5paisa Research Team

5paisa Research Team

Sachin Gupta

Sachin Gupta

Intraday in Stocks vs 24x7 Crypto Trading: Which Actually Works for Retail Investors?

by

5paisa Research Team

16th May 2025

Recently the total Demat accounts in India crossed a historic benchmark of 10 crores. Not to brag about our business, but the retail participation in the equity markets in India has grown by leaps and bounds in the last few years.

The total number of Demat accounts in India were only 4 crore till 2020, but the figure has now crossed the 10 crore threshold. This means we have opened more accounts in the last two years than ever.

From a time when investments were synonymous with keeping savings in an FD to a time when people are seeking knowledge on investing in Crypto, NFTs, and Stocks, we have come a long way.

In the last two years, we did witness a change in the attitude of people towards the stock market. Financial literacy, lack of a fixed revenue source due to COVID, and hassle-free broking services by discount brokers like us? are some reasons we are witnessing this shift.

But financial markets still have a long way to go because even today only 4%-5% of Indians directly invest in stock markets compared to 55% in the US.

Discount brokers, Portfolio managers are all racing to get a pie of enormous growth in the industry. Amongst all, there is one player that is definitely going to benefit from the growth in capital markets and that player is CDSL.

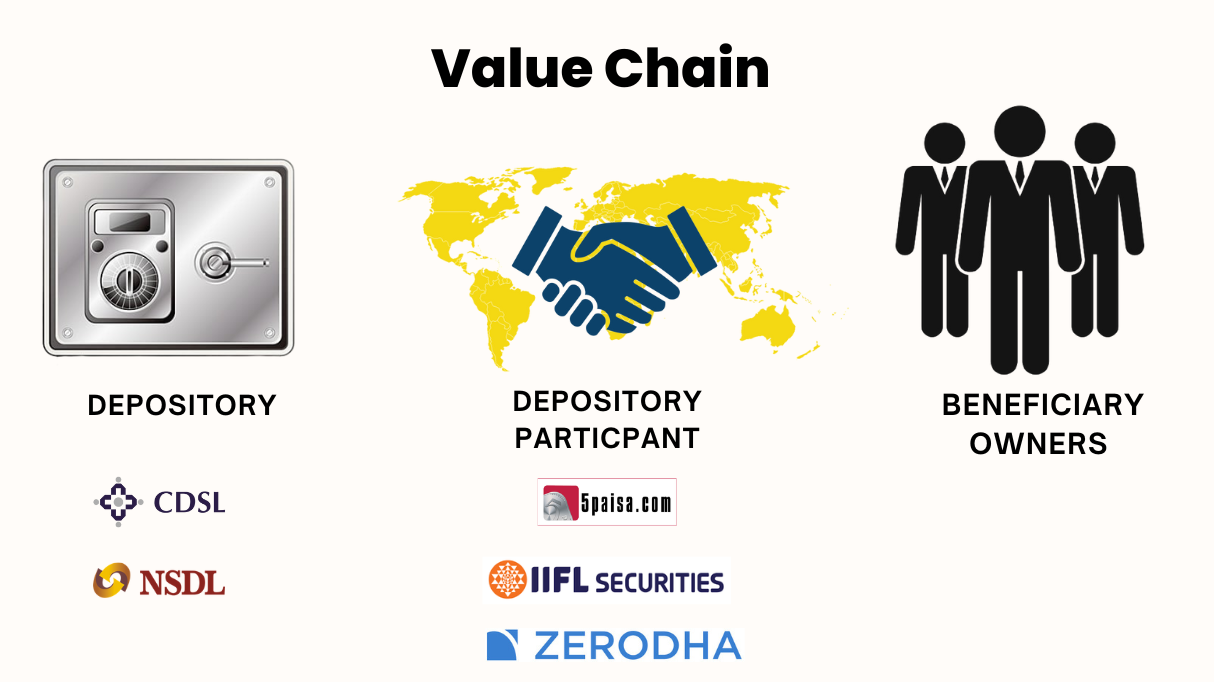

CDSL promoted by the Bombay Stock Exchange is one of the two depositories in India. Before getting into the business of CDSL, let’s learn what exactly is a depository. So, just like your bank stores your funds in electronic form, these depositories store your securities like equities, debentures, bonds, etc in electronic form.

A lot of you might be of the opinion that your shares are stored with your broker but that is not the case. They are stored with depositories. Discount brokers and Traditional brokers act as an intermediary between investors and depositories. They are known as Depository Participants. So, think of a depository as a “tijori" that stores your financial securities in digital form.

The main operations of CDSL include holding and transacting securities in electronic form and settlement of trades executed on stock exchanges. These securities include equities, debentures, bonds, Exchange Traded Funds (ETFs), units of mutual funds, units of Alternate Investment Funds (AIFs), Certificates of deposit (CDs), commercial papers (CPs), Government Securities (G-Secs), Treasury Bills (TBills), etc.

Another depository is NSDL which is promoted by National Stock Exchange.NSDL is short for ‘National Securities Depository’, whereas CDSL stands for ‘Central Depository Services Limited.

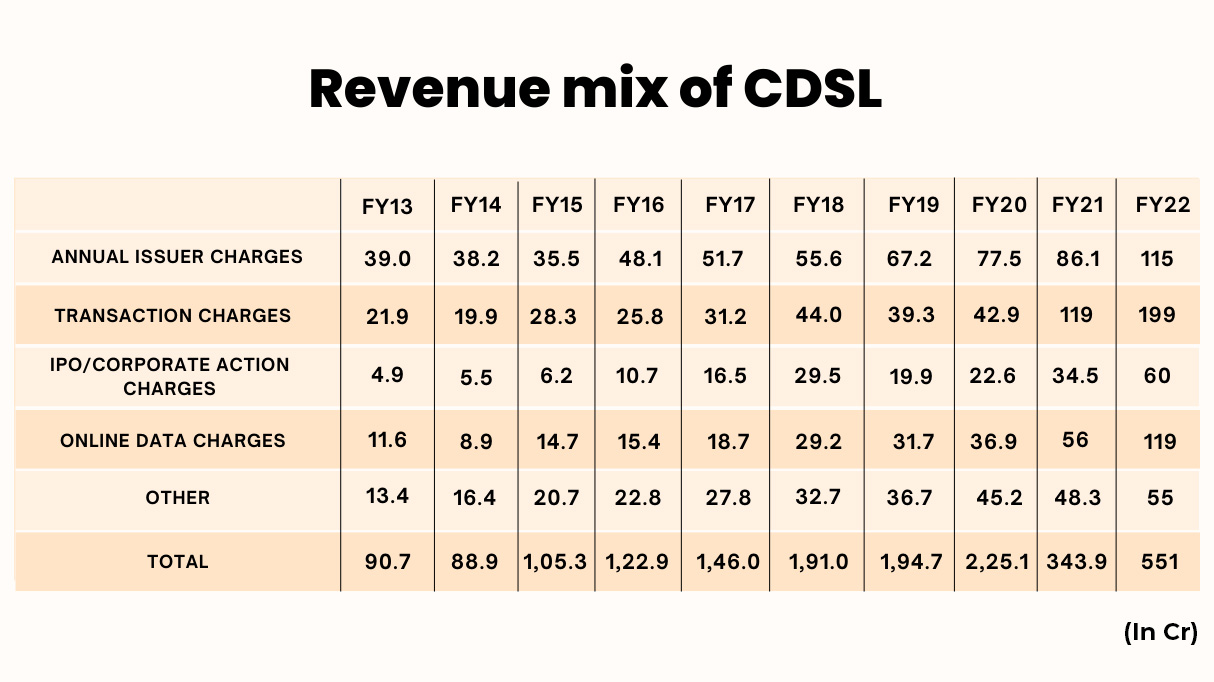

Annual issuer charges:- CDSL charges corporates as annual issuer fees. All the corporates, listed or unlisted, have to pay these charges for dematerialisation of their securities to depositories. This fee is decided by SEBI and is the same for both depositories. It is currently levied at a rate of Rs. 11 per folio (ISIN position) subject to the Nominal Value of Securities admitted (Paid-up capital). Annual Issuer charges for FY 2021-22 stood at ₹ 11,540.21 lakh as compared to ₹ 8,611.89 lakh for FY 2020-21, which has increased by 34%. With more companies raising funds from the capital markets, annual charges are bound to increase in the coming years.

Transaction Charges:- For any transaction done by an investor, the broker has to pay a fixed amount to CDSL for the transaction settlement. These charges depend on the number of transactions done by the investors and not much on the value of transactions. Depositories charge DP’s on every debit transaction in the market. While NSDL charges a flat fee of Rs.4.5, CDSL charges DP’s a fee on a slab rate based on their total monthly bill. The slab based fee structure of CDSL appeals to DPs and hence it is able to attract more DP’s than NSDL. The revenue from transaction charges depends on the number of transactions happening in the market, which is dependent on investor sentiment and market conditions. Therefore revenue from transaction fees is highly volatile for the depositories. In FY21-22 transaction charges stood at ₹ 19,948.35 lakh 67% higher than FY 2020-21.

Online data charges:- CDSL through its subsidiary CDSL Ventures Ltd (CVL) provides KYC service to capital market intermediaries like Mutual fund companies etc. CVL is the largest KYC Registration Agency (KRA) in India, with 60% of the market. The primary revenue in the segment includes one-time charges for KYC creation of customers and the fees for providing data of customers to intermediaries. Currently, CVL charges Rs.15 for the creation of each KYC and Rs35 for data fetching to the intermediaries. The revenue from online Data charges increased by 114% to ₹ 11,997.96 lakh in FY 2021-22 as compared to ₹ 5,616.77 lakh in FY 2020-21

IPO & corporate action charges:- Whenever a company comes with an IPO or it performs any corporate action like rights issue, bonus issue, or stock splits they have to pay depositories for these actions. This revenue source of CDSL is also dependent on capital market sentiments as most companies launch their IPOs when there is a bull in the market. For ex. In the last two years, IPOs were raining due to the bull run. Therefore this revenue source of CDSL is also volatile and highly dependent on the market. The revenue from IPO and Corporate Action charges increased by 84% to ₹ 6,053.12 lakh in FY 2021-22 as compared to ₹ 3,285.55 lakh for FY 2020-21

Other segments:- In addition to the above sources, the company also earns revenue from account maintenance fees, e-voting fees, and ECAS fees.

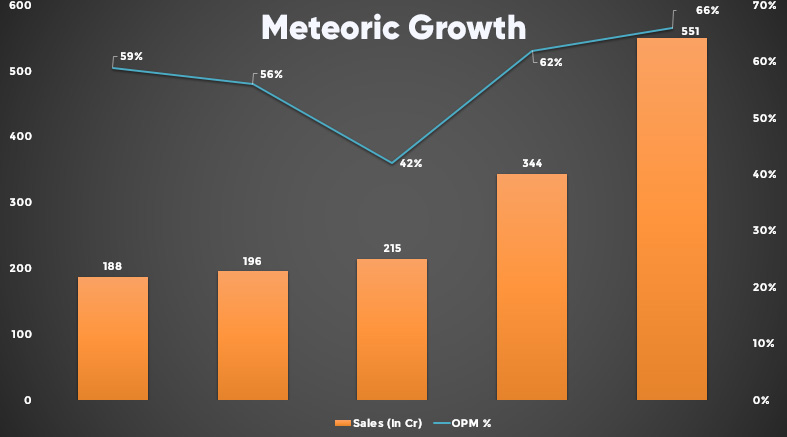

In the last five years, CDSL has grown its revenue at a CAGR of 24%. It operates on an asset-light model due to which most of its revenue flows down to profits. In FY 22, it had an OPM of 66%.

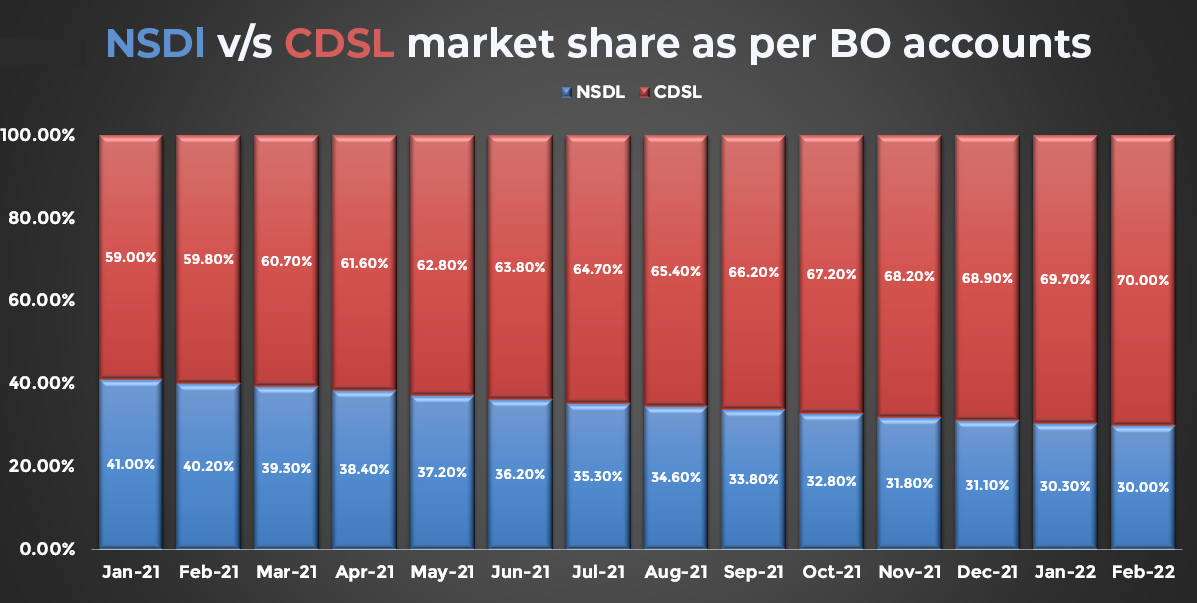

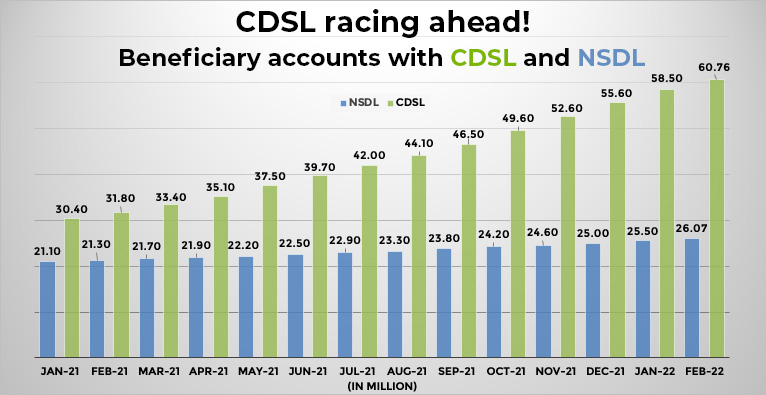

Though it came into existence a few years after NSDL, it has a market share of around 70% in terms of beneficiary accounts. Due to it attractive slab-based pricing or better technology. It has continuously gained market share from NSDL in the last few years.

In the coming years, it will benefit from the growth in the capital markets. The duopolistic nature of the industry, high entry barriers, and attractive charges would contribute to its growth.

Regulatory compliance: No business is perfect, and neither is CDSL’s, the company is strictly regulated by the market watchdog, SEBI, due to which it does not have pricing power and can only compete with NSDL by providing better services to DPs.

Appointment of Central Registry of Securitisation Asset Reconstruction & Security Interest of India (CERSAI) as the central KYC registration agency could impact the KYC business of CDSL Ventures.

Overall capital market sentiments: While our studies suggest no direct correlation to equity markets (also given that a mere 25% of revenues is directly linked to market movements), any change in investor sentiment can have a direct bearing on transaction charges and related services.

Being in the business of technology, risk due to cyber-attacks cannot be ruled, and hence, remains one of the biggest risks.

Indian Stock Market Related Articles

Intraday in Stocks vs 24x7 Crypto Trading: Which Actually Works for Retail Investors?

Checklists to Stay Calm During Volatile Markets

What to Do When Your Portfolio Is in the Red? A Rational Look at Market Downturns

How a Diversified Portfolio Can Help in Situations Like War, Pandemic, etc.

How to Use F&O to Manage Risk in a High Volatility Market: Advanced Hedging Strategies

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.