What are Bonds?

5paisa Capital Ltd

- What Is a Bond?

- Types of bonds

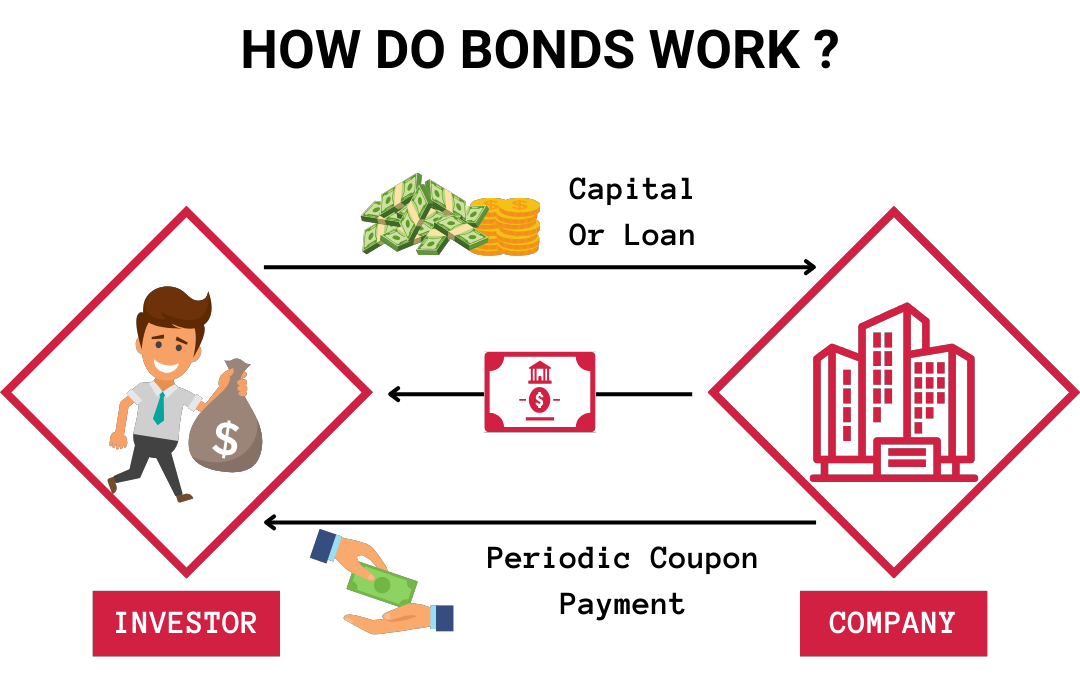

- How do bonds work?

- How To Invest in Bonds?

- Bond Elements

- Example of How Bonds Work

- How Do Bond Ratings Work?

- How Bonds Are Priced?

- Features of a Bond

- Conclusion

A bond is a type of debt security. Bonds are issued by borrowers to attract capital from investors ready to extend a loan to them for a specific period of time.

When you purchase a bond, you are making a loan to the issuer, which could be a corporate, government, or municipality. In exchange, the issuer agrees to pay you a specific rate of interest throughout the course of the bond's existence and to refund the bond's principal when it "matures," or becomes due, after a predetermined amount of time.

Learn more about what is a bond, its types, and more, in this blog.

More Articles to Explore

- BankBees vs Bank Nifty: Key Differences

- How to Earn ₹1000/Day from Share Market

- Rights Issue of Shares: Meaning & Benefits

- SEBI Registered Investment Advisor (RIA) Guide

- Worst Stock Market Crashes in History

- Types of Dividend in Stock Market

- What is a Block Deal? Meaning & Rules

- CE vs PE in Stock Market Explained

- What is Market Mood Index?

- What is Short Covering in Stock Market?

Disclaimer: Investment in securities market are subject to market risks, read all the related documents carefully before investing. For detailed disclaimer please Click here.

Frequently Asked Questions

Throughout its term, bonds earn fixed or variable interest rates that are paid to creditors on a regular basis. Because interest is traditionally paid on paper bonds in the form of coupons, bond interest rates are also known as coupon rates. Bond interest rates are determined by a number of factors, including bond duration and the issuer's standing in the public debt market.

Credit rating firms such as Standard and Poor's, Moody's, and Fitch Ratings provide credit ratings for a company and its bonds. The term "investment grade" refers to the highest caliber bonds, which include those issued by the US government and extremely reliable businesses like several utilities.

"High yield" or "junk" bonds are those that are not investment grade but are also not in default. Investors demand a larger coupon payment on these bonds since they have a bigger default risk in the future.

Anyone who is interested in stable and predictable income and little above the fixed deposited return can make investment in the Bonds.

Government and Municipal bond are considering to be safest bond in India.

Yes, you can make profit from Bonds Investment if you stay holder till it matures.

Yes, the issuer and the Credit rating of the bonds and the market situation ans also the bond is embedded or not.