5paisa Research Team

5paisa Research Team

Intraday in Stocks vs 24x7 Crypto Trading: Which Actually Works for Retail Investors?

by

5paisa Research Team

16th May 2025

I’ll share a real incidence with you guys, so when Zomato came with an IPO, some my colleagues we were researching on it and we did a bit of scuttlebutt exercise in our office, so there is one colleague of mine, who is the most loyal Zomato customer and orders food every now and then, we just opened his order history and guess what we got?

He had ordered food worth Rs.70,000 from his account in an annual year! I know you are as shocked as I am!

Not just him even for me food is everything, it the first thing on my mind when I start my day, and probably it is the only thing that is on my mind every second. And I believe everyone has a love for food in India. I am writing this blog while my order of Pao Bhaji is on its way.

Have you observed, in no time these companies have become a part of our lifestyle, like you got a promotion let's order food, there is lauki in the lunchbox, lets order food!

Zomato’s business seems perfect from a consumer point of view, but is it a lucrative business to invest in? You’ll find out today! Also I will try my best to not bring my love for food and Zomato’s social media team in between of this analysis! Pinky Promise.

Zomato recently came up with its FY 22 results which painted a rosy picture.

Here are they key takeaways

Revenue from operations in FY22 stood at Rs 4,192.4 crore as against Rs 1,993.8 crore in FY21.

Its net loss increased to Rs 1,222.5 crore from Rs 816.4 crore in the previous financial year.

After the fabulous results, its share price rose by 18% on Tuesday, which had been falling since its listing.

Good Results, Stock price up! Party over!

Well, if you observed, above we mentioned , its result painted a rosy picture, well that means the company’s results are not as good as they seem on the surface.

The company’s quarterly earnings have more or less flattened in the recent quarters, losses have been ballooning and the company has no clear idea, how and when its food delivery business and Blinkit will be on their path to profitability.

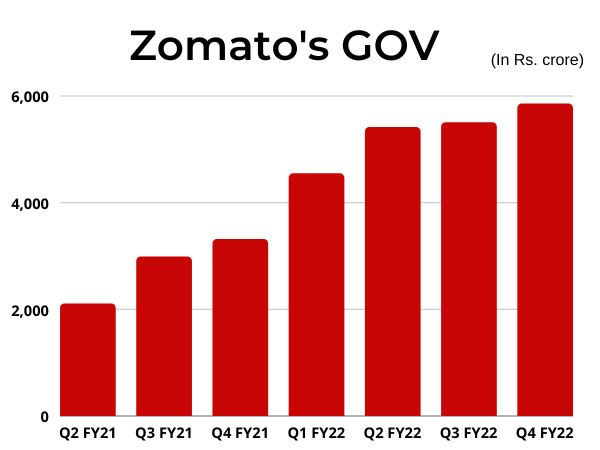

One thing that exhibits their stagnant growth is their GOV, Gross order value is the total money that a company makes from orders and it includes delivery charges, commission etc,

GOV has increased in the last few years dramatically due to the pandemic, because you see people who order from these apps mainly were millennials or people working in cities, who did not have time to cook, now the dynamics have changed, people are working from home, they are ordering for their families and hence the GOV has gone up.

Further, during the pandemic a lot of high end restaurants have also listed them on food delivery apps due to which the GOV has increased, but if you look at the recent quarterly it has been hovering around 55.5 billion.

Wish its GOV could grow as fast as its food delivery! Wait am I making a joke of its slow growing GOV or its 10 min food delivery? ?

Moving on, Stagnant growth of its GOV is not the only the thorn in its flesh, Another major problem with the food aggregator is the revenue concentration, the company in its recent quarterly report mentioned that around 60% of its GOV comes from top 8 cities and around 99% of is GOV comes from top 300 cities. Any guesses Zomato is present in how many cities?

Not 500, Not 800, 1000 cities. Yes, that means its operations in 700 cities bring less than 1% of its revenue. Even after so many years of operations, its revenue is concentrated in a few cities.

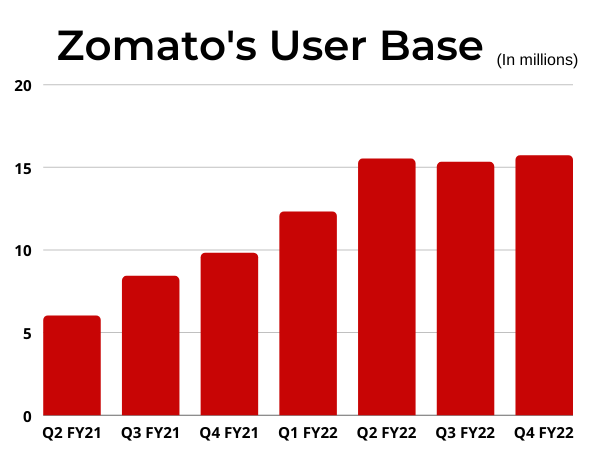

Not just the revenue concentration in higher in a handful of cities, it seems as if the Zomato magic is not working in tier 2 and tier 3 cities as the number of monthly transacting users( number of people who order at least once from Zomato) are stagnating.

They witnessed a phenomenal growth in the past few years because of the pandemic, but with opening up restaurants and increased dine in activity, they are witnessing a snaillike growth.

This means it has to focus more on a handful of customers and have to make them order more frequently to increase the GOV. In its recent call, the management mentioned that 90% of their business comes from repeat customers and even in the future they would be focusing more on the repeat orders rather than acquiring new customers.

Which is probably a good sign as it would lower down its cost of acquiring customers and would narrow its losses.

Let’s talk money

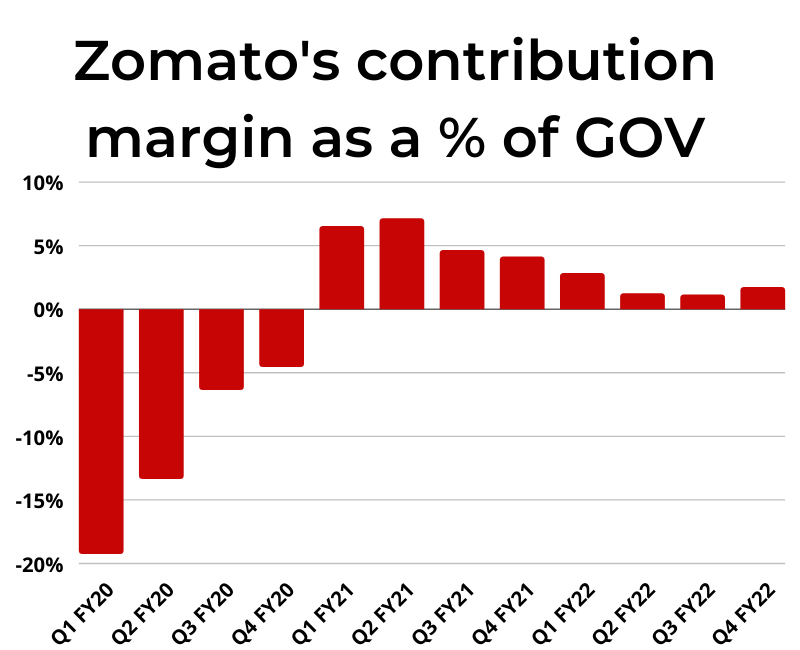

One concern that has been among the investors for most start ups that have listed this year is the profitability, most of these blooming start-ups are loss making, and investors are concerned about their profitability, same goes for Zomato as well. It's contribution margins, basically, the profit Zomato makes on each order. When it came with an IPO, it boasted about how in FY21, the company had a positive contribution margin, but guess that was just an IPO thing as its contribution margins as a % of GOV have been on a decline.

High market share, Increase in the middle income population can definitely contribute to its growth in the long term, but we cannot ignore the fact that the company had a dream run amidst the pandemic and it would have to work towards sustaining the growth as well towards being EBITDA positive.

01

5paisa Research Team

5paisa Research Team

Indian Stock Market Related Articles

Intraday in Stocks vs 24x7 Crypto Trading: Which Actually Works for Retail Investors?

Checklists to Stay Calm During Volatile Markets

What to Do When Your Portfolio Is in the Red? A Rational Look at Market Downturns

How a Diversified Portfolio Can Help in Situations Like War, Pandemic, etc.

How to Use F&O to Manage Risk in a High Volatility Market: Advanced Hedging Strategies

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.