

₹ 5,89,597.01 |

|

33 |

₹ 4,32,000 |

₹ 7,02,016.64 |

|

34 |

₹4,80,000 |

₹ 8,26,208.08 |

|

35 |

₹5,28,000 |

₹ 9,63,403.99 |

|

36 |

₹5,76,000 |

₹ 11,14,966.10 |

|

37 |

₹6,24,000 |

₹ 12,82,398.75 |

|

38 |

₹6,72,000 |

₹ 14,67,363.78 |

|

39 |

₹7,20,000 |

₹ 16,71,697.06 |

|

40 |

₹7,68,000 |

₹ 18,97,426.71 |

|

41 |

₹8,16,000 |

₹ 21,46,793.21 |

|

42 |

₹8,64,000 |

₹ 24,22,271.64 |

|

43 |

₹9,12,000 |

₹ 27,26,596.26 |

|

44 |

₹ 9,60,000 |

₹ 30,62,787.64 |

|

45 |

₹10,08,000 |

₹ 34,34,182.65 |

|

46 |

₹ 10,56,000 |

₹ 38,44,467.58 |

|

47 |

₹ 11,04,000 |

₹ 42,97,714.69 |

|

48 |

₹ 11,52,000 |

₹ 47,98,422.71 |

|

49 |

₹12,00,000 |

₹ 53,51,561.39 |

|

50 |

₹12,48,000 |

₹ 59,62,620.92 |

|

51 |

₹12,96,000 |

₹ 66,37,666.38 |

|

52 |

₹13,44,000 |

₹ 73,83,397.91 |

|

53 |

₹13,92,000 |

₹ 82,07,217.28 |

|

54 |

₹14,40,000 |

₹ 91,17,301.30 |

The formula for compound interest is:

A=P(1+r/n)nt

Where:

- A= Future value of investment

- P= Monthly investment amount

- r= Annual interest rate (in decimal)

- n= Compounding frequency per year

- t= Number of years

For Vedant (Investing ₹4,000/month from Age 25 to 55)

- MonthlyInvestment (P): ₹4,000

- TotalYears (t): 30

- AnnualRate (r): 10% or 10

- CompoundedMonthly (n = 12)

- Monthly Rate : 0.10/12 = 0.008333

Using the SIP formula for monthly investments:

FV=P×(1+r/n)nt−1/r/n)×(1+r/n)

Using exponential method (1+i)= 1 + 0.008333 = 1.008333

(1.008333)360 = 19.92 (approx)

So as per formula = 4000 * 19.92-1/0.008333 * 1.008333

= 4000 * 18.92/0.008333 *1.008333

= 4000 * 2270.49*1.008333

= 4000*2289.40

= 91.57 lakhs approx

Click on the excel sheet to get the calculations –Link

CASE 2- For Nirav (Investing ₹4,000/month from Age 35 to 55)

Monthly Investment (P): ₹4,000

Total Years (t): 20

Annual Rate (r): 10% or 0.10

Compounded Monthly (n = 12)

FV=4000×((1+0.10/12)12×20−1/0.10/12)×(1+0.10/12)

Solve (1 + r/n) 1+0.10/12=1.0083333

Calculate the exponent 12×20 =240months (1.0083333)240

Using exponentiation: (1.0083333)240 ≈7.328

Solve the fraction inside the brackets (7.328−1)/0.0083333

=6.328/0.0083333

=759.39

Multiply by (1 + r/n) (1+0.0083333)=1.0083333

759.39×1.0083333=765.71

Multiply by the monthly investment FV=4000×765.71

FV=₹ 30.62 lakhs (Approx)

Compounding Table Showing Nirav’s Investment Growth-AGE- 35

| 35 | ₹ 48,000 | ₹ 50,681.12 |

| 36 | ₹ 96,000 | ₹ 1,06,669.23 |

| 37 | ₹ 1,44,000 | ₹ 1,68,520.01 |

| 38 | ₹ 1,92,000 | ₹ 2,36,847.38 |

| 39 | ₹ 2,40,000 | ₹ 3,12,329.52 |

| 40 | ₹ 2,88,000 | ₹ 3,95,715.63 |

| 41 | ₹ 3,36,000 | ₹ 4,87,833.35 |

| 42 | ₹ 3,84,000 | ₹ 5,89,597.01 |

| 43 | ₹ 4,32,000 | ₹ 7,02,016.64 |

| 44 | ₹ 4,80,000 | ₹ 8,26,208.08 |

| 45 | ₹ 5,28,000 | ₹ 9,63,403.99 |

| 46 | ₹ 5,76,000 | ₹ 11,14,966.10 |

| 47 | ₹ 6,24,000 | ₹ 12,82,398.75 |

| 48 | ₹ 6,72,000 | ₹ 14,67,363.78 |

| 49 | ₹ 7,20,000 | ₹ 16,71,697.06 |

| 50 | ₹ 7,68,000 | ₹ 18,97,426.71 |

| 51 | ₹ 8,16,000 | ₹ 21,46,793.21 |

| 52 | ₹ 8,64,000 | ₹ 24,22,271.64 |

| 53 | ₹ 9,12,000 | ₹ 27,26,596.26 |

| 54 | ₹ 9,60,000 | ₹ 30,62,787.64 |

Click on the link to get Nirav’s Compounding Table Calculations

Nirav’s investment grows to ₹ 30.62 lakhs at age 55.

What did you Learn?

Now look at the numbers. Vedant began investing a decade before Nirav, and he invested only ₹ 5 lakhs more. But when you compare their final amounts, Vedant has earned more than twice as much as Nirav’s . This shows the power of starting early and letting your money grow on time. It is like a snowball effect. The earlier you start, the more time your money has to roll with interest and grow in to something big.

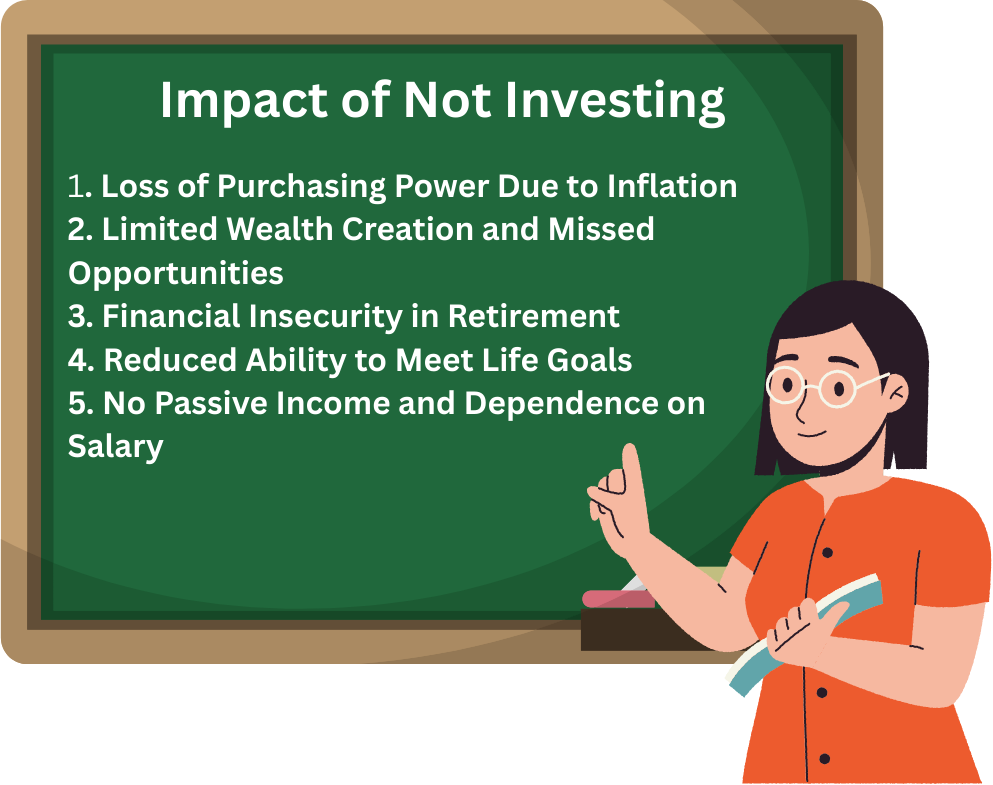

1.4 Impact of Not Investing

Not investing can impact your financial growth negatively and at the same time it can impact your future opportunities and stability as well. Many of them believe that savings is enough but inflation makes us realize that something more is needed. Below are some points which makes us understand what is impact of not investing.

- Loss of Purchasing Power Due to Inflation

As we already discussed in earlier sections, Inflation steadily erodes the purchasing power of idle cash and thus keeping Rs 100000 in a savings account earning 3% interest when the inflation is at 6% is a net loss in real value. Over a period this gap widens which reduces financial stability and future opportunities. Thus one should do active investment to grow wealth and secure a long term well being.

- Limited Wealth Creation and Missed Opportunities

It is now obvious that investing is a powerful tool for building wealth. Through compounding we can grow our passive income and also it helps in asset appreciation. Without it , financial progress remains slow and quite limited. Let us go back to Nirav and Vedant example. Both saved ₹ 4000 per month, but Vedant invests his savings when he is 25 years whereas Nirav starts to invest when he is 35 years. Both invested the amount @ 10% annual returns. After 30 years Vedant accumulated over 91 lakhs and Nirav ends up with just 30 lakhs. This difference highlights how investing helps to build wealth creation compared to savings.

- Financial Insecurity in Retirement

Depending completely on savings without investing can create serious financial challenges during retirement as non invested funds diminish gradually due to inflation. Passive income from investments like mutual funds, stocks or bonds offers long term financial stability and helps maintain purchasing power. For instance, a person who invests consistently throughout their working life can retire peacefully with a secured income stream in their hand. But the one who avoids investing may face retirement with limited financial resources and increased vulnerability.

- Reduced Ability to Meet Life Goals

Investments play a very important role in achieving life dreams such as home, education, or travel. Without investing individuals may need to rely on loans or delay their financial goals. Investing in equity funds or real estate can help a person afford a home of their dream more easily compared to someone who has not invested any amount and depended solely on savings.

- No Passive Income and Dependence on Salary

Investments in dividend stocks , rental properties or interest bearing assets creates passive income streams which reduces financial dependency. Someone who invests in dividend paying stocks builds an additional income source, while those who don’t invest must rely on their job and salary.

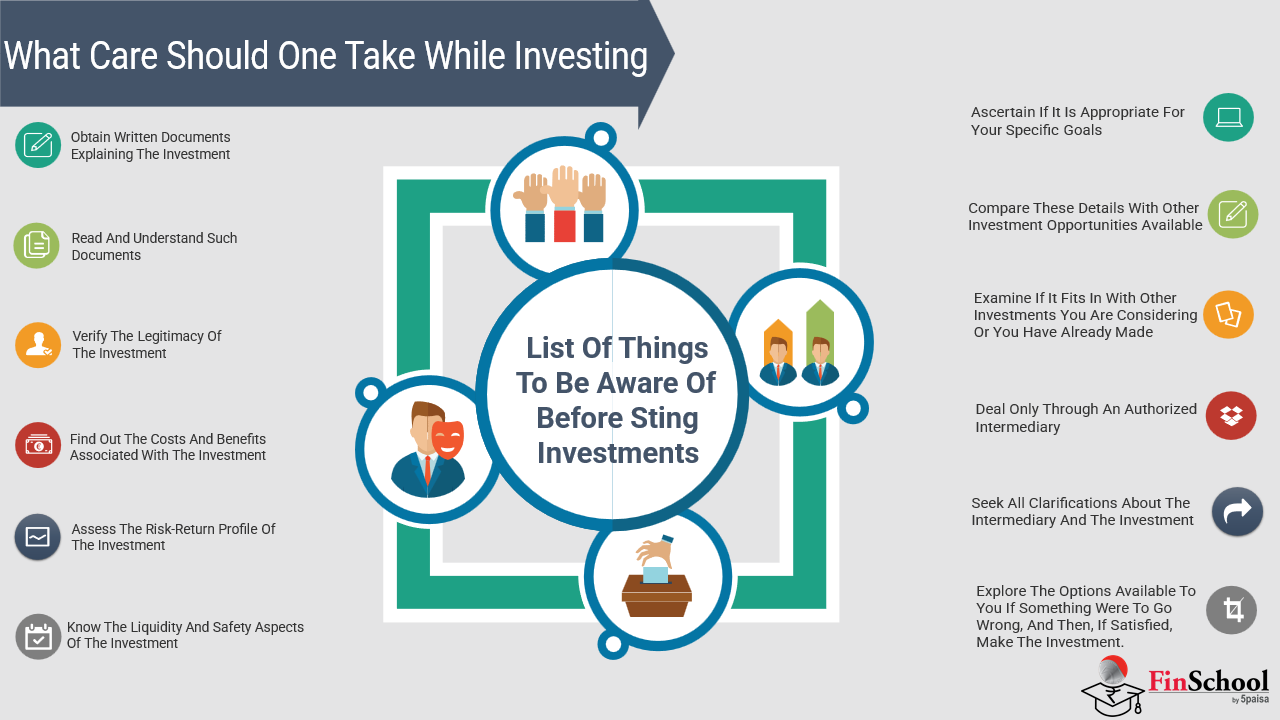

Once we realize how important is savings as well as investments, the next step is to understand the multiple sources of investing and that too with the help of strategies. Investing is all about discipline. Before you invest and put your hard earned capital it is essential that you understand few critical aspects that can shape investment outcomes.

1.5 Things to know before investing

Trading is just like a skill. You need strategy , mental sharpness and the ability to make split second decisions based on your opponents decision. Just like you play one day cricket. Similarly traders must read the market signals manage risk and adjust position quickly as prices change. In contrast long term investing resembles planting a tree; you select the right seed , nurture it and allow to foster steady growth. Trading demand constant vigilance and emotional resilience. Before entering the financial markets as a trader it is very important that you understand the market behaviour and manage risks accordingly. Be mentally prepared for emotional ups and downs. This foundation is the key to take decisions than making costly mistakes.

-

Understanding Market Structure and Asset Classes

The trading world is not just about clicking buttons, the marketplace has its own structure , own rules and whole of mix asset classes. Consider Stocks, commodities like gold and oil, currencies and more complex instruments like derivatives. Each of them carry different characteristics and risk profile. Let us understand each one of them.

Ok. So before we understand what exactly equities offer Let us first understand what are equities . Equities are stocks or shares and they represent ownership interest in any corporation where you are entitled to enjoy the future profits of the corporation. It offers opportunities for both short-term gains and long-term appreciation. In this case, you should be extremely cautious since they tend to be volatile and they depend on corporate profits, macro-economic policy and world events.

The Commodities such as Gold, Oil and Agricultural Products vary according to factors such as supply and demand, geopolitical stability, and economic cycles. Forex trading deals with currency pairs which are effected by interest rate decisions, inflation, and international trade policies.

Options and Futures allows room for leveraging and hedging opportunities which require advanced strategies to manage risks effectively.

2. Technical Fundamental Analysis

There are two ways to understand the market. One is technical analysis and the the other one is fundamental analysis. So what is technical analysis? Well Technical analysis is a form of analysis that studies the heart of stocks based on historical price movements patterns while fundamental analysis analyze the earnings, policies and economic indicators that drive prices. To put this differently technical analysis can be viewed as short term signal while fundamental analyses the earnings , policies and economic indicators that drive prices.

Technical analysis : This method of analysis basically involves study of historical price movements. It basically involves analysing historical price movements, chart patterns, and market trends. The use of technical indicators like moving average, relative strength index (RSI), and Bollinger Bands helps in identifying entries and exits.

Fundamental analysis : Fundamental analysis is based on looking at financial statements, economic data, and corporate earnings. Reports on profits, interest rates, and economic trends are key to functioning the sentiments prevailing in the market.

3. Risk Management and Capital Protection

Have you ever drove a car without seatbelt and brakes? If Yes then its too risky!

Similarly in trading it is essential to use certain tools like stop loss to avoid huge losses. Knowing when to cut losses and when to book profit and how much risk should be taken is the key to stay in market.

- Position Sizing means Limiting exposure per trade prevents overcommitment and balances portfolio risks.

- Stop Loss and Take Profit Orders means setting predefined exit points ensures traders minimize losses while securing profits.

- Risk-Reward Ratio means a well-planned trade should offer a favorable risk-to-reward ratio to justify the investment.

- Leverage Control enhances profits, excessive use can magnify losses

4. Market Psychology and Emotional Discipline

What is FOMO?

Let us understand this concept in a better way. Trading isn’t just about numbers—it is about your mindset. Fear creates panic and then you sell , greed pushes you to over trade, and FOMO gets you into bad trades. Just like a villain in a movie. You expect good but FOMO spoils it . So a clear head and a disciplined plan is a must in trading. Emotion-led trading is a shortcut to regret. So here are three factors you should be careful about.

Fear of missing out (FOMO) forces the traders to chase trends and thus increasing the risk of buying at peak prices. Overtrading happens due to over confidence, resulting in poor decision-making and unnecessary losses. Panic selling at the time of market crisis can lead traders to exit profitable positions too early.

Thus developing emotional discipline through structured strategies and rational decision-making enhances trading efficiency. You need to have well defined plan that will prevent you from taking impulsive decisions to market fluctuations.

-

Importance of Liquidity and Market Timing

Suppose You are trying to sell an expensive piece of art vs. selling a popular phone . Which one do you feel is easy ? Obviously it is way easier to find a buyer for the latter. That is liquidity. Trading in highly liquid markets like major stocks and forex makes easier entries and exits. Also, timing matters news releases and opening bells often bring price swings.That is why Liquid assets like major stocks and currency pairs, allow smooth transactions with minimal price slippage. Non liquid assets can experience extreme price fluctuations due to fewer buyers and sellers thus increasing risks. Additionally, market timing plays a very crucial role in trading profitability. Some strategies work best during market volatility, such as the opening and closing hours of stock markets.

-

Trading Strategies and Choosing the Right Approach

Different trading strategies suit personalities. Are you someone who likes action? You might like day trading. Prefer a more relaxed pace? Swing trading could be for you. Scalping is ultra-fast and intense. And if you are tech-savvy, algo trading lets you automate everything. Match your strategy to your style and risk comfort.

Day Trading: Short-term trading where positions are closed within the same day is known as Day Trading. It requires making decisions and constantly monitoring charts.

Swing Trading: Swing Trading involves holding positions for a period.Swing Trading means Holding assets for multiple days or weeks to capture short- to mid-term trends. It is suitable for traders who prefer moderate risk exposure.

Scalping: Scalping means extremely short-term trading where positions are opened and closed within minutes. It is designed for capturing small price movements with high frequency.

Algorithmic Trading: Automated trading using mathematical models and pre-defined conditions is known as algorithmic trading. It needs expertise in coding and market analysis. Choosing the strategy depends on a traders risk tolerance and time. Selecting the right strategy depends on a trader’s risk tolerance, time commitment, and expertise level.

-

Transaction Costs, Taxes, and Regulations

Every trade has hidden costs—brokerage fees, taxes, and compliance rules. If you neglect these your profits may shrink fast. Thus staying informed and organized helps you keep more of what you earn.

Brokerage Fees: Brokerage fess means frequent traders should account for commission costs, spreads, and exchange fees.

Taxes on Capital Gains: Taxes on capital gains depends on the country’s tax policies. Short- term trading profits may be subject to taxation.

Regulatory Compliance: Regulatory Compliance requires that traders are aware of the laws imposed by governing financial authorities to prevent fraud and penalties. Knowing one’s financial obligations is part of optimizing their overall profit while remaining within the regulations of the marketplace.

-

Continuous Learning and Adapting to Market Conditions

Markets change very quickly like technology. Something that works today may not work tomorrow. For example, a new phone model is released each year. Keep up-to-date by reading, trying out strategies, and learning from people around you. You will continue to be able to do so throughout your career as you develop and refine yourself as an individual.

So what should you do ?

Firstly you should read financial reports, economic forecasts, and regulatory changes as it enhances decision making. Secondly you should Back-test strategies using historical data verifies performance before implementing them in live markets. Third and most important is you should Learn from experienced traders through mentorship, courses, or trading communities that accelerates progress.

Here are some investment instruments and diverse tools available to shape your wealth- building journey.

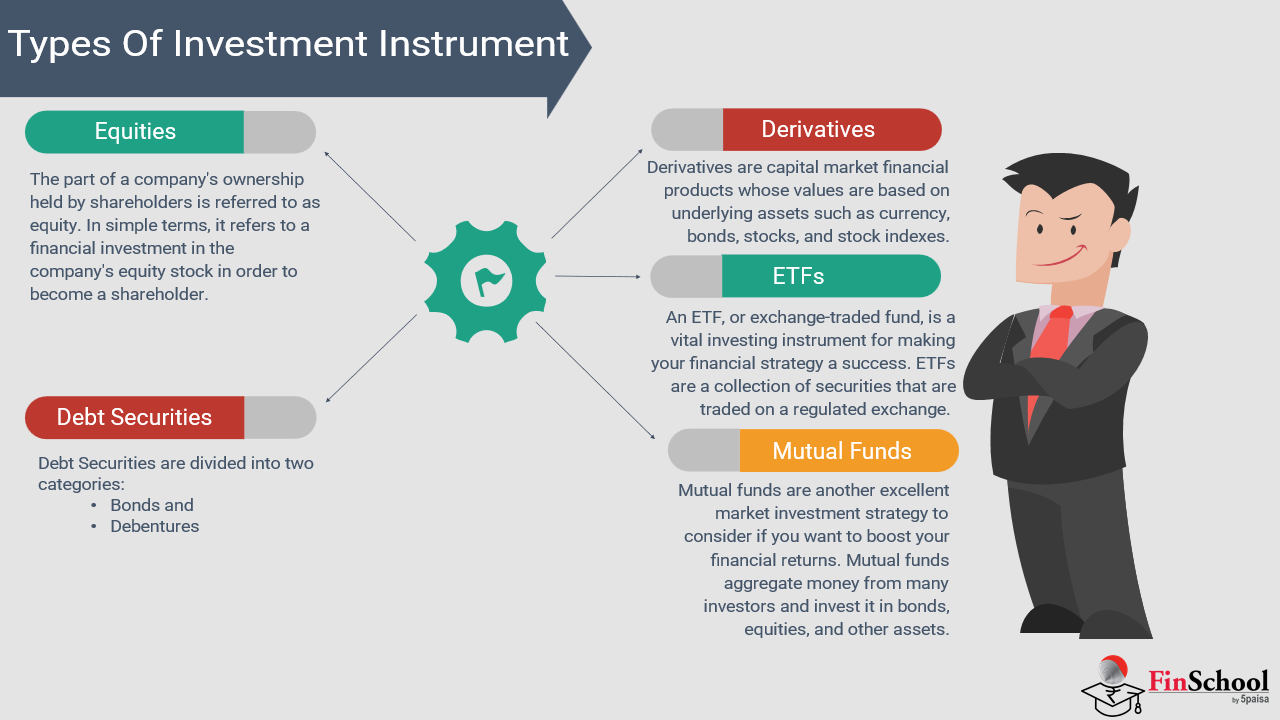

1.6 Types Of Investment Instruments

Investment Instruments

Investment instruments represent financial assets which can increase your net worth (i.e., value), provide income and help you to reduce risk. Each instrument has different purposes, and choosing the right ones depends on your risk tolerance, time horizon and knowledge of the market. By now you must be aware that investment is done in instruments apart from savings bank account. As mentioned earlier investment instruments are financial assets such as equities, fixed income securities , Mutual Funds and ETFs , Commodities and Precious Metals, Derivatives etc.

Lets understand them in detail

-

Equities

Equity investments involve buying shares of a company which makes investors partial owners as they can claim the assets and earnings. These investments offer potential returns through capital appreciation. This happens when the share prices rise and dividends are shared with the shareholders. However they do carry market risk because when the share values fluctuate based on factors like economic conditions, company performance and investor sentiments. For instance purchasing 100 shares @ Rs 100 brings the total to Rs 10000. If the price here rises to Rs 150 the share value becomes Rs 15000 I.e. a 50% gain. But if the price drops to Rs 80 the value falls to Rs 8000 and this is the risk involved.

Now let us understand the types. There are two types of equity investments

a. Common Stocks

Common stocks are the most common type of equity investment. They give investors voting rights on company matters, including selecting members of the board of directors. Investors earn their returns on common stock mostly by:

- Capital appreciation: When companies perform well, their stock prices will appreciate in value and consequently investors will be able to sell their shares at a profit.

- Income : For some companies, profits will be shared with shareholders in the form of dividends. An example of such is Infosys, as they have a history of paying dividends and producing substantial amounts of appreciation in stock value, making them appealing for both growth and dividend-focused investors.

For Example: Infosys pays dividends to shareholders, alongside long-term stock price appreciation, making it attractive to both growth and income investors.

b. Preferred Stocks

Preferred stocks differ from common stocks because they provide fixed dividends, meaning investors receive guaranteed periodic payouts regardless of company profits.

What does Preferred Stocks provide?

- Stable Income: Preferred stockholders receive dividends before common

- Limited Voting Rights: Unlike common stock, most preferred shares do not provide shareholders with voting rights on company matters

- Priority in Bankruptcy: Preferred Stockholders Have Priority Over Common Stockholders in Bankruptcy. Preferred Stockholders Will Be Paid Ahead Of Common Stockholders If A Company Quits Paying Their Debts

For Example: Many financial institutions (primarily banks) issue what are referred to as “Preferred Stock Series A” containing a specified interest payment under terms that have no impact on common stock providing a fixed dividend payment. This makes preferred stock an excellent investment option for conservative investors desiring fixed income without risking potential high growth.

2. Fixed Income Securities

Fixed income securities are investments that offer regular interest payments and return the principal at maturity. This provides stability and predictability. It is much like Nirav lending money to his cousin and receiving Rs 500 until the full amount is repaid. Now think Instead of lending to individuals , investors lend to governments, corporations or municipalities. This will earn consistent interest with volatility which are lower than equities. Government affiliated bonds such as Treasury Bills, RBI Bonds are low-risk due to sovereign backing in comparison with corporate bonds which offer higher returns but that comes with credit risk. Other option is Municipal Bonds which fund public infrastructure, zero-coupon bonds which are sold at discount plus there are no periodic Interest but these can be redeemed at full value. Such Investment options are recommended for investors with conservative mindset, Retirees or investors who want reliable income related investments with portfolio diversification options.

3. Mutual Funds and ETFs

The best example to explain Mutual fund is Nirav and Vedant. Suppose Nirav and his neighbour plan a festive meal. Everyone contributes money. Vedant here becomes fund manager, selects the best ingredients for a balanced feast of stocks, bonds and commodities. ETFs are like Nirav’s cousin Arjun who picks ready made combo meal anytime. It offers similar diversification but more flexibility. Mutual funds offer equity for growth, debt for stability and hybrid for balance while index funds track benchmarks like Nifty 50. ETFs trade on stock exchanges. It provides liquidity , transperancy and lower costs. Both helps to simplify investing through professional management. It is ideal for beginners and seasoned investors alike.

4. Commodities and Precious Metals

Commodity investing is like splitting costs among friends for a weekend trip. Each person covers a different expense to make the whole plan work. Now compare this with investment. Each investors allocate money across essentials like oil, wheat and gold to balance risk and protect against inflation and market volatility. Commodities include physical assets such as metals, energy products and agricultural goods.

These all items are vital to global trade. Precious metals like gold and silver act as safe havens during economic uncertainty, while energy commodity such as crude oil and natural gas respond to geopolitical and supply demand shifts. Agricultural commodities are effected by climate and consumption trends. Though commodity trading require expertise to manage price volatility , it offers valuable diversification and inflation protection. It is a strategic choice for institutional and seasoned investors.

5. Derivatives (Futures and Options)

Financial instruments that derive value from assets underlying such as stocks, commodities, currencies are called Derivatives. They also help manage market uncertainty like everyday agreements. Example – Locking price of mango for next month which is like a future contract. Paying a small amount for option to buy a concert ticket like an option contract. It offers flexibility without any obligation.

Swaps include exchanging financial terms. Example – Swapping loan type between two friends to manage risk. Another example is a cafe owner fixing cocoa price in advance to avoid future sot spikes that can happen. These tools – futures, options, swaps and forwards are often used for hedging/speculation. They are often used by experienced traders due to complexity and leverage in the trade they deal with daily.

Broader investment tool-kits include equities, bonds, ,mutual funds, commodities and derivatives. They allow investors to tailor portfolios to achieve heir desired goals, risk appetite and time horizon.

But there still remains a deeper financial question – savings or investment? Understanding both approaches is the key to secure one’s financial future.

1.7 Saving Or Investment – The Better Option

Now that we know that investing is always a better option rather than just saving. Both carry unique benefits , their impact on wealth creation differs significantly.

Traders and investors recognize that simply saving money may not be enough to build financial security. Investment is necessary for long term wealth creation.

Liquidity: Here Liquidity is readily available. Here Liquidity is variable—some investments have lock-in periods

Time Horizon: It is generally for Short-term focus It is Long-term wealth-building strategy

The Impact of Inflation on Savings vs. Investments

One of the biggest risks with relying solely on savings is inflation. If inflation averages 6% per year, a savings account earning 3% interest is losing purchasing power annually. Investing combats inflation by offering higher returns over time.

|

Year |

₹1 Lakh in Savings (3% Annual Interest) |

₹1 Lakh in Investments (10% Annual Return) |

|

1 |

₹ 1,03,000.00 |

₹ 1,10,000.00 |

|

2 |

₹ 1,06,090.00 |

₹ 1,21,000.00 |

|

3 |

₹ 1,09,272.70 |

₹ 1,33,100.00 |

|

4 |

₹ 1,12,550.88 |

₹ 1,46,410.00 |

|

5 |

₹ 1,15,927.41 |

₹ 1,61,051.00 |

|

6 |

₹ 1,19,405.23 |

₹ 1,77,156.10 |

|

7 |

₹ 1,22,987.39 |

₹ 1,94,871.71 |

|

8 |

₹ 1,26,677.01 |

₹ 2,14,358.88 |

|

9 |

₹ 1,30,477.32 |

₹ 2,35,794.77 |

|

10 |

₹ 1,34,391.64 |

₹ 2,59,374.25 |

|

11 |

₹ 1,38,423.39 |

₹ 2,85,311.67 |

|

12 |

₹ 1,42,576.09 |

₹ 3,13,842.84 |

|

13 |

₹ 1,46,853.37 |

₹ 3,45,227.12 |

|

14 |

₹ 1,51,258.97 |

₹ 3,79,749.83 |

|

15 |

₹ 1,55,796.74 |

₹ 4,17,724.82 |

|

16 |

₹ 1,60,470.64 |

₹ 4,59,497.30 |

|

17 |

₹ 1,65,284.76 |

₹ 5,05,447.03 |

|

18 |

₹ 1,70,243.31 |

₹ 5,55,991.73 |

|

19 |

₹ 1,75,350.61 |

₹ 6,11,590.90 |

|

20 |

₹ 1,80,611.12 |

₹ 6,72,749.99 |

To view the link for calculating the Risk vs. Reward:

Risk vs. Reward Analysis Traders and investors must assess the amount of risk they are willing to take on, in terms of the potential return as compared to the alternative. Savings accounts provide immediate access to cash, however, investing in stocks, bonds, mutual funds, commodities, and real estate can provide long-term growth.

Hierarchical View of Investment Instrument Risks:

Low Risk: Fixed Deposits, Government Bonds, PPF are generally Considered low risk

Moderate Risk: Mutual Funds, REITs, Corporate Bonds are considered moderate risk category

High Risk: Equities, Derivatives, Cryptocurrencies are high risk investment instruments.

The Power of Compounding in Investment

We have already discussed this example but let us discuss again here

Example: ₹ 4,000 Monthly Investment vs. ₹4,000 Monthly Savings

Over 30 Years Investment Growth

(Assuming 10% Annual Return): FV=P×((1+r/n)nt−1)/r/n)×(1+r/n)

Where:

- P= ₹4,000

- r= 10%

- n= 12 (compounded monthly)

- t= 30 years

Using the formula, investing ₹4,000 per month would grow to ₹ 91 lakhs approx, while simple savings at 3% interest would total only ₹28 lakhs—a difference of ₹85 lakhs over 30 years.

1.8 How Investing Helps for Retirement Planning?

Retirement planning is not just about saving . It is about investing smartly . It is to ensure financial stability and comfortable post work life. Many individuals rely on saving account but inflation, medical expenses and a longer lifespan make investments today a necessity.

Let us take an example for understanding the concept of Retirement Planning

Nirav is 30 years old and he is earning Rs 75000 per month. He dreams of retiring at 60 years of age All together he has monthly passive income of Rs 1 lakh to sustain his lifestyle. Now if here relies solely on his savings, he has a risk of inflation plus the risk of healthcare costs. In order to have an enjoyable retirement,

Nirav needs to plan his investments. The first thing he has to do is figure out what he wants for his retirement and when he wants it to happen.

He has to think about

- How old he wants to be when he stops working

- How money he will need every month after that.

Some questions to consider:

- When does Nirav want to stop working for example when he is 60 years old?

- What kind of life does Nirav want to have. The basics or a nice life?

- Does Nirav want to travel or start new things after he stops working?

Now Nirav has to estimate how money he will need to retire comfortably. Let’s say Nirav wants one lakh rupees per month which’s twelve lakh rupees per year when he is not working.

He can use a rule to calculate how much he needs to save:

Corpus = how much Nirav spends in a year divided by 4%

Corpus = 12lakhs/0.04 = 3 crores.

So Nirav has to build a portfolio of three crores by the time he retires.

That way Nirav will have money. Nirav wants to live comfortably after he retires. There are investment options to help him plan his retirement. Nirav can use these options to make a plan. Nirav’s goal is to have a retirement with Nirav’s investments. Nirav needs to make investment decisions for his future. He builds a portfolio to balance growth and stability

Equity Mutual Funds & Stocks: 50% allocation in equity mutual funds and stocks is essential for long-term appreciation.

- Fixed Income (Bonds, FDs): 20% for capital You should invest in Fixed Income Bonds and FD’s .

- Pension Plans (NPS, EPF): 20% for structured retirement savings. Invest in Pension Plans like NPS and EPFs.

- Real Estate: 10% rental properties to generate passive Rental income every month of 10% will act as a cushion during emergencies.

- Diversification ensures returns while reducing risk securing Nirav’s financial stability post-retirement.

How Compounding Strengthens Retirement Investments

Nirav starts investing ₹10,000 per month in an equity mutual fund at 12% return.

Withdrawal Strategy for Nirav’s Retirement Nirav plans his retirement withdrawals wisely:

- The 4% Rule: Withdraw ₹1.4 lakh per month from his ₹3.5 crore corpus to sustain

- Dividend Stocks & Rental Income: Passive earnings like giving flat for rent ensures financial security.

Medical Expense & Medical Emergency Planning

Nirav invests in health insurance, life insurance and emergency funds as a way to protect against incurring medical costs without depleting his retirement account. In addition, his disciplined approach provides him with financial freedom, as he has a consistent source of passive income that allows him to retire without relying on either savings or his current job.

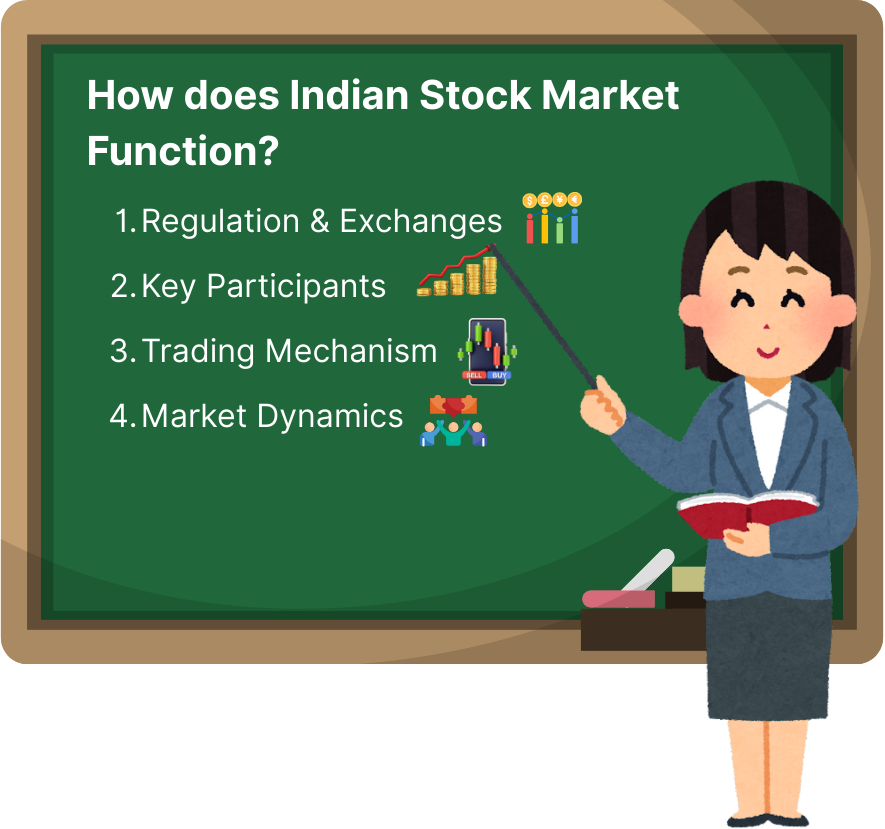

1.9 How does Indian Stock Market Function?

The Indian Stock Market is a place where people can invest their money by buying and selling types of financial products. These products include Stocks, Bonds, futures, options, Derivatives and Mutual Funds. The market is controlled by the Securities Exchange Board of India or SEBI for short. SEBI makes sure that people who buy and sell stocks do it in a way. This helps protect people who invest in the Indian Stock Market.

In India there are two places where people buy and sell stocks.

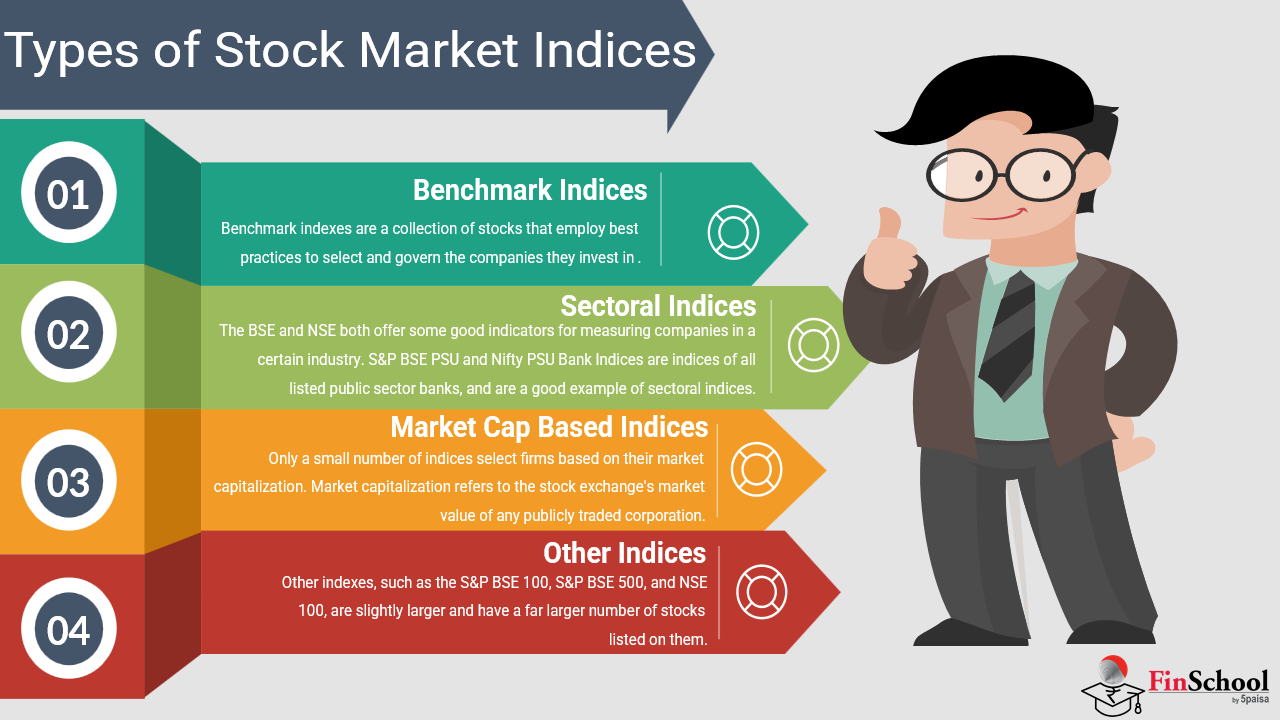

The Indian Stock Market has two exchanges:

- The Bombay Stock Exchange, also called BSE

- The National Stock Exchange, also called NSE

The Indian Stock Market is very important for people who want to invest in Stocks, Bonds and other financial products. It is the placew where people can buy and sell these products. SEBI regulates it to ensure everything is fair and transparent. It helps people invest their money.

The BSE and NSE are the two places, for buying and selling.

Key Entities Involved in Managing the Stock Market are Several participants facilitate stock market operations:

- Stock Exchanges: NSE and BSE . They provide the infrastructure for

- SEBI: SEBI Ensures fair practices and prevents

- Companies: Companies list their shares for public trading via

- Brokers & Traders: Intermediaries executing trades on behalf of

- Retail & Institutional Investors: Individuals and large institutions participating in stock transactions.

Stock Trading Mechanism

The trading process in the Indian stock market follows a structured approach:

Pre-Open Session (9:00 – 9:15 AM): This time allows price discovery before market opening.

Regular Trading Session (9:15 AM – 3:30 PM): During this there is Continuous electronic trading of stocks.

Post-Closing Session (3:40 – 4:00 PM): This time determines the closing price for stocks.

Shares are bought and sold through the order-matching system, ensuring liquidity and efficient transactions.

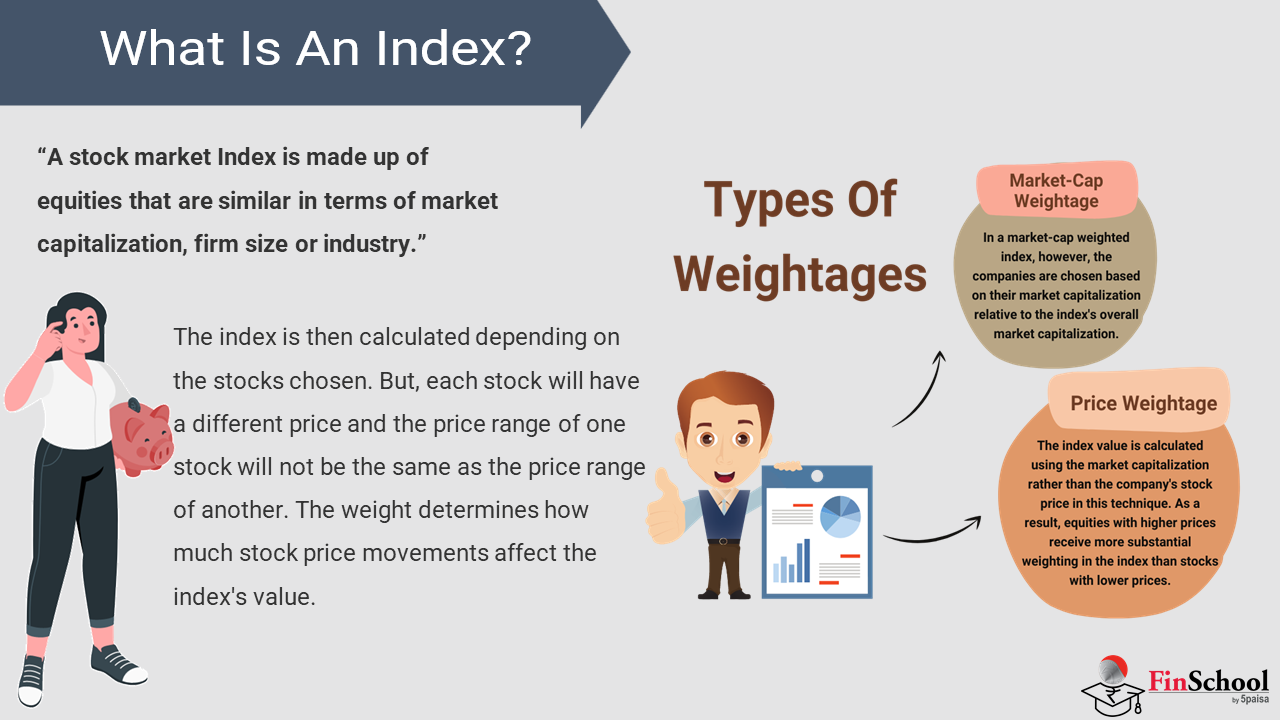

Market Index & Price Movement

Stock Market indices such as NSE and BSE serve as key benchmarks for the Indian financial system by tracking the performance of their top tier companies. This reflects the overall market trends. These index are not static , rather their prices fluctuate based on the complex interplay of factors, including company specific performance regarding earnings, revenue and management decisions. Additionally index are influenced by domestic economic policies such as RBI interest rate, inflation data and GDP growth metrics. Occasionally, global events such as international market trends, geopolitical developments and crude oil prices becomes major reason for volatility along with the changing investor sentiment and demand supply dynamics.

Regulatory & Risk Management

Corporate governance and accountancy are regulated at a high level through SEBI in order to safeguard the rights and interests of investors; they are also regulated through other means as well, including risk management tools like circuit breakers, margin requirements and stop-loss orders to limit overall volatility in the market place.

1.10 Key Takeaways

- Investingis an Important aspect of financial security, particularly in a rising cost

- Savingsprovide safety while investments yield superior gains due to compounding interest and market appreciation.

- Startingearly results in substantial growth of wealth, evident from Nirav and Vedant example.

- Wise investments create diversified incomes and financial Market inflation and liquidity risks can be overcome using diversification and education.

- Failureto invest implies reduced savings, lost chances and inadequate retirement Traders should learn different asset classes , technical and fundamental analysis and emotional intelligence.

- Investmentinstruments include stocks, mutual funds, bonds and other Indian Equity market functions under SEBI Regulations through NSE and BSE Exchanges