Long Put Condor Option Strategy

The neutral- long put condor strategy gives investors profits when the underlying stock remains between two short-put strikes at expiry. A trader gets into this strategy by buying one lower strike put, selling one lower-middle strike put, selling 1higher middle strike put and then purchasing one higher strike put. However, all these trading options should be within the same underlying instrument.

In addition, the options must bear the same date of expiry. The lower-strike and the lower-middle strike put in the long-put condor strategy are in-the-money puts. On the other hand, the higher middle and high strike puts are out-of-the-money puts. At the start of the long-put condor strategy, the underlying stock price is somewhere between two middle strikes.

Then, the four trading legs of the long-put condor are equidistant from each other. But that's not a hard nor fast rule. Other times, a trader may prefer to maintain a wide distance between two middle strikes than a distance between the outer strike and the equivalent middle strike to enjoy an extensive maximum profit zone.

The Time When Long-put Condor Strategy Works Best

A neutral long-put condor has no directional bias, and it is a range-bound trading strategy. Mainly, the strategy produces the best results if the underlying stock price remains limited between two middle strike prices. Sometimes, the neutral- long put condor strategy may have a slightly bullish or even bearish position. For example, if a trader picks two middle puts at the start of strategy execution, and the underlying price is lower than the two middle strikes, the long put condor strategy becomes bullish. Therefore, the trader may prefer the underlying price to increase and get into the zone of the two middle strikes.

Furthermore, the long-put strategy takes a slight bearing position when the trader picks middle puts, and the underlying price is higher than the two middle strikes. As a result, the trader would wish the underlying price to drop and get into the zone of two central strikes. That happens since investors get maximum benefits if the underlying price falls within two middle strikes at the expiry period.

Why Long-put Condor Works

The neural long-put condor spread is a four-legged trading option. That means it’s a blend of four different trades, including the purchase and sale of one call option, one put option at a specific strike price, and two other options at a different price strike. Long-put condor offer trader limited risk with limited possibility for profit.

When a long-put condor takes a bearish position, traders can sell one put option at a specific strike price and purchase another put option bearing a lower strike price near expiry. An investor can also buy one call option at a specified price. But the price should be above the earlier sold put option.

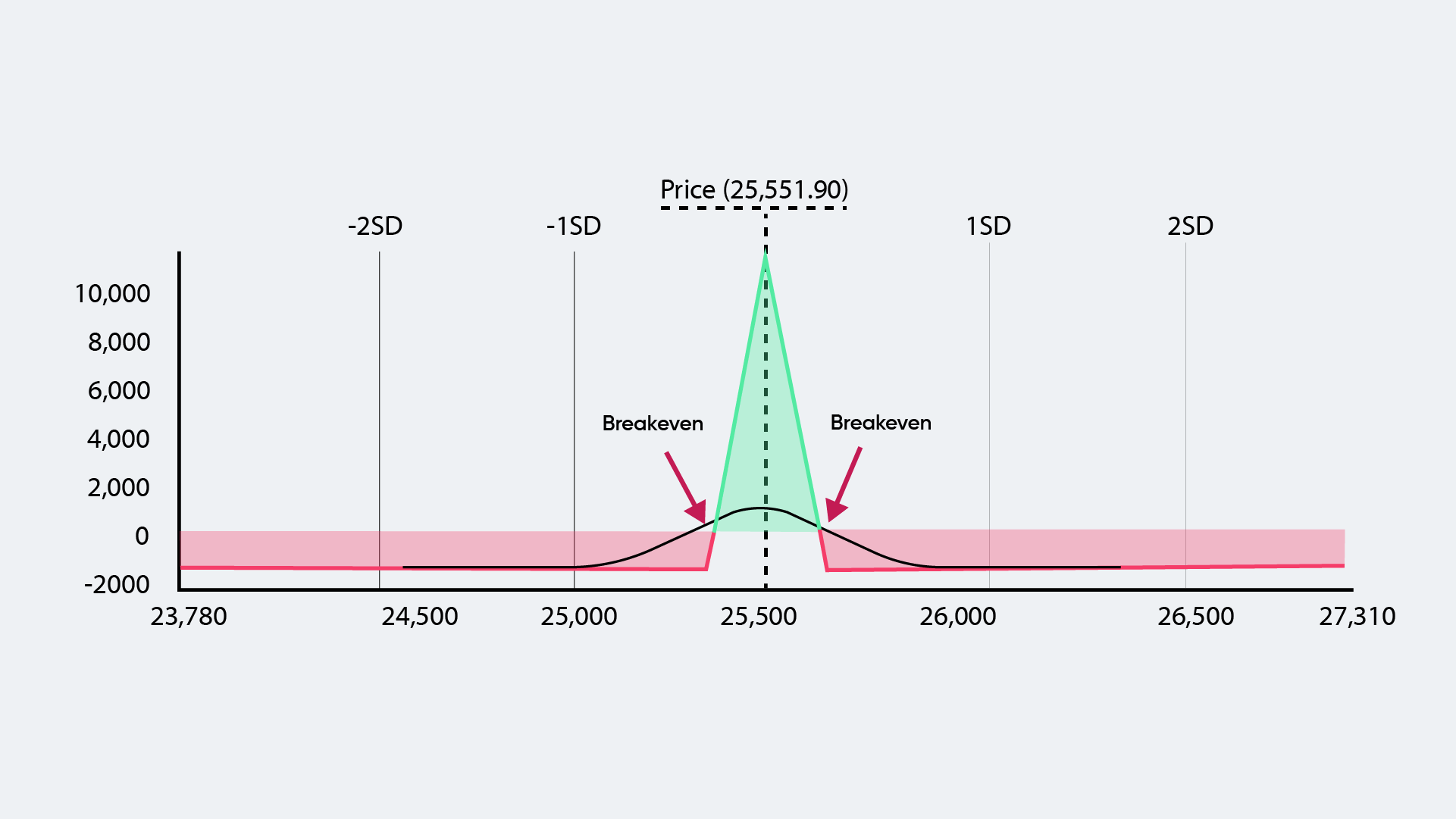

Breakeven Points of Long-Put Condor

Traders experience two breakeven points when they opt for a neutral- long put condor strategy. The strategy stays profitable as long as the underlying price stays between two breakeven points. The maximum profit gained from the long-put condor strategy is always limited. In addition, it is obtained only when the underlying price remains within two middle strikes.

Consequently, the long-put condor strategy becomes unprofitable if the underlying price falls or drops below the lower breakeven level or increases above the higher breakeven point. On the other hand, the minimum loss in this trading option is also limited to the level of net premium paid. The minimum loss will be experienced when the underlying price falls below or above the higher strike.

Advantages of Long-put Condor

- The strategy can achieve maximum profit potential with greater success probability than a long-out butterfly.

- Time-decay has gained in this strategy so long as it stays profitable

- Long put condor offer good risk to reward ration when a trader chooses the strikes well

- The strategy has limited minimum loss irrespective of how high or low the underlying price moves.

- Long put condor offers a wider maximum profit zone than a long butterfly.

Drawbacks of Long-put Condor

- There is the potential of losing the whole net debit sum when the underlying price drops below the lowers strike or rises beyond the upper strike.

- The trading account requires a greater margin when initiating a long put condor strategy since it involves selling two options.

- The maximum profit from the long-put condor strategy is smaller or equal in absolute terms to the butterfly's strategy.

- A rise in unexpected volatility may affect trade success when using a long-put condor strategy.

Risk in Long-Put Condor

The strategy has assignment and expiration risks. In some style options, the short trading options forming the body of the long-put condor strategy are subject to assignment at any time. When early assignment ensues on short-put options, traders may have to finance the stock for one business day. In addition, investors should be well-informed about situations in which the underlying is involved in capitalisation or restructuring. These include special dividends, spin-offs, takeovers or mergers, which can completely upset typical expectations about the early exercise of trading options on the stock.

On expiration risk, investors may experience uncertainty if underlying trade at levels below short pout strikes but are above the lower long put strike. In such a situation, the investors are likely to be assigned on short-puts leading to a long and unhedged position following expiration. When that happens, traders may be subject to an adverse move to the next day's business.

An Example of a Long-Put Condor

Let’s assume investor XYZ has executed a neutral- long put condor on Nifty. The strategy details and amounts in (Rs) include

- The strike price of out-of-the-money long-put is 8800

- The strike price of out-of-the-money short-put is 9000

- The strike price of in-the-money short-put is 9200

- The strike price of in-the-money long-put is 9400

- long-put premium = 60 (lower strike)

- short-put premium= 120 (lower middle strike)

- short-put premium=225 (higher middle strike)

- long-put premium=335 (higher risk)

- Net debit = 70(60+355-120-225)

- Net debit = 5, 2550(70*70)

- Breakeven point (lower) = 8870(8800+70)

- Breakeven point (upper) = 9330(9400-70)

- The maximum reward will be 9,750((9000-8800-70)*75)

- Risk (maximum) = 5,250

A table showing scenarios of Nifty’s position at the expiry date and effects on trade profitability.

| Underlying price at expiry | Profit or loss (net) | Notes |

|---|---|---|

| 7000 | 5,250 (loss) | Payoff=[(8800-7000,0)-60]+[120-(9000-7000,0)]+[225-(9200-7000,0)]+ [(9400-7000,0)-355]. That led to loss. Underlying price is below lower breakeven point at expiry date |

| 8000 | 5,220 (loss) | Payoff=[(8800-8000,0)-60]+[120-(9000-8000,0)]+[225-(9200-8000,0)]+ [(9400-8000,0)-355]. That led to loss. Underlying price is below lower breakeven point at expiry date |

| 8800 | 5,250 (loss) | Payoff=[(8800-8800,0)-60]+[120-(9000-8800,0)]+[225-(9200-8800,0)]+ [(9400-8800,0)-355]. That led to loss. Underlying price is below lower breakeven point at expiry date |

| 8835 | 2,625 (loss) | Payoff=[(8800-8835,0)-60]+[120-(9000-8835,0)]+[225-(9200-8835,0)]+ [(9400-8835,0)-355]. That led to loss. Underlying price is below lower breakeven point at expiry date |

| 8870 | No loss and no profit | Payoff=[(8800-8870,0)-60]+[120-(9000-8870,0)]+[225-(9200-8870,0)]+ [(9400-8870,0)-355]. No loss and no profit. Underlying price is equal to lowest breakeven point at expiry date |

| 8900 | 2,250 (profit) | Payoff=[(8800-8900,0)-60]+[120-(9000-8900,0)]+[225-(9200-8900,0)]+ [(9400-8900,0)-355]. That led to profit. Underlying price lie between two breakeven points at expiry date |

| 9000 | 9,750 (profit) | Payoff=[(8800-9000,0)-60]+[120-(9000-9000,0)]+[225-(9200-9000,0)]+ [(9400-9000,0)-355]. That led to profit. Underlying price lie between two breakeven points at expiry date |

| 9100 | 9,750 (profit) | Payoff=[(8800-9100,0)-60]+[120-(9000-9100,0)]+[225-(9200-9100,0)]+ [(9400-9100,0)-355]. That led to profit. Underlying price lie between two breakeven points at expiry date |

| 9200 | 9,750 (profit) | Payoff=[(8800-9200,0)-60]+[120-(9000-9200,0)]+[225-(9200-9200,0)]+ [(9400-9200,0)-355]. That led to profit. Underlying price lie between two breakeven points at expiry date |

| 9300 | 2,250 (profit) | Payoff=[(8800-9300,0)-60]+[120-(9000-9300,0)]+[225-(9200-9300,0)]+ [(9400-9300,0)-355]. That led to profit. The underlying price lies between two breakeven points at the expiry date |

| 9330 | No loss and no profit | Payoff=[(8800-9330,0)-60]+[120-(9000-9330,0)]+[225-(9200-9330,0)]+ [(9400-9330,0)-355]. No profit no loss. Underlying price is equal to higher breakeven points at expiry date |

| 9365 | 2,625 (loss) | Payoff=[(8800-9365,0)-60]+[120-(9000-9365,0)]+[225-(9200-9365,0)]+ [(9400-9365,0)-355]. That led to loss. Underlying price is above higher breakeven points at expiry date |

| 9400 | 5,250 (loss) | Payoff=[(8800-9400,0)-60]+[120-(9000-9400,0)]+[225-(9200-9400,0)]+ [(9400-9400,0)-355]. That led to loss. Underlying price is above higher breakeven points at expiry date |

| 10000 | 5,250 (loss) | Payoff=[(8800-10000,0)-60]+[120-(9000-10000,0)]+[225-(9200-10000,0)]+ [(9400-10000,0)-355]. That led to loss. Underlying price is above higher breakeven points at expiry date |

Based on the above scenarios, XYZ trader incurs the highest loss (5,250) if Nifty is below the lowest strike (8800) or above 9400, the upper strike. On the other hand, the maximum profit from the long put condor is 9,750 and gained if the Nifty remains between 9000 and 9200, which are the middle strikes.

The trader benefits from the strategy as far as the Nifty stay within the 8870 and 9330, the two breakeven points. In addition, the strategy is unprofitable once nifty goes outside the two breakeven points. The risk and reward ratio based on this strategy stands at 1.85.

Summary

The neutral-long put strategy is good for beginners to start trading without fear of much loss. The strategy has four different put options with the same expiration. Long-put condor earns a profit when the underlying security remains between two short-put strikes on the expiry time. The strategy also has limited maximum loss and maximum gains. In addition, the long-put condor exhibits two breakeven points.