Long Term Capital Gain Tax on Mutual Funds

5paisa Research Team Date: 12 Sep, 2023 02:17 PM IST

Want to start your Investment Journey?

Content

- What is Long Term Capital Gain Tax on Mutual Funds

- Understanding Details about Long-term Capital Gain Tax on Mutual Funds

- Tax Implication on Systematic Investment Plan

- Tax Situation on Long-term Capital Gains

- How to Calculate the Payable Tax against Long Term Capital Gains on Mutual Funds?

- Calculation Example

- Exemptions on Capital Gains

- Conclusion

The long-term capital gains tax on mutual funds is lower than the short-term capital gains tax on mutual funds. This tax structure was implemented to encourage investors to keep their money invested for a longer length of time. The long-term capital gain tax dynamics for mutual funds are a little different. Every installment of a SIP is treated as a distinct investment. As a result, tax is imposed individually on each instalment's gains. The type of fund it is invested in determines the tax rate that is triggered.

Scroll through this article to expand your knowledge about tax on long-term mutual fund returns.

What is Long Term Capital Gain Tax on Mutual Funds

Long-term capital gains on mutual funds are available when you sell your equity shares after holding on to them for more than a year. When your long-term capital gains are above Rs 1 lakh, you will have to bear taxes on them. The LTCG on mutual funds tax rate is 10% with no indexation benefit.

Remember that you will have to bear taxes on mutual fund investments only when you sell the scheme or redeem the units. Therefore, the capital gain tax on mutual fund schemes is not applicable every year.

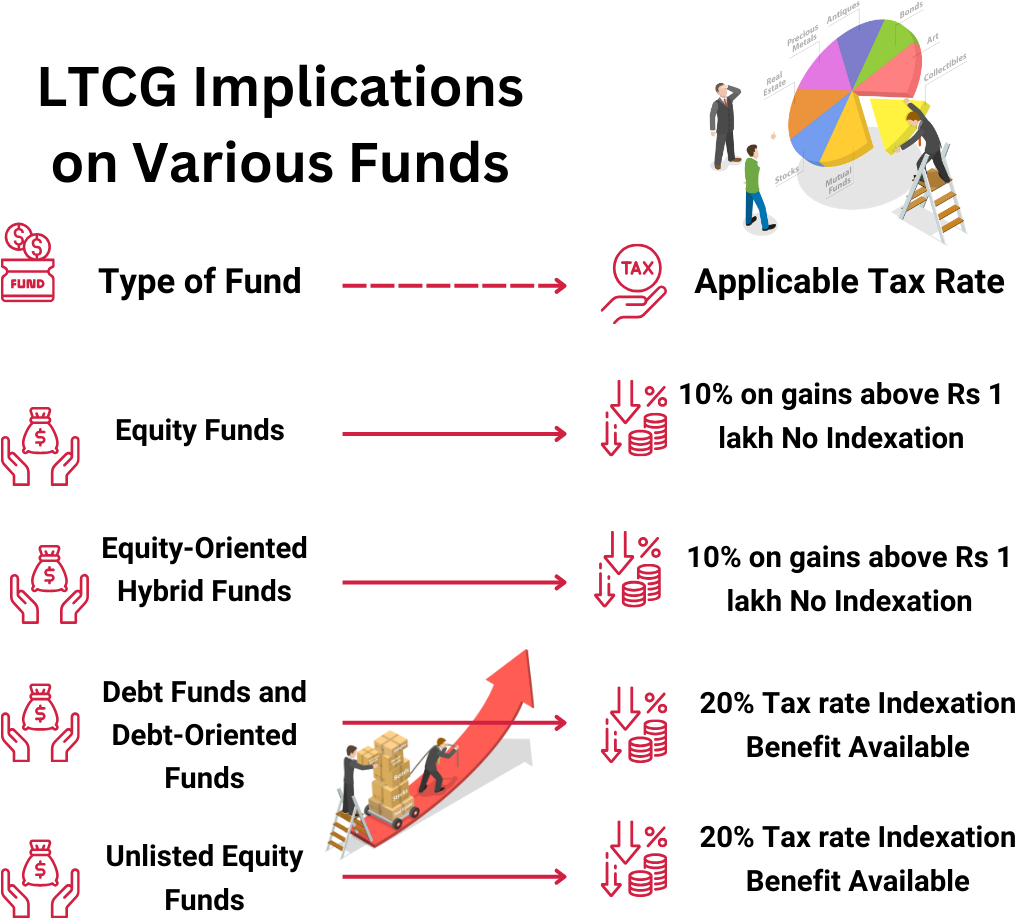

Understanding Details about Long-term Capital Gain Tax on Mutual Funds

The mutual fund taxation rate will vary for investors according to the amount they are holding. The tax implications of mutual funds of different types are as follows:

● Equity Funds

These mutual funds invest in the equity shares of different companies. You will come across tax-saving as well as non-tax saving equity funds in the market.

The tax-saving equity fund is called the Equity-Linked Savings Scheme or ELSS. They come with a lock-in period of 3 years, during which you cannot sell or transfer the funds. Therefore, they will attract long-term capital gain on tax.

In the case of non-tax saving equity funds, you won’t find any lock-in period. Therefore, they can attract long term capital gain tax as well as short term capital gain tax according to the holding period. These equity funds have a 10% tax when the gains are above Rs 1 lakh.

● Equity-oriented Hybrid Funds

These mutual funds are useful for buying debt as well as equity funds. In hybrid funds, 65% of the investments should be toward equity or equity-oriented shares. Therefore, the long term capital gain tax on these funds is similar to equity funds.

● Debt Funds

These mutual funds are for purchasing debt instruments from the market. The long term capital gains on mutual funds that invest in debt instruments are taxable at a rate of 20% after indexation. The Cost Inflation Rate is used to perform the indexation.

The Cost Inflation Index can be calculated by checking the inflation in the acquisition cost. It is useful for reducing the capital gain amount. The formula for the collection of the CII is as follows:

(Actual cost of acquisition * Index of the current year)/ Index of the base year.

● Debt-oriented Balanced Funds

In these mutual funds, more than 60% of the assets are invested toward debt instruments in the market. The tax rate applicable to these funds is 20% after indexation.

● Unlisted Equity Funds

The long term capital gains from unlisted equity funds have a tax rate of 20% and the benefit of indexation. The tax rate for the unlisted equity funds includes the applicable surcharge and cess tax.

|

Type of Fund |

Applicable Tax Rate |

|

Equity Funds |

10% on gains above Rs 1 lakh No indexation |

|

Equity-Oriented Hybrid Funds |

10% on gains above Rs 1 lakh No indexation |

|

Debt Funds and Debt-Oriented Funds |

20% tax rate Indexation benefit available |

|

Unlisted Equity Funds |

20% tax rate Indexation benefit available |

Tax Implication on Systematic Investment Plan

The long term capital gain tax on mutual funds is calculated differently when you are investing through a SIP. If you are investing through SIP, each installment is considered a separate investment.

Therefore, the tax becomes applicable on the long term capital gains on mutual funds from each installment. The tax rate will depend on how much you are investing.

Tax Situation on Long-term Capital Gains

The long term capital gain tax on mutual funds did not exist before 2018. A flat 10% became applicable as capital gains tax on investments. But the tax will be applicable only when the capital gains amount is more than Rs 1 lakh. Since it is a flat tax, you will always have to bear a tax of 10% on capital gains above Rs 1 lakh, no matter how long you have held the funds.

How to Calculate the Payable Tax against Long Term Capital Gains on Mutual Funds?

To calculate the long term capital gain tax on mutual funds, you will have to be aware of the following terms:

● Cost of Acquisition: It refers to the value with which a seller has gained the capital asset.

● Full Value of Consideration: It refers to the consideration yet to be received or already received by a seller for transferring their capital asset.

Calculation Example

For instance, you bought shares for Rs 50,000 in January 2016 and sold them at Rs 3 lakh in February 2018. Due to a tenure of more than 12 months, the profits will be considered a long-term capital gain.

To calculate the long term capital gains on mutual funds, you will have to consider the following:

● The full value of consideration: Rs 3 lakh

● If the cost of inflation index for the mentioned year is 280, the indexed cost of acquisition will be Rs 50,000 * (280/ 100)= Rs 1,40,000.

● The total taxable gain will be Rs 3,00,000 - Rs 1,40,000= Rs 1,60,000

The rate of long term capital gain tax on mutual funds over Rs 1 lakh is 10%. Therefore, the tax amount applicable to the mutual fund gains mentioned above is Rs 16,000.

Exemptions on Capital Gains

You can enjoy the following tax exemptions on LTCG on mutual funds:

Section 10(38)

According to this section, the long term capital gains on mutual funds are exempt from taxes under the following circumstances:

1. The transfer was made after 1 October 2004.

2. A long-term asset was transferred.

3. The sale transaction is liable under security transaction tax.

Section 54F

You can enjoy tax benefits on the sale of an asset from long-term capital gains on mutual funds. You can claim these capital gain tax exemptions for mutual funds under the following conditions:

● You will have to buy an asset one year before or a couple of years after the date of sale.

● You have constructed property with your capital gains from sales. The construction must be completed within three years from the date of the transaction.

Conclusion

When you hold your mutual fund schemes for a long time, they become more tax-efficient. The tax applicable on long term capital gains on mutual funds is much lower than short term capital gains. Therefore, planning your mutual fund investments for the long term can help you enjoy several tax benefits.

More About Mutual Funds

- SWP and Dividend Plan

- What is Solution Oriented Mutual Funds?

- Growth Vs Dividend Reinvestment Option

- Annual vs Trailing vs Rolling Returns

- How to Get Capital Gain Statement for Mutual Funds

- Mutual Funds Vs Real Estate

- Mutual Funds vs. Hedge Funds

- Target Maturity Funds

- How to Check Mutual Fund Status with Folio Number

- Oldest Mutual Funds In India

- History Of Mutual Funds In India

- How To Redeem ELSS Before 3 Years?

- Types of Index Funds

- Who Regulates Mutual Funds In India?

- Mutual Fund Vs. Share Market

- Absolute Return in Mutual Fund

- ELSS Lock in Period

- Treasury Bills Repurchase (TREPS)

- Target Date Fund

- Stock SIP vs Mutual Fund SIP

- ULIP vs ELSS

- Long Term Capital Gain Tax on Mutual Funds

- Smart Beta Funds

- Inverted Yield Curve

- Sinking Fund

- Risk-Return Trade-Off

- Registrar and Transfer Agents (RTA)

- Mutual Funds Overlap

- Mutual Fund Redemption

- Mark to Market (MTM)

- Information Ratio

- Difference Between ETF and Index Fund

- Difference Between Mutual Fund and Index Fund

- Top 10 High Return Mutual Funds

- Passive Mutual Funds

- Passive Funds vs Active Funds

- Consolidated Account Statement

- Mutual Funds Minimum Investment

- What is Open Ended Mutual Fund?

- What is Closed End Mutual Fund?

- Real-Estate Mutual Funds

- How to Stop SIP?

- How to Invest in SIP

- What is a Blue Chip Fund?

- What is XIRR in Mutual Funds?

- What is a Hedge Fund?

- Tax Treatment of Long Term Capital Gains

- What is SIP?

- NAV in Mutual Funds

- Advantages of Mutual Funds

- Stocks vs Mutual Funds

- What is STP in Mutual Fund

- How Mutual Fund Works?

- What is Mutual Fund NAV?

- What are Mutual Funds?

- Mutual Fund Cut Off Time

- Mutual Fund the Best Investment Option for Conservative Investors

- Advantages and Disadvantages of Mutual Funds

- How to Choose Mutual Funds in India?

- How to Invest In Mutual Funds?

- How to Calculate NAV of Mutual Fund?

- What Is CAGR In Mutual Funds?

- What is AUM in Mutual Fund

- What is Total Expense Ratio ?

- What is XIRR in Mutual Funds?

- What is SWP in Mutual Fund

- How to Calculate Mutual Fund Return?

- Gold Mutual Funds

- Tax On Mutual Fund Investment

- The Top Benefits and Drawbacks of The Rupee Cost Averaging Approach

- How to Start a SIP Investment?

- What Is SIP & How does SIP Work?

- Best SIP Plans for Long Term: How and Where to Invest

- Best SIP Mutual Fund Plans

- ELSS Vs SIP

- Top Fund Managers in India

- What is NFO?

- Difference Between ETF and Mutual Fund

- ULIPs VS Mutual Funds

- Direct Vs. Regular Mutual Funds: What’s The Difference?

- ELSS vs Equity Mutual Fund

- NPS vs Mutual Fund

- Can NRIs Invest in Mutual Funds?

- Mutual Funds Categorisation In India

- Everything You Need to Know About Small-Cap Funds

- What is Public Provident Fund ?

- What is Large Cap Mutual Fund ?

- What is Index Fund ?

- What is IDCW in Mutual Fund ?

- What is Hybrid Fund?

- What is Gilt Fund ?

- What is ELSS Fund ?

- What is Debt Funds?

- What is an Asset Management Company - A Thorough Explanation

- What are Mid Cap Funds

- Liquid Funds - What are Liquid Funds?

- A Beginner's Guide to Investing in Fund of Funds Read More

Open Free Demat Account

Be a part of 5paisa community - The first listed discount broker of India.