RBL Bank: Another Yes Bank in Making?

Last Updated: 9th December 2022 - 04:41 pm

RBL bank’s share price plunged 22% after the appointment of R. Subramaniakumar as its MD and CEO, now you may ask why did the markets react so much to a hiring?

Well, RBI has a history of appointing ex- PSU bankers in the top management of private banks, when there is a lot of rot in the financials, and they want to clean up the mess.

Yes Bank, Laxmi Vilas Bank are living examples of that.

So, is there something really wrong with the Bank? On the surface, the company claims everything is fine and this is just a routine exercise by the central bank, even the RBI clarified that the asset quality of the bank is fine.

But all these efforts couldn’t stop the share price of the company from plunging, because RBI’s appointment was such, Subramaniam’s expertise in reviving the bad banks can be compared to Daya's expertise in breaking the darwaza! Don’t kill me for the bad analogy. ?

He has a reputation of reviving the banks with rotten balance sheets, and bad loans, he is a go to person for RBI, when they want to pull a bank out of mud. His career history says it all. He was associated with PNB bank for 35 years till 2016. During his tenure, he strived to transform the bank by leveraging technology. Under his leadership, PNB bagged a string of firsts to its name – first state-owned bank to launch RTGS online, the first to have the largest Finacle core banking system setup, – the kind of stuff that PNB still likes to brag about in its investor presentations.

After that he was appointed executive director at Indian Bank, which was under the Prompt corrective action framework of the RBI, it is basically a sort of black list that the RBI maintains for all the banks that have too many bad loans. Just like a list that our teacher use to have of all the notorious back benchers.

After his spectacular performance, in just one year, he was appointed as the managing director of Indian overseas banks, due to his amends and prompt action, the bank came out of the framework in 2021.

After he retired in 2019, RBI appointed him the administrator of shadow bank DHFL, whose loan book was hiding a lot of secrets and fictitious loans worth Rs. 11,000 crore, he worked tirelessly with the stakeholders and the company saw successful insolvency proceedings.

With a track record like that if RBI has appointed him for RBL bank, then its prudent we dig deeper into the company.

First and the foremost thing that reflects a bank’s health is the CASA ratio, so to put it simply a bank’s business is to get deposits from people in the form of current accounts and savings accounts and lend that money to people who need a loan. Say a person deposited Rs. 1000 with a bank, then the bank would give him a interest of 3% and would lend that money to another person and charge 10% interest from him, now this 7% is the money that bank makes. Simple right?

So, CASA ratio what is tells is how much money the bank has in the form CA&SA deposits as a % of their total deposits, if the number is high, it implies that bank is getting most of its deposits through CASA, where in they have to pay very less interest, the higher it is the better it is but in case of RBL bank their CASA ratio is just around 35.3%, just to give you a reference big players like HDFC, ICICI and Kotak have a CASA ratio of 48%, 45% and 60%, clearly on a much higher side.

Low CASA implies that RBI is getting most of its money through term deposits, of which the interest rates are high. It implies that of cost of funds for RBL are on a higher side.

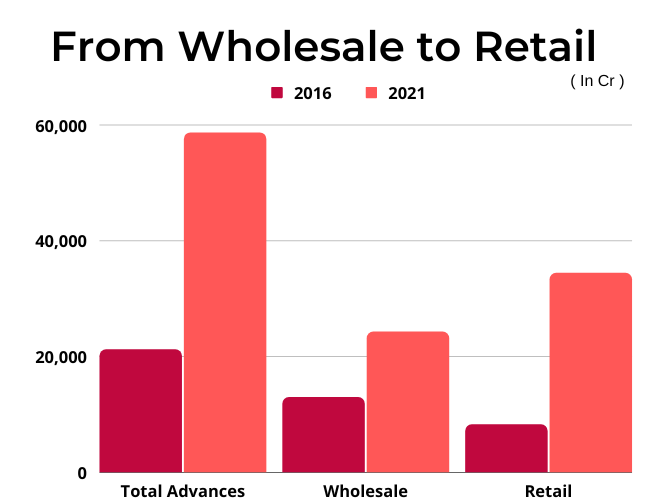

Now generally banks either lend to corporates or normal people like you and me, the former is known as wholesale lending, the latter is known as retail lending.

Generally whenever a company lends to corporates, the loan size is bigger and the default could cause a major dent on the balance sheet of the company. Remember Vijay Mallya, Nirav Modi? How banks have written off thousands of crores for them? So, wholesale lending is on a bit riskier side.

But, RBL was doing it right, under Vishwavir Ahuja, the former CEO of the bank, it lend to some of the cleanest corporates in the India like Tata and Mahindra, but then because of back to back corporate frauds, the company shifted gears and focused on retail lending, in 2015-16, wholesale loans made up around 61% of its total loans, which are now just 48% of its total loans.

At that time, since the wholesale loans crippled the entire banking sector the move seemed right, but then retail loans come with their own set of risks. Now, In the retail lending, RBL had to compete with giants like HDFC, Kotak and ICICI, to compete with them, it either had to lend at lower interest rates or had to give out unsecured loans, Vishwavir chose the latter option. Although the move was risky, he had to take his chances, because due to lower CASA, the cost of funds was already high for RBL, there was no way it could compete with the giants. The bank started giving out unsecured loans to the point that as of September 2021, unsecured loans made up 65% of its retail loan book.

The same figure for HDFC is just 3%!

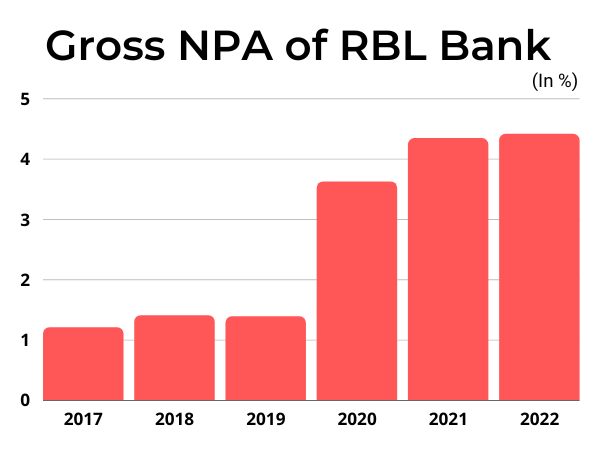

Unsecured loans were risky, he knew it but he did not know that a deadly pandemic would hit all of us, and people would be unable to pay their loans. After the pandemic, people started defaulting on their loans. The defaults started increasing and so did the NPA’s of the company, these are basically loans that people won’t repay back. The GNPA’s of the company have increased from 1.2% in 2017 to 4.41% in 2022.

Rising NPAs, Deteriorating asset quality is something RBI doesn’t like.So, what do you think? The appointment of Subramania is just a coincidence or RBIs plan to avoid another Yes Bank fiasco?

- Performance Analysis

- Nifty Outlook

- Market Trends

- Insights on Market

Trending on 5paisa

Varda Khade

Varda Khade

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.