Why Aswath Damodaran believes Zomato deserves an even lower valuation?

2021 was a terrific year for the stock market. Investors saw 2x 3x even 5x gains in their portfolio. Many companies made a debut in the markets to benefit from sky-high valuations. One of them was Zomato, a loss-making, cash-burning company that had the potential to grow exponentially.

Investors were highly optimistic about its performance, and you see when there is a bull market, investors are optimistic about most things.

But one man who is known for his complex yet thorough valuation models, had a completely different view from investors. He valued Zomato at Rs. 41.

Investors just susshed him and told him, we know better. The company got listed at Rs.76. Not only that, in late 2021 its share price flirted with new peaks and went up to Rs. 169.

But as they say, the houses that are hollow, leak the first in the monsoon. With the bear market, Zomato's stock price has plummeted. Its share price has fallen by 49% in the last six months, while the benchmark index NIFTY50 fell just by 2.37% in the same period.

The fall in the share price can be attributed to ballooning losses, its acquisition of Blinkit, and macroeconomic factors as well.

Its share price touched a low of Rs. 41 on 26th July, and everyone across the social media was like, Aswath Damodaran said it so. It was kind of a moment when your astrologer told you about an event that can happen and that event occurs and you are like she is the god.

Well, the guru has come up with a revised valuation for Zomato, and its even lesser than his earlier valuation. He valued Zomato at Rs. 35.32 per share. Now the question is why did he revalue it again and why he decreased the company’s valuation.

So, the change in valuation was because of two things,

1. Change in the fundamentals of the company, post its listing

2. Change in the macroeconomic condition of our economy

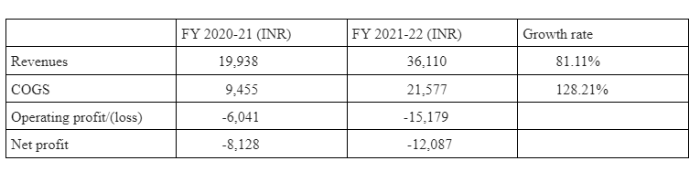

Post its IPO, the company has come up with four quarterly results and these results carry both good and bad news for investors. The good news is food delivery market has grown in the last one year, and the market has mostly consolidated with Zomato and Swiggy ruling most of it. As a result, the revenue and gross order value (total value of orders placed on its platform, value includes everything taxes, delivery charges, and discounts but excludes the tips) both have increased in the last one year, which indicates the food delivery market has grown and Zomato has been a beneficiary of this growth. The GOV has grown from Rs. 94.8 billion to Rs. 213 billion, while its revenue has grown from Rs. 19 billion to Rs. 36 billion.

Another good news is that the company is well off when it comes to its liquidity position, as its cash and short term investments were around ₹68746 (including short term investments) in March 2022. Having a heavy purse, would ensure that the company can sustain downturns.

Now comes the bad news, the company’s costs and its losses have grown at a much higher rate than its revenue. This implies that even though the GOV is increasing, its costs like delivery charges, discounts, and employee expenses are increasing at a higher rate. The revenue of the company has grown by 81% in the last one year, while its losses has grown by 151%.

The management speaks of economies of scale, but the numbers clearly don’t say so!

Coming to macroeconomic factors have resulted in a low valuation for Zomato.

A lot has changed in the one year, the time when Zomato got listed. Last year, most economies were booming, and markets were at their all-time high. Investors had the appetite to invest in loss-making budding startups, but things have changed drastically now. Two things that have affected the markets and investor perception are

Inflation and Scarce risk capital

Inflation across the globe is at an all-time high, so whenever the inflation or mehengai is high, a general measure taken by the central banks is to increase interest rates, so that people deposit their money into the bank and there is less money available for them to spend.

F.D. returns in India are typically between 5.5% and 6%; however, if you are investing in a more risky asset class, then naturally you can expect higher returns. Say you are investing in equity, that means you are taking the risk that your capital can go to even 0, so naturally if you are investing in a risky asset class you would expect more returns than risk-free investments.

This in simple terms is a Risk premium.

The riskier the investment, the higher returns an investor would expect.

Whenever the interest rates are low, investors do not earn a significant return on it, so they tend to take a higher risk on their capital and invest in risky assets, but when interest rates are high tend to refrain from investing in risky assets.

In addition, when interest rates are high, such as 6.5% - 7.5% on an FD, you would expect higher returns from other investments. Therefore, as inflation increases, risk capital becomes scarce in the market and investors reallocate their capital, which leads to a decline in prices.

As inflation increases, investors start shifting their capital toward companies with high margins, pricing power, and sustainable cash flows.

Because when the market is bullish, everyone trades and speculates on the price but when the markets are bearish, people try not to burn their hands and invest in fundamentally good companies.

- Flat ₹20 Brokerage

- Next-gen Trading

- Advance Charting

- Actionable Ideas

Trending on 5paisa

5paisa Research Team

5paisa Research Team

Sachin Gupta

Sachin Gupta

Tanushree Jaiswal

Tanushree Jaiswal

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.