Long Put Ratio Backspread Strategy

The popular bear put ratio has bottomed out and is now making new highs. This bullish-put ratio is poised to continue on its run because it is not in the process of being squeezed. It will likely continue to make new highs until we see a pullback and reversal.

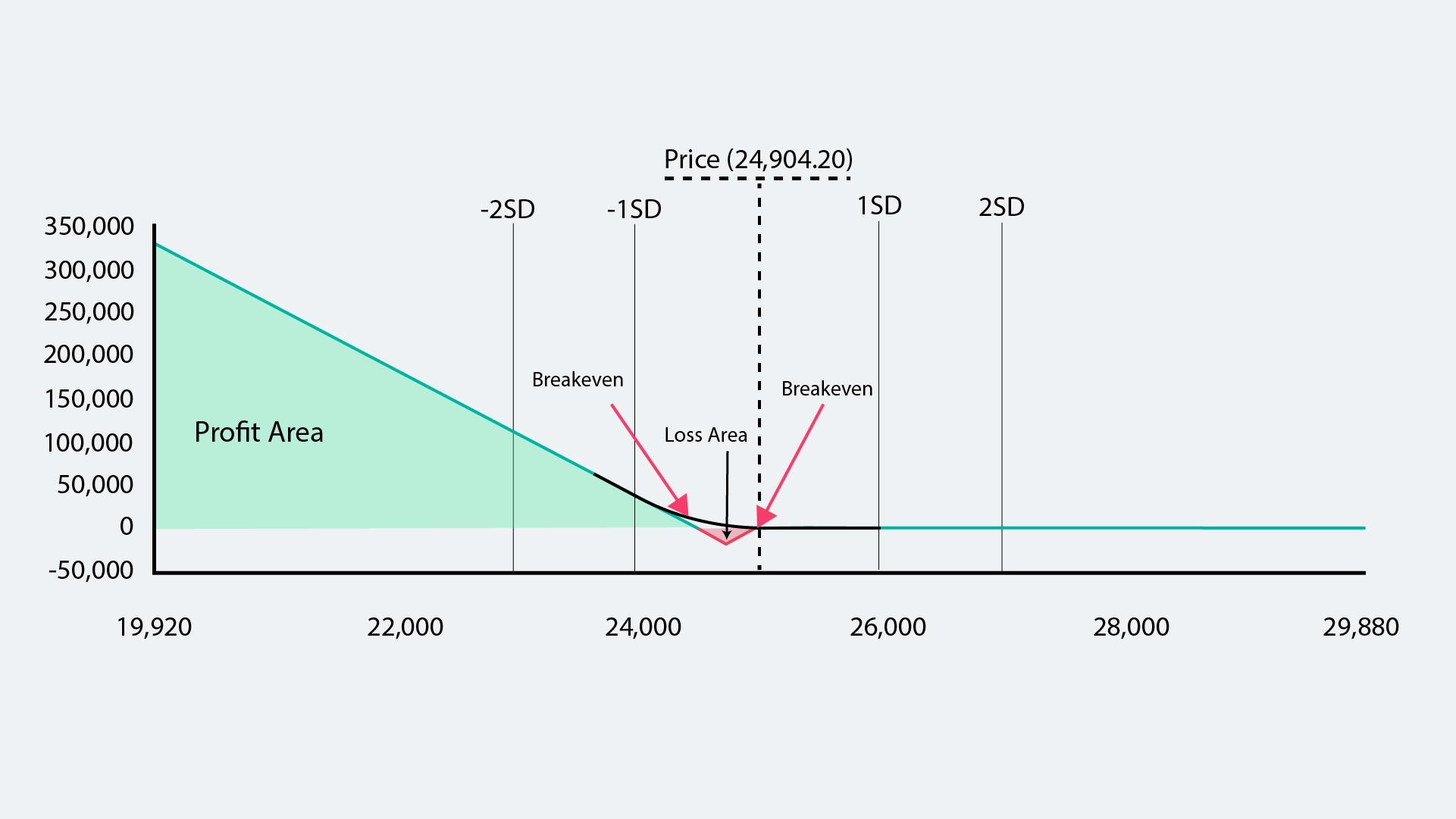

What is the Bearish-Put Ratio Back Spread?

The bearish-put ratio back spread is a limited risk options strategy used to achieve large profits on a downward move in the market. It combines puts and calls to give the trader limited risk while making unlimited money.

The bearish-put ratio back spread should only be used by traders comfortable with high probability trades with limited risk. The maximum loss equals the original credit received when opening the trade. The leverage provided by these positions is unrivalled and, for those experienced enough to use them, can yield great profits on even small moves in the underlying stock price.

The bearish-put ratio back spread has a high probability of success and is effective when the stock price is trending nicely in one direction. It also performs well when used on short term options with an expiration date of a few weeks.

Illustration of Bearish- Put Ratio Back Spread Through an Example:

Suppose a trader has $500,000 available to trade and plans to use it for day trading. The trader wanted to use the entire $500,000 for one day. The trader decides to open a bearish-put ratio back spread. Using his trading platform, the trader bids 25 cents and receives 35 cents on his options position. The trader will also get 50 cents back on the original credit that he used to open the position.

The investor decides that he would like to have a stock market outlook of 75% and an option expiration of 3 weeks after entering into this trade. The investor's platform returns the following values: The stock price will have to move down 8.08% for the trade to cover its costs. The trader is risking $500,000 divided by $1.35 (cost per option) times 100 minus three, which equals $485,022.22 risk exposure.

The break-even range for this trade is calculated as follows: ($1,000 – 25cents) divided by $1.35 times 100 minus three which yields a result of -$0.7725 or -77.25 points in the downside direction for this trade to break even at the current stock prices ($1,000 per option). A move of 8.08% requires the stock to fall by -$0.7725 times 100 minus 80 which equals a total of -8.08% for the trade to break even at current prices ($1,000 per option). The trader's risk exposure will not be exceeded if the stock falls below $1,000 per option. In this case, the trader will risk being margin called on his position if he is margin trading.

The maximum loss on this trade will be equal to 35 cents divided by $1.55 times 100 minus 3 which equals a maximum loss of $27,149.70. This loss will occur if stock prices move up to $1,000 and the option is priced at $1.55 times 100 minus 3 or $3.25 per option (pricing implied volatility) for this trade to return all of its costs. Thus the maximum risk on this trade would be -$27,149.70 or -$27,149 should the stock price reach $1,000 per option, and there be no further upward movement in the stock prices after reaching this level further downside movement in stock prices than what was already assumed.

The maximum loss on this trade will be equal to 35 cents divided by $1.35 times 100 minus 3 which equals a maximum loss of $26,084.04. This loss will occur if stock prices move up to $1,000 and the option is priced at $1.35 times 100 minus 3 or $2.95 per option (pricing implied volatility) for this trade to return all of its costs. Thus the maximum risk on this trade would be -$26,084.04 or -$26,084 should the stock price reach $1,000 per option, and there be no further upward movement in the stock prices after reaching this level or any further downside movement in stock prices than what was already assumed.

The best scenario will be if the stock price stays below $1,000 per option at expiration. The trader will have made a profit of $15,044.04 or 15% on this trade. The full theoretical profit is $30,089.70 or a 30% return on risk capital at the expiration date if stock prices remain below $1,000 per option at expiration and all costs are collected with no change in implied volatility up to that point.

The Strategy of Bearish-Put Ratio Back Spread:

Like any other put call spread strategy, the bearish-put ratio back spread consists of a long-stock position and a short-stock position. The long stock position comprises one call option and one put option. The short stock position comprises one call option and one put option. The long-stock position creates unlimited profit on a long term move down at the underlying stock price. The unlimited profit can be achieved when the stock price moves to zero.

The short-stock position will be used to absorb all losses due to any unforeseen down moves in the stock price. This can help protect from any catastrophic loss or one that is larger than what the trader had originally planned for due to a large downward move in the stock price. The short-stock position can also help protect the trader from a very large or sudden downward move in the stock price if the trader is trading in a margin account. This would allow the trader to continue to trade this spread if he wanted to by adding more capital.

The bearish-put ratio back spread has unlimited risk on the downside and limited upside. The unlimited loss occurs when stock prices move beyond all pre-determined stop losses, and there are no further down moves in stock prices after this point. The limited risk on the upside will equal the net credit received when the bearish-put ratio back spread is opened. This net credit will help limit the trader's maximum loss exposure. If a stop-loss were placed on this trade, then the limited risk on the upside would also equal the stock price minus all possible stop losses.

The bearish-put ratio back spread can be used by traders in many different ways depending on their trading objectives, time frames for trading and their overall risk appetite. It can be used for a long term approach to trading. Its primary purpose is to collect option premiums and create income while adding downside protection to a portfolio of stocks to create more stable returns in percentage terms.

Strategy Table:

| Market Expiry | ITM_IV | PR | ITM Payoff | OTM_IV | PP | OTM_Payoff | Strategy Payoff |

|---|---|---|---|---|---|---|---|

| 6500 | 1000 | 134 | -866 | 1400 | 92 | 1308 | 442 |

| 6600 | 900 | 134 | -766 | 1200 | 92 | 1108 | 342 |

| 6700 | 800 | 134 | -666 | 1000 | 92 | 908 | 242 |

| 6800 | 700 | 134 | -566 | 800 | 92 | 708 | 142 |

| 6900 | 600 | 134 | -466 | 600 | 92 | 508 | 42 |

| 7000 | 500 | 134 | -366 | 400 | 92 | 308 | -58 |

| 7100 | 400 | 134 | -266 | 200 | 92 | 108 | -158 |

| 7200 | 300 | 134 | -166 | 0 | 92 | -92 | -258 |

| 7300 | 200 | 134 | -66 | 0 | 92 | -92 | -158 |

| 7400 | 100 | 134 | 34 | 0 | 92 | -92 | -58 |

| 7500 | 0 | 134 | 134 | 0 | 92 | -92 | 42 |

| 7600 | 0 | 134 | 134 | 0 | 92 | -92 | 42 |

| 7700 | 0 | 134 | 134 | 0 | 92 | -92 | 42 |

| 7800 | 0 | 134 | 134 | 0 | 92 | -92 | 42 |

| 7900 | 0 | 134 | 134 | 0 | 92 | -92 | 42 |

| 8000 | 0 | 134 | 134 | 0 | 92 | -92 | 42 |

Advantages of the Bearish-Put Ratio Back Spread:

- The bearish-put ratio back spread has limited risk due to the short stock position. The break-even point will occur when the stock price moves -$0.7725 times 100 minus 80 or -8.08% in the downside direction from current stock prices ($1,000 per option).

- This trade has unlimited profit potential due to the long-stock position. The maximum profit will be achieved when a move of +$0.7725 times 100 minus 80 or +8.08% occurs in the upside direction from current stock prices ($1,000 per option).

- A smooth trending market is required for this trade to perform well. The shorter the time frame for expiration, the more volatile the stock price will become, making it difficult for the trade to perform well.

- The trader must be prepared to close this trade out when it is used as protection or in a situation where a large share of profits is already realized. This can pose a challenge when taking on much larger positions in the stock than initially planned.

- This strategy can be used for both short-term and long-term value.

Wrapping Up:

The bearish-put ratio back spread can be used to create unlimited profits throughout a trend in the stock price. The trade should be used when the market is trending strongly and there is no real reason for an uptrend in the underlying stock prices.

This trade needs to have a good amount of time until expiration to ensure that it is used as protection instead of as a way to make large profits early on. Good traders will use this strategy when they are unsure which path their options will take. They will also use it for day trading only if they feel that their risk exposure can handle this trade size.

More Derivative Strategies

- Bullish Short Put

- Bullish Bull Call Spread

- Bullish Long Call Butterfly

- Bullish Ratio Call Spread

- Bullish Call Ratio Back Spread

- Bullish Bull Call Ladder

- Bullish Bull Put Spread

- Bullish Bear Call Ladder

- Bearish Long Put

- Bearish Bear Put Spread

- Bearish Bear Call Spread

- Bearish Bear Put Ladder

- Bearish Long Put Butterfly

- Bearish Bear Bull Put

- Bearish Ratio Put

- Bearish Short Call

- Bearish Put Ratio Back Spread

- Neutral Diagonal Put

- Neutral Long Iron Butterfly

- Neutral Short Straddle

- Neutral Straddle

- Neutral Diagonal Call

- Neutral Calendar Put Read More